It’s Russia, Stupid!

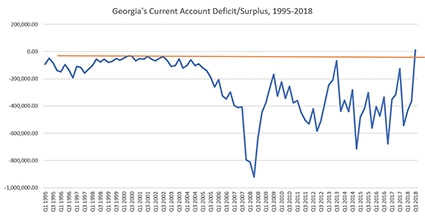

The red headline in last week’s “Georgian Weekly Market Watch” by Galt & Taggart was something of a shock: “Georgia recorded its first ever quarterly current account surplus since 1995.” Mind you, Georgia’s current account was far from positive before 1995 either. Until then, Georgia simply had not maintained a balance of payments records worthy of the name.

The G&T headline referred to Georgia’s achievement in a single quarter, Q3 2018, in which the country’s current account balance reached positive USD 11.9 million, compared with negative USD 124.9 million in Q3 2017. And even though it is about a single quarter, this achievement may represent a watershed event in Georgia’s economic history.

Why is this important, you ask? Well, a current account surplus implies that the country is no longer borrowing from the rest of the world in order to finance its consumption. Put differently, in Q3 2018, Georgia received more revenues from exports, foreign aid, and money sent home by Georgian workers abroad (“remittances”) than it spent on imports and interest payments to foreign lenders. Thus, the country was left with extra foreign currency reserves, which, in turn, improved its monetary position, and strengthened investors’ confidence in the Georgian economy.

FREE TRADE AGREEMENTS WORKING IN GEORGIA’S FAVOR?

One possible explanation for the upswing in Georgia’s current account balance is the country’s success in leveraging the free trade agreements it has signed in recent years with the European Union (the so-called Deep and Comprehensive Free Trade Area agreement, or DCFTA) and the European Free Trade Association (EFTA), consisting of Iceland, Liechtenstein, Norway, and Switzerland.

Let us examine the data. According to GeoStat, Georgia’s total exports in 2018 stood at USD 3.362 billion, an increase of 22.9% year-over-year. Our leading export products were copper ores, beverages, ferro-alloys, pharmaceuticals, and tobacco. Contrary to our logic, however, the share of EU in total exports comprised only 22%, a two-percentage point decline relative to 2017. In the meantime, the share of Russia and CIS in Georgia’s total exports increased from 43% to 50%.

Moreover, instead of improving, Georgia’s trade balance with European markets has actually worsened. Net exports of goods covered by DCFTA and EFTA agreements, for example, dropped from negative USD 978.7 million in Q3 2017 to negative USD 1,004.5 million in Q3 2018. Thus, Georgia has become more of a net importer from Europe since the previous year and has only slightly improved its position since Q3 2014 when net exports of goods stood at negative USD 1,099.8 million.

The DCFTA agreement with the EU and EFTA are worth further scrutiny. Of Georgia’s total exports to the EU, only about 11% were foodstuffs and agricultural products that can be said to have directly benefited from the DCFTA. Exports to Europe are dominated by copper ores, beverages, gold, and nitrogen fertilizers. Most of these products could be exported to Europe custom-free under the GSP+ regime which Georgia enjoyed since late 2000s.

While growing in value, food and agricultural exports to Europe are not having a great impact on Georgia’s current account or its economic development. The country was able to penetrate the (Eastern) European market with some of its premium wines and mineral waters, but it had no success whatsoever with animal products, including the much touted Georgian honey, which at some point was thought to have the potential to “sweeten Tbilisi’s EU dream”.

The reasons for Georgian failure in this regard are quality and consistency of supply, on the one hand, and price competitiveness, on the other. Georgian mandarins, to take one example, are more expensive than their Spanish equivalent, and their flavor and visuals are not suitable for the European market. Georgian milk or meat products are not produced in sufficient quantity to supply even the local Georgian market, and are way too expensive for European consumers.

Georgia is competitive in the production of nuts, which were the greatest early success story of Georgia-EU economic relations in 2014 and 2015. Since then, however, hazelnut production has been decimated by the infamous “marmorated stink bug”. In the first 10 months of 2018, hazelnut exports to Europe decreased by 16.5 percent, after a whopping 64% drop in 2017. What’s more, as reported by JAM news, in November 2018, “Russia replaced the European Union as the main destination for Georgian hazelnut exports.”

Exports to Russia and other CIS countries did contribute to balancing Georgian current account. As these countries recover from the crisis of 2014-2016, they are able to absorb a larger share of Georgian traditional products, such as wine, mineral water, fruit, greens and vegetables. But is it necessarily a good thing?

IT’S TRADE IN SERVICES!

As we have seen, Georgia’s success in balancing its current account in Q3 2018 cannot be attributed to any breakthroughs in customs-free exports of agricultural or any other products to Europe. The country is still very far from becoming a modern agriculture paradise or an export platform for manufactured goods. In fact, the main driver of Georgia’s current account surplus – and of the Georgian economy as a whole – is exports of services, not products.

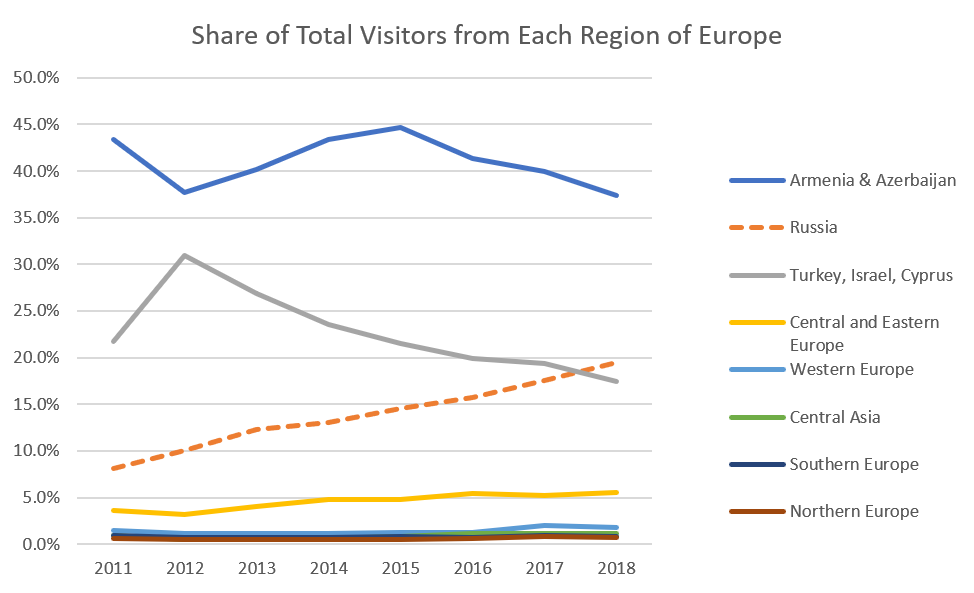

A closer inspection of the structure of the current account shows that the positive trade balance in services is actually mostly due to the USD 1.2 billion inflow from the travel and tourism sectors, which constitutes a 12.3% increase year-over-year. According to the Georgian National Tourism Administration, the number of international visitors increased by 720,520 people in 2018. Of these extra visitors, 37 percent were from Russia, while 35 percent were from Azerbaijan, Turkey, and Israel, combined.

EVERY CLOUD HAS A SILVER LINING

The great news about Georgia being able to balance its current account (even if only in a single quarter) comes with serious questions concerned with the manner in which this feat has been achieved. Instead of product and market diversification, the Georgian economy appears to be increasingly dependent on one particular sector of the economy – tourism and hospitality. Instead of reaching out to new markets, Georgia follows the easy road to its traditional buyers in Russia and other CIS countries.

Such development comes with serious risks. The Georgian economy cannot afford to put all of its eggs in the Russian basket. Any shocks to the Russian economy, such as recessions, financial crises, or political sanctions, can have adverse effects on the Georgian current account and push the economy back into the net borrower position from which it has barely escaped.

By Eric Livny and Rezo Surguladze