Georgia’s GDP Growth Softens at Year-End, Exports & Tourism Up

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the fourth quarter of 2018 (final update), and the first quarter of 2019. These are the highlights of this month’s release:

Highlights

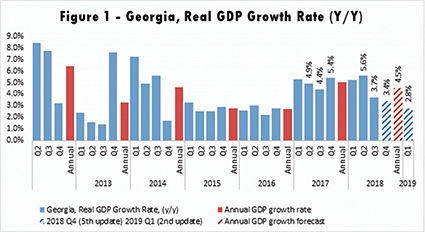

• Geostat updated its preliminary estimate of real GDP growth for the third quarter of 2018. The Q3 estimate was revised downward to 3.7% (0.3 percentage points lower than the previous estimate).

• The real GDP growth rate reached only 2.2% year-on-year for November 2018. Consequently, the estimated real GDP for the first eleven months of 2018 was revised downward to 4.7%.

• ISET-PI’s real GDP growth forecast for the fourth quarter of 2018 was reduced to 3.4%.

• Based on November’s data, annual growth in 2018 is expected to be 4.5%.

• According to the most recent (second vintage ) forecast for 2019, the growth rate in the first quarter is expected to be 2.8%.

• The National Bank of Georgia’s forecast for real GDP growth in 2018 remained the same at 5.5%, while the World Bank predicts 5.3% growth. It is notable that NBG has maintained the growth forecast at 5% for 2019. This number coincides with the WB’s recent estimate.

In the ISET-PI GDP forecast model, very few variables changed in a meaningful way between the months of October and November. The most significant changes were observed for variables related to national and foreign currency deposits, monetary aggregates, the real effective exchange rate, and external sector statistics.

National and Foreign Currency Deposits, Monetary Aggregates

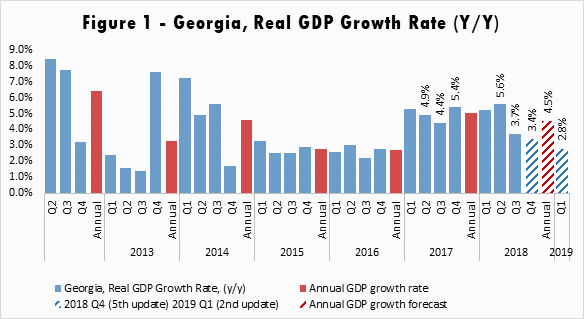

The first set of variables that have had a significant positive effect on our forecast relate to national currency deposits in commercial banks. In November, all types of national currency deposits experienced double-digit growth in annual terms. In particular, the national currency total deposits increased by 20% in yearly terms. The main contributors to this growth figure were national currency time deposits (12 percentage point increase) and national currency demand deposits (6 percentage point increase).

Moreover, national currency deposits allocated by legal entities also increased by 16% yearly, while short-term and long-term deposits of legal entities increased by 42% and 34%, respectively. According to our model, these variables have a significant positive contribution to estimated GDP growth. Such a significant increase in deposits by legal entities can be in part due to changes in the tax code (as a consequence of the corporate income tax reform which came into effect in 2018). This reform effectively increased the amount of liquidity available to firms by shifting the timing of profit tax.

In contrast to domestic currency deposits, all types of foreign currency total deposits increased moderately by 4% compared to the same month the previous year. Moreover, foreign currency current accounts had a negative contribution to this growth figure (-3 percentage points), while time and demand deposits accounted for 3 and 4 percentage points of the growth in foreign currency total deposits. In addition, foreign currency total deposits allocated by legal entities went down by 10% yearly - short-term deposits were reduced by 6%, while long-term deposits increased by 14%. As a result, deposit dollarization was reduced to 64%, compared to 67.5% in the same period of the previous year. According to our model, the trends in foreign currency deposits put a downward pressure on overall economic growth.

In addition, all the monetary aggregates, including the largest - broad money M3 (9% increase YoY) and M2 (14% increase YoY) – continued the upward trend. Moreover, currency in circulation (CCIR) increased by 9% in yearly terms. Improved monetary statistics positively contributed to the growth estimates.

Improved external statistics

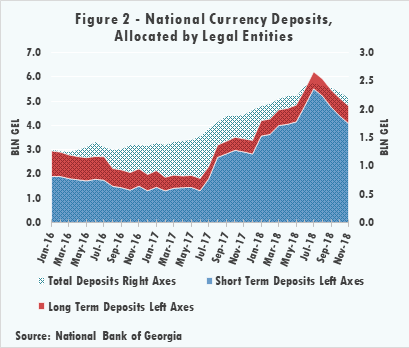

After a rapid recovery period, Georgia’s neighboring countries are struggling to maintain high growth rates. In November, the Armenian economy advanced by only 3.6%, yearly, while the real GDP of Azerbaijan increased by only 1% compared to the same month of the previous year. According to the Eurasian Development Bank (EDB), Armenia’s economic growth will continue to slow down, but will remain at a rather high level of 5.9% at the end of 2018. In addition, the main reasons for the GDP growth slowdown were a decline in agricultural production caused by unfavorable weather conditions and a decrease in ore mining due to increased requirements for compliance with environmental standards .

The State Statistics Committee of Azerbaijan claims that in the first three quarters of 2018, growth was observed in all sectors of the economy except construction (the construction sector decreased by 15.9% yearly in January-September 2018) . The Russian economy was up by 1.8% in November, however, government officials expect a slowdown in the first quarter of 2019 due to the volatility of financial markets, sanctions and a devalued ruble which puts further pressure on the inflation rate . Lastly, Turkey’s economic growth is expected to hit 2.8% for 2018 with record-high inflation and the lingering effects of a currency crisis. The main contributor to the positive growth figure in Turkey was high positive net exports .

Another set of variables which had a significant positive effect on our GDP growth forecast was related to external trade. Georgia’s exports continued to expand, increasing by 19.6% yearly in November (the main contributors were growth in export of motor cars, cigarettes, and cigars to Azerbaijan), while imports shrunk by 3.1% (due to reduced imports from Azerbaijan, the EU and China). As a result, the trade deficit declined by 13.3% year-on-year and amounted to 454.7 million USD. Furthermore, other external variables, such as remittances (9% increase), number of international visitors (5.8% increase) and tourism (14% increase) maintained their growing trends in November.

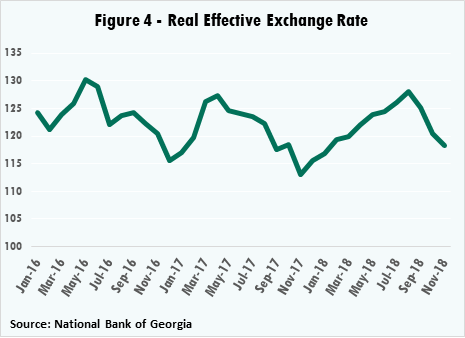

Real Effective Exchange Rate

The Georgian lari appreciated against the majority of trading partner currencies in November. The most significant appreciation was observable with respect to the ruble (2% in monthly and 14% in annual terms), euro (1% in monthly and 5% in annual terms) and US dollar (0.5% in monthly and 1% in annual terms). Furthermore, the lari appreciated against the Turkish lira by 24% in yearly terms, but depreciated by 7% in monthly terms. In addition, the real effective exchange rate (REER) depreciated by 1.7% relative to the previous month, and appreciated by 4.6% relative to the same month in the previous year. Notably, the NBG purchased 20 million USD worth of foreign exchange reserves in November (which may have contributed to the slight weakening of the national currency in monthly terms). Overall, REER-related variables had a small negative contribution to the real GDP growth projections.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych