A Fruitful Summer for Georgian Agriculture! The Business Confidence Index Q3 2018

ISET ECONOMIC INDICATORS

Overall, the BCI lost 4.2 points compared to Q2 2018. Expectations in the private sector in Georgia decreased by 2.8 percentage points, and dropped to 64.2 index points (up from 67.0 points in Q2). Business performance over the past three months decreased, reaching nearly 38.2 points (decreasing from 41.6), indicating a downturn in production/turnover/sales. The synergy of worsening performance in the past three months and lower expectations have led to a drop in overall BCI.

The BCI index worsened in manufacturing (-36.2), retail trade (-10.1), financial (-36.2), and other (-4.2) sectors. The construction, agriculture and service sectors improved by 16.4, 13.4 and 4.7 points, respectively.

Business confidence in the third quarter of 2018 decreased for both large firms (-3.8) and SMEs (-5.9). Both types of firms expressed less optimism and had weaker performance, which resulted in a decrease of -4.2 index in overall BCI.

Past performance

Businesses’ actual performance decreased by -3.4 compared to the second quarter of 2018. In the Q3 2018 reporting period, sales (production or turnover) of the 130 firms surveyed decreased from 41.6 (Q2 2018) to 38.2 (Q3 2018).

A significant increase in performance was observed in the agriculture (+86.1) and construction (+27.0) sectors. Significant improvement means that in these sectors, the weighted balance between positive and negative responses decreased compared to the previous quarter. In the remaining sectors, production/turnover/sales for the past three months worsened: financial (-52.9), manufacturing (-46.7), service (-1.8) and others (-45.0) sectors.

Expectations

The Expectations Index decreased by 2.8 index points in the third quarter of 2018. Expectations about the next three months improved for the agriculture (47.0), construction (2.9) and service (4.1) sectors. The highest decrease was reported in the manufacturing and retail trade sectors.

The majority (59%) of surveyed businesses do not expect any changes in employment over the next three months. Furthermore, 28% of firms stated that they would employ more employees in the future.

55% of the surveyed firms expected that the economic condition of their businesses would improve over the next three months, and 35% did not expect any changes in the future, while a lower share of businesses expect their business conditions to worsen.

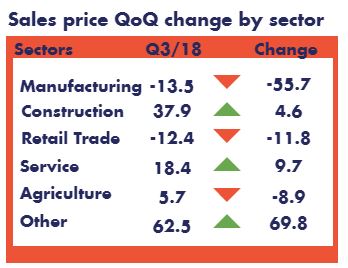

Sales Prices Expectations

The Sale Price Expectation Index decreased from 11.7 points (Q2 2018) to 10.3 points (Q3 2018). The decrease in the Index is driven by a significant drop in the manufacturing, retail trade and agriculture sectors. The manufacturing sector expects a noticeable decrease in prices over the next three months, while the service and construction sectors expect an increase.

The majority (77%) of all surveyed firms are not going to change the prices they charge over the next three months. Only 8% of firms expect to decrease prices, and 15% expect to increase prices in the future.

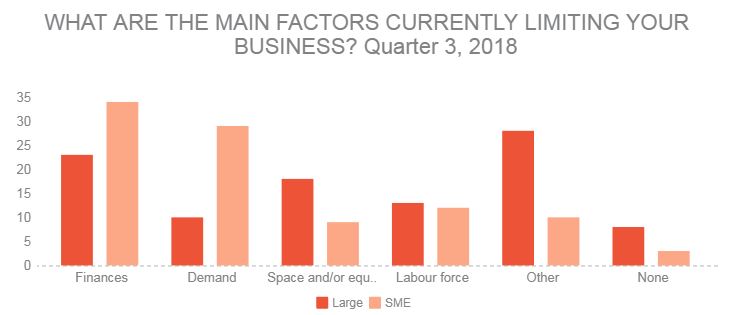

A low level of consumption activities and lack of access to financing continue to be two of the most significant obstacles for businesses. From a total of 130 firms participating in the survey, 23% of large sized firms and 34% of SMEs noted that lack of access to finance was their main obstacle. Meanwhile, 10% of large firms and 29% of SMEs chose lack of demand as the main limiting factor for further business development.

It should be noted that the BCI results presented here may be overestimated, as the survey only covers businesses currently operating, and not those that have already exited the market. Firms still in operation are more likely to have a negative outlook to some extent.