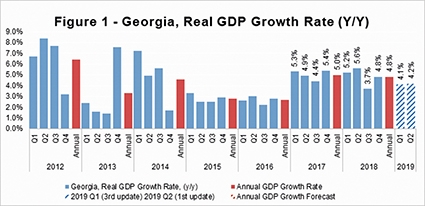

First Predictions: Georgia’s Real GDP Expected to Grow by 4.4% in 2019

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the first and second quarters of 2019. These are the main features of this month’s release:

• Geostat has published its rapid estimate of real GDP growth for the fourth quarter of 2018, and their estimated growth stands at 4.8%, which is 1.1 percentage point above ISET-PI’s most recent forecast.

• Utilizing the latest data, real annual GDP growth in 2018 amounted to 4.8%. It is notable that by March of 2018, our model predicted 4.8% real growth in the “middle-of-the-road” scenario that now perfectly coincides with the official statistics. Moreover, our annual GDP forecasts of 4.7% (since November) and 4.6% (since December), equally were revealed to be quite accurate.

• ISET-PI’s forecast for the first quarter of 2019 now stands at 4.1% - up from 3.1% in January. The second quarter growth forecast currently stands at 4.2%.

• Based on the data from December, we expect annual growth in 2019 to be 4.1% in the worst-case scenario, and 5.2% in the best-case or an average long-term growth scenario. Our middle-of-the-road scenario (based on the average growth in the last four quarters) predicts a 4.4% increase in real GDP.

Expected growth in Q1 2019 has risen, and ISET-PI’s forecast for real GDP growth for the first quarter of 2019 was upwardly revised by 1.0 percentage point. This change is resultant on two factors: firstly, Geostat’s newly released growth figures for the fourth quarter of 2018 was 1.1 percentage point higher than ISET-PI’s most recent forecast. Secondly, rapidly increasing national currency deposits, continuing monetary growth, and a notably improved trade balance have all contributed to buoyant expectations.

Rapidly increasing national currency deposits

The first set of variables with a significant positive effect on our forecast relate to national and foreign currency deposits in commercial banks. In December, all national currency deposits experienced double-digit growth in annual terms. In particular, the national currency demand deposits saw an annual increase of 28%. Additionally, the national currency time deposits increased by 27.5% annually. The main contributors to this growth were national currency deposits with a maturity of less than 1 month (19.9 pp.) and national currency deposits with a maturity greater than 12 months (8.8 pp.). Consequently, national currency total deposits increased by 23% yearly. It worth mentioning that in just December the Georgian government placed 550 million national currency deposits with a maturity of 1 month in domestic commercial banks.

In contrast to domestic currency deposits, foreign currency total deposits increased relatively moderately by 10.5% compared to the same month of the previous year. Furthermore, foreign currency demand and time deposits increased by 19.2% and 11.5% yearly, respectively. Deposit dollarization was reduced to 63.1, compared to 65.6 in the same period of the previous year. According to our model, the trends in national and foreign deposits have had a significant positive contribution to real GDP growth.

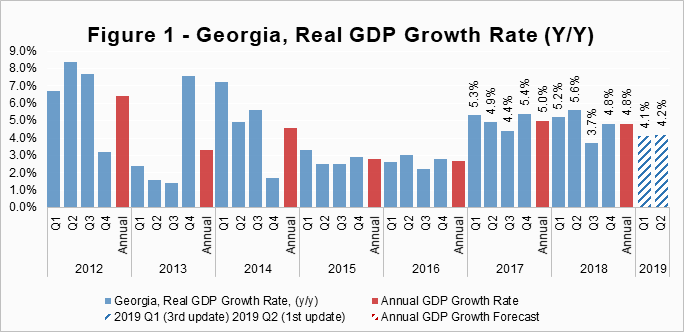

Continuing monetary growth

Monetary aggregates are another set of variables that have had a significant positive effect on our forecast. As of December, the monetary policy committee of the National bank of Georgia (NBG) decided to leave its monetary policy rate (MPR) unchanged. NBG follows a slow normalization process in its monetary policy, as the risks remain in the external sector, which could potentially have a negative impact on Georgian inflation. However, all of the monetary aggregates experienced reveal notable yearly increases, including currency in circulation (4.1% monthly and 7.8% yearly) and broad money (M3) (6.7% monthly and 14.7% yearly).

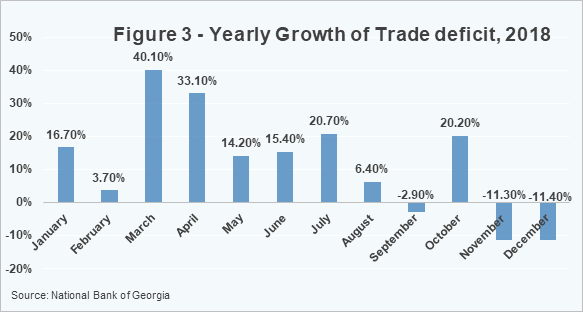

Notably improved trade balance

The final variables which have had a substantial positive effect on the predicted real GDP growth are related to the external sector. Georgian exports continued to expand, increasing by 14% yearly in December 2018, while imports shrunk by 2.7% yearly. As a result, the trade deficit declined by 11.4% yearly to 488.1 million USD. Furthermore, the re-export of automobiles, the exports of cooper ores and concentrates, and Ferro-alloys were the main contributors to the growth in export. While other external variables, such as remittances (9.1% increase), the number of international visitors (0.2% increase) and tourism (11.6% increase), maintained their growth trends in December. Our model reveals that external sector variables have had a positive contribution on real GDP growth projections.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (the 1st vintage) is available about five months before the end of the quarter in question. The last forecast (the 5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych