Georgia's Growth Projections Strong, but Turkish Lira Crisis May Dampen Buoyant Forecasts

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the third and fourth quarters of 2018. Here are the highlights of this month’s release:

Highlights

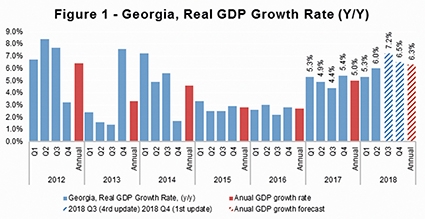

• Recently, Geostat released the preliminary estimate of real GDP growth for the second quarter (April-June) of 2018, which now stands at 6.0%. This is only 0.1 percentage points above the recent ISET-PI forecast. As a result, real GDP growth for the first seven months of 2018 reached 5.5%.

• ISET-PI’s forecast of real GDP growth for the third quarter (July-September) of 2018 stands at 7.2% - the same as last month’s prediction. The first estimate for the fourth quarter (October-December) growth forecast stands at 6.5%.

• Based on July’s data, we expect annual growth in 2018 will reach 6.3%. This optimistic forecast is consistent with the evidence coming from the National Bank of Georgia and international development institutions. For example, the National Bank of Georgia revised its expectation for the real GDP growth from 4.8% to 5.5% in 2018. According to the Monetary Policy Report, among the reasons behind the upward revision of the prediction are the improved domestic and external demands due to significant foreign inflows (mainly from export, tourism, and remittances), improved business sentiment, credit growth, and capital spending by the government.

• Moreover, the International Monetary Fund (IMF) has also raised its growth forecast from 4.8% to 5.5% in 2018. IMF provided similar findings to the National Bank of Georgia, identifying some other contributors of the real GDP growth: low and stable inflation that allows the Central Bank to carry out expansionary monetary policy, and markedly reduced dollarization of loans and deposits. However, this authoritative institution identified threats coming from deteriorating economic conditions in the region.

The Georgian statistics office, Geostat, has released its preliminary estimate of GDP growth for the second quarter of 2018. Its estimated growth figure is 6.0%, which is only 0.1 percentage point higher than ISET PI’s forecast. As a result, our projected real GDP growth for the third quarter of 2018 remains unchanged at 7.2%.

ISET PI’s forecast for fourth quarter growth stands at 6.5%. This optimistic forecast figure can be explained by markedly improved external and internal conditions. The economic situation in the region remains favorable, leading to the high numbers in export (currency crisis in Turkey and ruble depreciation is not reflected in the model yet), tourism and remittances, low and stable inflation, credit expansion, enhanced monetary aggregates, and accelerated growth of national currency deposits.

External Factors

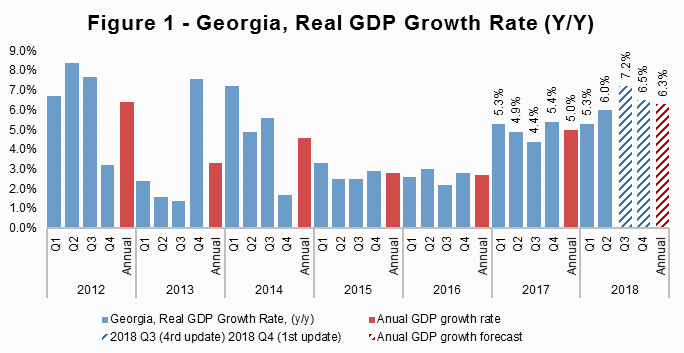

A great majority of the countries in the wider region continue their strong growth path in June and July of 2018. According to the rapid estimates of real GDP growth, Kazakhstan, Belarus, and Russia advanced on average by 4.6%, 4.5%, and 2.2%, respectively, in June-July 2018, compared to the same month of the previous year. The Armenian economy continues to surprise economists with high growth figures - currently 10.4% in annual terms. Only the Azerbaijani economy is still far behind its peer countries, with an average annual growth rate of 0.8% in June-July. Improved economic conditions in the wider neighborhood stimulated the Georgian economy through trade, remittances, and tourism channels. However, the Turkish currency crisis and the significant depreciation of the Russian ruble, both of which are potential external threats to the Georgian economy, are not taken into consideration in our model yet.

