2018 Growth Forecasts on the Up

2018 Growth Forecasts Inch Upward Due to Positive External Trends, Higher Gov’t Expenditure on Capital

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the second quarter of 2018. Here are the highlights of this month’s release:

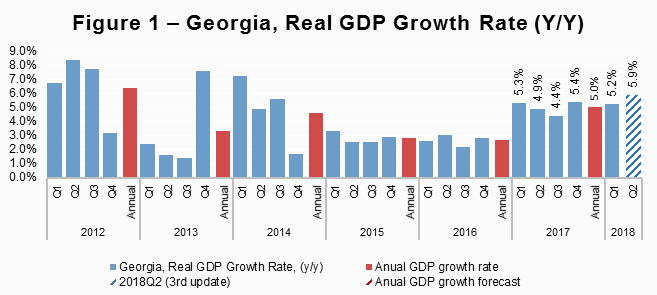

• Geostat has released its GDP growth estimate for the first quarter of 2018. The Q1 growth stands at 5.2 percent, which is 1.1 percentage points above the recent forecast.

• ISET-PI’s forecast of the real GDP growth for the second quarter of 2018 stands at 5.9 percent - up from 5.1 percent in April.

• Based on March’s data, we expect annual growth in 2018 to be 5.4 percent in the worst-case or “no growth” scenario, and 6.4 percent in the best-case or “average long-term growth” scenario. Our “middle-of-the road” scenario (based on average growth over the last four quarters) predicts 5.7 percent real GDP growth in 2018.

• The National Bank of Georgia has revised the real GDP growth forecast upward to 4.8 percent in 2018 from 4.5 percent in February. The upward revision was explained by positive trends in the external sector and increased government capital spending, which is expected to improve consumption and investment spending, and further contribute to growth.

According to the recent Geostat’s release, the official estimate of growth for the first quarter of 2018, which is based on VAT taxpayers’ turnover data, now stands at 5.2 percent. The newly estimated Q1 figure is higher than initially anticipated by the ISET-PI forecast. Consequently, ISET-PI second quarter forecast has also been revised upward to 5.9 percent. The upward revision of the forecast is most likely due to the improved external environment, credit expansion and fiscal stimulus in Georgia.

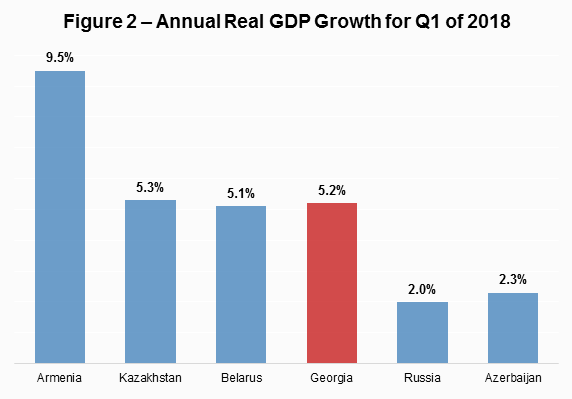

The beginning of 2018 showed strong growth trends in Georgia’s neighboring region, which further stimulated the Georgian economy though trade, remittances and tourism channels

According to the rapid estimates of real GDP growth for the first three months of 2018, the majority of countries in the region showed significant improvement in terms of economic activities compared to the same period of the previous year. The Armenian economy advanced by 9.5 percent year over year, while Azerbaijan experienced 2.3 percent annual growth. Moreover, the growth rate of the real GDP for Kazakhstan and Belarus reached 5.5 percent and 5.1 percent respectively. The Russian economy grew by 2.0 percent in January-February of 2018 compared to the same period of 2017.

In March 2018, external merchandise trade increased by 34.3 percent year over year. Exports of the merchandise goods increased by 33.1 percent year over year, while import advanced by 34.7 percent. Consequently, trade deficit deepened by 35.6 percent compared to the same period of the previous year. In addition, remittances and tourism maintained double-digit growth in the third month of 2018. Money inflow increased by 17.0 percent compared to the same period of the previous year. The number of international visitors also increased by 13.2 percent, while the change in tourist numbers (visitors who spent 24 hours or more in Georgia) was even higher – a 33.0 percent increase. Both tourism and remittances increase disposable income of citizens and have significant positive contribution to estimated GDP growth.

Rapid credit expansion is likely to boost economic activities in the short-run, but unchecked credit growth might have negative long-run consequences.

The domestic credit to the private sector extended by commercial banks grew by 21.1 percent in March of 2018. The domestic currency loans increased by 39.4 percent year over year (accounted for 15.6 percentage point of the growth in the total domestic credit to the private sector), while foreign currency loans experienced a relatively moderate 9.1 percent growth (accounted for only 5.5 percentage point of the growth in total credit). As a result, loan dollarization was reduced to 55.0 percent, compared to the 61.0 percent in the same period of the previous year.

Rapid credit expansion positively contributes to the short-term growth figures by stimulating private consumption. However, the growth rate of domestic credit significantly exceeds the growth of the Georgian economy as a whole, and borrowed money is often spent on purchasing imported products and services. This might have negative implications for the long-run economic growth of the country. Thus, domestic credit expansion needs to be closely monitored by the National Bank.

Financial sector environment in Georgia remains sounds.

In March, banks retained their highly profitability profile, with a return on equity (ROE) and return on assets (ROA) at 20.6 percent (0.4 percentage point lower than previous month) and 2.8 percent (0.1 percentage point lower than previous month), respectively. In addition, non-performing loans (NPL) decreased by 0.1 percentage point m-o-m to 1.6 percent of the total loan portfolio in March 2018, and 46.4 percent of NPLs were denominated in domestic currency.

The consolidated government budget was in surplus in March, even despite a significant increase in the infrastructure-related spending.

Tax collections decreased by 10.6 percent in March year over year, while current spending went down by 5.1 percent in yearly terms. The decrease in compensation to employers and other payments categories was balanced by higher spending on purchases of goods and services and interest payments. However, due to higher infrastructural spending – net acquisition of non-financial assets spiked by 61.6 percent. General budget ended up in surplus of 130.7 million lari, 46.7 percent smaller than in the March of 2017. Increased government spending (including net acquisition of non-financial assets) further contributed to economic growth.

Inflation rate continues to fluctuate around the targeted level as the exchange rate strengthens and the one-time price level increases are phased out.

In March 2018 lari strengthened against the US dollar by 0.9 percent, while nominal effective exchange rate gained 1.4 percent m-o-m. The pressures on prices from higher excise taxes in January 2017 (which caused a one-time shift in price levels) are already exhausted. Annual inflation in March 2018 constituted 2.8 percent, which was in line with the 3 percent NBG target.

The Monetary Policy Committee of NBG met on March 14, 2018 and decided to maintain the moderately tight monetary policy rate (7.25 percent). This decision was explained by the fact that despite the recent appreciation of the nominal effective exchange rate, the latter still pushes the inflation upwards. At this moment the future path of inflation mainly depends on the developments in the external sector.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including the GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych