Construction Falters, While the External Sector Continues to Improve in September 2018

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the fourth quarter of 2018. Here are the highlights of this month’s release:

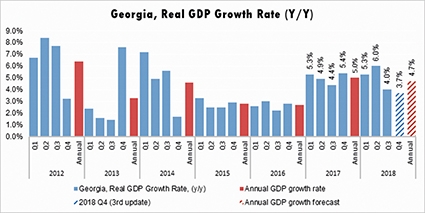

Highlights

o Recently, Geostat has released its preliminary estimate of real GDP growth for the third quarter of 2018. The Q3 growth rate now stands at 4.0%, which is 3.2% below the ISET-PI’s last forecasted value. As a result, the estimated real GDP growth for the first nine months of 2018 amounted to 4.9%.

o ISET-PI revised its forecast of real GDP growth for the fourth quarter of 2018 to 3.7% - down from 6.4% in October.

o Based on September’s data, we expect annual growth in 2018 to be 4.7%. This number is in line with the IMF’s growth forecast for 2018, but behind the NBG’s growth projections for the same period. Despite the fact that NBG’s forecast of real GDP growth for 2018 remained unchanged at 5.5%1, IMF has cut its economic growth forecast for Georgia from 5.5% to 5.0%. The revision occurred in the wake of economic difficulties in the region and the pending (or already enacted) credit restrictions2 which have put pressure on consumption and investment.

According to Geostat’s recent release, the official estimate for the third quarter of 2018 (based on VAT taxpayers’ turnover data) now stands at 4.0%. The newly estimated Q3 figure was substantially lower than initially anticipated by our forecast. Consequently, the ISET-PI Q4 forecast has also been revised downward to 3.7%. Thus, the revision of the forecast has to do with the update of the Q3 growth estimate rather than any significant changes in the model’s core explanatory variables. Yet, a few variables in the model did change substantially, both in annual and in monthly terms.

Growth in the Manufacturing and Financial Sectors

According to the Geostat, the manufacturing and financial sectors were the most important contributors to Q3 real GDP growth. It is notable that an increase in manufacturing translated into an increase in exports of these goods to the partner countries. For example, the export of Ferro-alloys and Copper Ores and Concentrates went up by 23.3%3 and 21.1% respectively in the third quarter of 2018, as compared to the same quarter of the previous year. Moreover, manufacturing goods were the main contributors to total merchandise exports in Q3 of 2018 and thus, positively affected growth projections in our model.

The output of the banking sector in the third quarter of 2018 grew by 18.4% compared to the same quarter of the previous year. Notably, the sound and profitable4 banking sector continues to support the domestic economy by issuing credit and financing domestic consumption and investment spending. The total volume of deposits (the main source of credit for banks) went up by 18.2% annually in September. This includes domestic and foreign currency deposits, which grew by 28.0% and 13.1% respectively5 compared to the same month of the previous year.

Before the introduction of the second wave of the restrictive credit regulations, the total volume of commercial banks’ loans to the national economy increased by 22.8% relative to the same month of the previous year. Moreover, the amount of loans issued to the industrial sector went up by 31.1% annually in September, while lending to the hospitality and the transport and communication sectors were up by 45.6% and 85.3% respectively. Domestic credit expansion contributed to the growth of money supply and real GDP growth. However, further credit expansion could be limited by the planned restrictive credit measures. According to the Banks Association, the new credit regulations are expected to reduce credit portfolios by 4.5-5% and the real GDP growth by 3% (0.8% as estimated by NBG).

Growth in Hotels and Restaurants, and Transport and Communication Sectors

According to the Geostat, the other sectors that contributed substantially to the real GDP growth were the hotels and restaurants, and transport and communications. The rapid development of these sectors was due to the increased number of international visitors, in particular tourists. The number of international visitors to Georgia increased by 5.7% in September compared to the same month of the previous year, while the number of tourists went up by 9.1% annually and accounted for 70.8% of all international visitors. According to the model, tourism made a significant positive contribution to the GDP growth forecast.

External Trade Improves, while the Construction Sector faces Problems.

Despite the deterioration of economic conditions in the wider region – especially the currency crisis and the economic downturn in Turkey along with the depreciation of the Russian ruble – Georgia’s external statistics continue to improve. Notably, exports grew by 17.1% year-over-year in September of 2018 and were driven by significantly larger exports/re-exports of motor cars to Azerbaijan, increased exports/re-exports of copper ores and concentrates to China, and recovered exports of ferroalloys to Russia. Georgian exports to Turkey, however, declined by 27.4% in Q3 of 2018 as compared to the same quarter of 2017. This was mainly due to the lari appreciation against the Turkish lira and the deterioration of economic conditions in Turkey (these factors could be considered as a major threat to Georgia’s real GDP growth going forward). During the same period, imports increased by 3.3%. The trade deficit thus improved by 4.9% compared to the same month in 2017 and reached 409.73 million USD. The improved trade statistics positively contributed to the growth projections.

The sector that made a substantial negative contribution to the growth forecast was the construction sector. The number of permits given to construction companies during January-September of 2018 was down by 4.6% yearly. The new credit regulations are expected to further constrain the construction sector and negatively contribute to the growth forecast.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.

1 According to the NBG’s monetary policy report, exports, consumption, and investment are expected to contribute to real GDP growth positively over the course of 2018.

2 The second wave of credit regulations was expected to enter into force by November 1st, 2018m but due to some technical issues the regulations were postponed by several days.

3 It is notable that the export of Ferro-allays to United States around doubled in yearly terms.

4 The ROA and ROE of the banking sector increased by 0.1 and 0.7 pp. respectively in September.

5 The same growth rate for contraction and trade were 17.8% and 19.1% respectively.

By Davit Keshelava and Yasya Babych