Despite Optimistic Growth Forecasts, Trade Deficit up in April

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the second and third quarters of 2018. Here are the highlights of this month’s release:

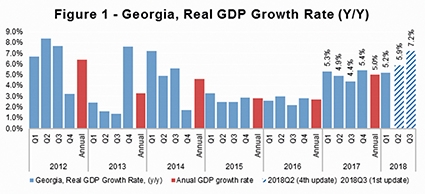

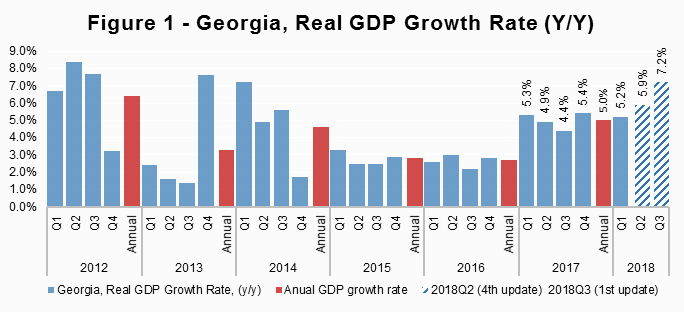

• Geostat has released its GDP growth estimate for the first quarter of 2018. The Q1 growth stands at 5.2%, which is 1.1 percentage points above the recent forecast.

• ISET-PI’s forecast of real GDP growth for the second quarter of 2018 remains unchanged at 5.9%. The first estimate for the third quarter growth forecast is at 7.2%.

• Based on April’s data, we expect annual growth in 2018 to be 6.2% in the worst-case or “no growth” scenario, and 6.5% in the best-case or “average long-term growth” scenario. Our “middle-of-the road” scenario (based on average growth over the last four quarters) predicts 6.3% real GDP growth in 2018.

Geostat has released its preliminary estimate of GDP growth for the first quarter of 2018. Its estimated growth figure is 5.9%, which is 1.1 percentage point higher than ISET PI’s forecast. As a result, our projected real GDP growth for the second quarter of 2018 has also been revised upward to 5.9%. Moreover, ISET PI’s first forecast of the third quarter growth is also very optimistic, at 7.2%. These high forecast figures can be explained by the fact that quarterly growth rates typically follow a certain pattern, captured by ISET-PI’s empirical forecast model. Thus, the higher-than-usual growth in the first quarter may result in an overly optimistic forecast about the next quarter’s performance. Indeed, ISET PI’s forecasts for Q2 and Q3 are largely influenced by the high Q1 actual growth.

Yet, looking at the economic landscape from the standpoint of April data, we note that several variables changed significantly, affecting growth predictions. Improved external statistics, the accelerated growth of national currency deposits, credit expansion and increased monetary aggregates were the main contributors to real GDP growth.

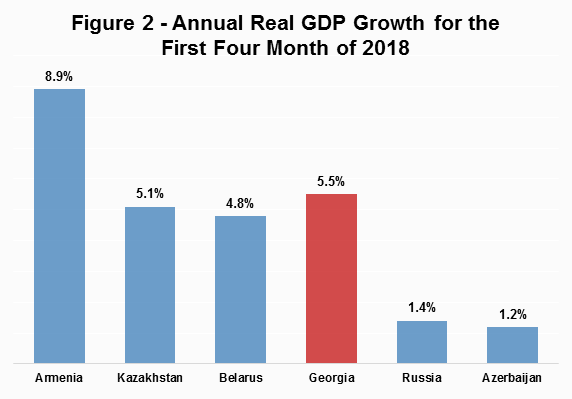

Improved Economic Conditions in the Wider Region

The beginning of 2018 showed strong growth figures in the wider region. According to the rapid estimates of real GDP growth, most of the countries in the region experienced significant acceleration of economic activities in the first four months of 2018. The Armenian economy advanced by 8.9% annually, while the Russian and Azerbaijani economies grew on average by 1.4% and 1.2%, respectively. Improved economic conditions in the wider neighborhood further stimulated the Georgian economy though trade, remittances and tourism channels.

Promising Statistics of Export, Remittances and Tourism

In April 2018, total exports grew by 8.3% year over year (slightly decelerated growth rate compared to the earlier months of 2018), driven by the export of alcoholic beverages, higher re-exports of motor cars to Azerbaijan, Ukraine and Armenia, accelerated export/re-exports of tobacco products (increased by more than 22 times on an annual basis), and mineral/chemical fertilizers. Re-export of copper and copper ores, however, was reduced by 51.4%. The main destination markets for Georgian export products were Turkey, Russia, Azerbaijan, Bulgaria and Armenia, accounting for 55% of total exports.