As was mentioned earlier, favorable economic conditions in Georgia’s partner countries contributed to real GDP growth through trade, remittance, and tourism. Notably, exports grew by 31% year-over-year in July of 2018, driven by significantly larger exports/re-exports of motor cars, cigarettes and cigars to Azerbaijan, increased exports/re-exports of copper ores and concentrates to China, and accelerated export of fruits, grapes and natural wines to Russia. However, the exports of ferroalloys declined by 31.5%, and exports to Turkey were reduced significantly. Furthermore, metal prices (metals are the main exporting commodity for Georgia) increased by 6% annually, but went down by 8% in monthly terms. During the same period, imports increased by 21.8%, driven by petroleum and petroleum gases, motor cars, copper ores and concentrates (the last two are used mostly for re-export). Moreover, world prices of crude oil increased by 53.2% yearly, which negatively contributed to the growth forecast. As a result, the trade deficit deepened by 17.2%, compared to the same month in 2017, and reached 503.4 million USD.

Both remittances and tourism showed significant yearly increases in July of 2018. Money transfers rose by 19.3% in the seventh month of 2018, driven by remittances from Israel (28%), Italy (35.4%), Greece (40.5%), France (72.2%), Azerbaijan (52.4%), and Turkey (8.7%). Remittances from the Russian Federation experienced a slight yearly decline and had a 0.1 percentage point negative contribution to the total growth of remittances. Nevertheless, Russia remains the top country of origin for money inflow, accounting for 29.8% of total remittances. The share of money inflow from the European Union amounted to 33.5% of the total.

The number of international visitors increased by 10.7% in July, compared to the same month of the previous year, while the number of tourists increased by 15% annually and reached 66.8% of total international visitors. According to the model, both tourism and remittances had a significant positive contribution to the GDP growth forecast.

Internal Factors

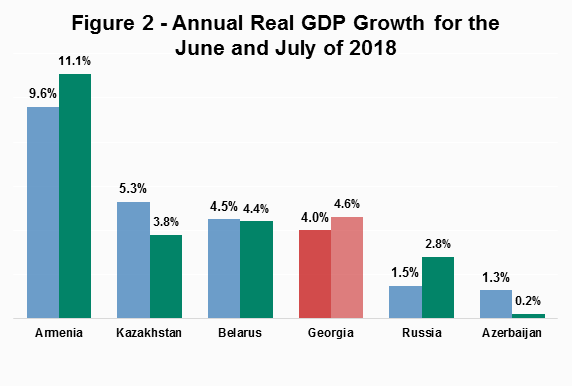

The other factor that contributed positively to the real GDP growth forecast was the expansion of credit to the national economy. Loans to the domestic economy increased by 18.9% in July compared to the same month of the previous year . The credit portfolio grew mainly due to the increase in loans issued in national currency, as well as the expansion of loans issued in foreign currency. The largest annual growth was observed in Transport and Communications (59.4%), Hotels and Restaurants (34.1%) and Transactions in Real Estates, Researches (26.8%). Rapidly growing credit positively contributes to the short-term growth figures by stimulating private consumption.

In addition to the rapid credit expansion, the National Bank of Georgia reduced the Monetary Policy Rate (MPR) by 0.25 percentage point in July, which stimulated further borrowing and contributed to higher growth. This was the first raise since September of 2016, when the National Bank of Georgia conducted an expansionary monetary policy by reducing the policy rate (NBG restricted monetary policy several times during the whole of 2017 to avoid high inflation caused by the one-time increase of the excise tax, higher crude oil and food prices in the world market, and inflationary expectations of the economic agents). A low and stable inflation (the inflation rate was 2.8% in July - very close to the targeted 3%) gives policymakers the opportunity to actively use monetary policy instruments to boost growth figures. However, the use of monetary policy tools to stimulate the domestic economy might still be quite limited in the second half of the year due to the depreciation pressure on the Georgian lari (and pressure on the price levels) caused by the currency crisis in Turkey and the marked depreciation of the Russian ruble.

The credit expansion contributed to an increase in the amount of currency in circulation. All of the monetary aggregates, including the largest - Broad Money (M3) - experienced significant yearly growth (M3 aggregate rose by 15%). The largest increase was observed for Monetary Aggregate M2, which went up by 19% relative to the same month in the previous year. Our model’s outcomes confirm the standard textbook result that a marked increase of monetary aggregates positively contributes to real GDP growth in the short run.

Last, one of the most important factors contributing to the real GDP forecast is the accumulation of national currency deposits in the commercial banks. The total deposits in commercial banks amounted to 21.8 billion lari by the end of July – 21.6% higher than in the same period of the previous year. In particular, the stock of national currency deposits grew substantially, by 42%, while the stock of foreign currency deposits increased by only 11%. As a result, deposit dollarization fell by 2.99 percentage points yearly and 0.1 percentage points monthly, and amounted to 61.1%. Rapid accumulation of deposits, as well as reduced deposit dollarization, had an appreciable positive contribution to our GDP growth projection.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including the GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych