GOGC - Ensuring Energy Security of Georgia

Fixed income research is one of the key directions of Galt & Taggart Research. We currently provide coverage of Georgian Oil and Gas Corporation and Georgian Railway, two state-owned entities with Eurobonds listed on the London Stock Exchange in the amount of US$ 250mn and US$ 500mn, respectively. In this article, we provide an overview of the Georgian Oil and Gas Corporation and its key role in ensuring energy security of Georgia, as well as a brief outline of the sector.

Georgian Oil and Gas Corporation (GOGC) is a state-owned company (under the Partnership Fund) committed to ensuring the energy security of Georgia. GOGC holds the legal status of a National Oil Company (NOC) and represents the state’s interests in upstream crude oil and natural gas projects in Georgia. GOGC was established to consolidate Georgia’s energy assets under single management. The company has five core activities:

- Ensuring long-term and sustainable development of the wholesale natural gas market;

- Managing the preparation, storage, transportation and sale of the state share of natural gas and oil;

- Commissioning, constructing, rehabilitating and replacing oil and gas pipelines on the Georgian territory;

- Implementing the projects aimed at transporting oil and gas from the Caspian and other regions via trunk pipelines on the Georgian territory;

- Participating in and implementing national and international projects aimed at exploration, transportation and supply of energy resources.

Georgia’s auspicious strategic location makes it a transport corridor for natural gas and crude oil supplies to European markets. The transport corridor through Georgia allows the EU to diversify its supply, increasing energy security. In addition, Georgia is the only route for the transportation of Russian natural gas to Armenia. Georgia’s favorable location has prompted significant investments into its oil and gas sector. To that end, GOGC represents the state in international energy transit projects. Georgia’s main natural gas pipelines are:

- Main Gas Pipeline System (MGPS) that stretches across the country and is comprised of:

- North-South Gas Pipeline (NSGP), extending 235km and transporting gas from Russia to Armenia;

- East-West Gas Pipeline (EWGP);

- Southern branch;

- Kakheti branch;

- South Caucasus Pipeline (SCP) that stretches 692km (249km in Georgia) and transports natural gas from Azerbaijan to Turkey through Georgia and from Turkey further to the EU. The Southern Gas Corridor project, aimed at improving the security and diversity of EU energy supply, will bring additional volumes of natural gas from the Caspian region to Europe. It is comprised of several separate energy projects, including the expansion of the SCP pipeline, which should bring additional volumes to GOGC as the pipeline capacity is poised to triple by 2021. As of end-1Q15, the SCP expansion project was 31.0% completed and ahead of schedule.

Georgia’s main oil pipelines are:

- Western Route Export Pipeline (WREP) that stretches 833km (375km in Georgia) and transits crude oil from Azerbaijan to the Black Sea coast (Supsa) for onward shipping to global markets;

- Baku-Tbilisi-Ceyhan Pipeline (BTCP) that stretches 1,768km long (249km in Georgia) and transits crude oil from Azerbaijan to Turkey on the Mediterranean Sea.

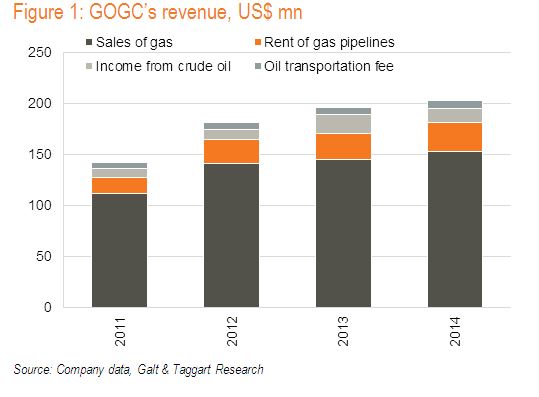

GOGC has long-term contracts with the operators of SCP and NSGP pipelines, through which the company receives gas at a favorable price and as an in-kind payment, respectively. GOGC also has a new contract with SOCAR for additional gas volumes at below-market prices. In 2014, GOGC imported 55.8% of Georgian national gas consumption (the remaining 44.2% was imported by SOCAR directly). The imported gas is then sold to the wholesaler, SOCAR Gas Export Import, which resells the gas to distribution companies. GOGC’s natural gas import and its further wholesale distribution is mainly aimed at supplying the household and power generation sectors, while the commercial sector is mostly supplied by SOCAR directly. Apart from the sale of gas and pipeline rental activities, GOGC also engages in upstream activities pursuant to its NOC status, in addition to receiving fees for the oil transported through the WREP pipeline.

Through 2011-14, GOGC’s revenue grew by a remarkable 12.5% CAGR. The growth has been driven by sale of gas and pipeline rental activities, accounting for 75.4% and 14.2% of the top line in FY14, respectively. In general, GOGC posted promising FY14 results, given the high regional uncertainty in 2014, especially in the oil and gas sector. In addition, a 14.3% y/y surge in national natural gas consumption last year suggests further upside potential for the company. Moreover, Gardabani CCPP is poised to start operations in late 2015 and boost profitability from the sale of electricity.

To facilitate Georgia’s energy security while diversifying the company’s revenue sources, GOGC initiated a major capital project in 2012, the Gardabani Combined Cycle Power Plant (CCPP). To finance the US$ 230mn project, GOGC placed a US$ 250mn, 5-year Eurobond on the London Stock Exchange. With a sizable 230MW installed capacity, Gardabani CCPP is the first power plant of its kind in the country. Gardabani CCPP has the reserve capacity to supply the country's energy grid in 25 to 30 minutes in case of a power failure. Construction of the plant began in early 2013 and was completed ahead of schedule. The power plant is expected to commence operations in late 2015, providing a profitable revenue stream for GOGC and ensuring energy security for Georgia. The government of Georgia, in line with its privatization plan, is considering the sale of Gardabani CCPP. A final decision regarding the sale is expected by the end of November 2015.

Two new major capital projects are in the pipeline for GOGC. The first one is building an underground gas storage reservoir in Samgori. It would be a strategically important gas storage facility for Georgia, increasing energy security by ensuring gas supply in critical situations and by mitigating the seasonal imbalance between supply and demand. The storage capacity would be 230-250 mmcm, about 10-15% of current annual consumption. Notably, Georgia is currently the only country in the region with no gas storage. A feasibility study should be completed by early 2016. If a decision is made to proceed with the project, the construction would commence in 2016 with expected completion in 2019. The estimated project cost is around US$ 250mn.

GOGC is also considering building a new combined cycle power plant, Gardabani CCPP II, with similar technical characteristics and in proximity to Gardabani CCPP. Given the experience gained in building Gardabani CCPP, which was completed ahead of schedule, GOGC is likely to benefit from significant savings on the construction of Gardabani CCPP II. The final decision will largely depend on whether Gardabani CCPP is sold.

GOGC’s mid-term outlook looks promising on the back of a profitable gas supply business, stable income stream from oil and gas transportation activities, and an attractive opportunity to enter the electricity generation segment. Minor capex requirements for projects in process, an experienced management team, and limited FX rate exposure further support our optimistic outlook. Keeping in mind the company’s track record, we expect GOGC to build on its successes in its crucial role in the oil and gas sector at both national and regional levels.

David Ninikelashvili (Galt and Taggart)