During the same period, imports of merchandise goods increased by 22.0%, driven by petroleum and petroleum gases, motor cars and copper ores and concentrates. The main trading partners of Georgia for imports were Turkey, Russia, China, Azerbaijan and Ukraine, accounting for the 47% of total imports. As a result, the trade deficit deepened by 29.5%, compared to the same month in 2017.

Both remittances and tourism showed significant yearly increases in April of 2018. Money transfers rose by 17.1% in the fourth month of 2018, driven by remittances from Israel (32% annual growth), Italy (43.6%), Greece (35.2%), Germany (32.9%), Azerbaijan (35.2%), and Turkey (8.7%). Notably, remittances from the Russian Federation experienced a slight yearly reduction. Nevertheless, Russia remains the top country of origin for money inflow, accounting for 28% of total remittances.

The number of all type of visitors in April of 2018 increased by 16.8% year over year and exceeded 619,000 people. Out of these, 56.6% were classified as tourists, and the growth rate of these visits reached 24.9% annually. The top five countries of origin for international visitors were Turkey (16.6% of total visitors), Azerbaijan (15.9%), Armenia (14.6%), Russia (14.4%) and Iran (4.2%). Both tourism and remittances contributed significantly to the GDP growth forecast.

Foreign Direct Investment, however, shrunk by 32.9% in the first quarter of 2018 compared to the same month of the previous year. According to Geostat, the main reason for decreasing FDI was the transfer of ownership in some companies from non-residents to residents, and the reduction of debt liabilities to non-resident direct investors (mostly payment of loans). The main countries of origin for foreign direct investment were the United Kingdom (29.6% of total FDI), Azerbaijan (18.2%), China (14.9%), the Netherlands (11.6%), and the United States (8.5%), accounting for 82.8% of total FDI. The economic sectors that depressed FDI growth the most were transport and communication (-37.7 ppt) and real estate (-24.2 ppt), while other sectors positively contributed to the growth figure – manufacturing (+8.1 ppt), financial (+7.8), and construction (+3.5 ppt).

Increase in National Currency Deposits

Total deposits (stocks) in commercial banks amounted to 21 billion GEL by the end of April - 20.4% higher than in the same month of the previous year. In particular, the stock of national currency deposits grew substantially, by 46%, while the stock of foreign currency deposits increased by only 9.1%. The largest yearly increase was observed for National Currency Time Deposits with less than 3 months of maturity – a 169% increase relative to the same month of the previous year. The second largest yearly increase was experienced by National Currency Demand Deposits – a 95% increase year over year. Overall, National Currency Total Deposits increased by more than 46% yearly. National Currency Deposit-related variables had a positive contribution to our GDP growth projection

The dollarization rates of non-bank deposits and loans decreased in April of 2018. Dollarization of deposits fell by 0.4 ppt, amounting to 62.5%, while loan dollarization was reduced by 0.1 ppt to 55.0%, compared to March of 2018. According to our model, deposit dollarization had a small, but positive, impact on real GDP growth.

Credit Expansion

Domestic credit to the private sector extended by commercial banks grew by 20.8% (even after excluding exchange rate effect growth rate, domestic credit still was 19.3%) in April of 2018. The credit portfolio grew due to the increase in loans issued in the national currency, as well as the expansion of loans issued in foreign currency. Rapidly growing credit positively contributes to the short-term growth figures by stimulating private consumption. However, the growth rate of domestic credit significantly exceeds the growth of Georgian economy and borrowed money is often spent on purchasing imported goods and services, which might have negative consequences to long-run economic growth.

Expansion of Monetary Aggregates

The other set of variables that had a significant positive effect on our forecast is related to currency in circulation. The Monetary Policy Committee of the National Bank of Georgia met in May and June, and decided to leave the monetary policy rate unchanged at 7.25%. However, all of the monetary aggregates, including the largest - Broad Money (M3) - experienced significant yearly growth (M3 aggregate rose by 17%). The largest increase was observed for Monetary Aggregate M2, which went up by 22% relative to the same month in the previous year. Moreover, Currency in Circulation itself increased by 8% in yearly terms. Rapid expansion of monetary aggregates contributed positively to real GDP growth forecast.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including the GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych