CA Balance & Capital Investments to Outweigh Pessimism/Lack of Credit?

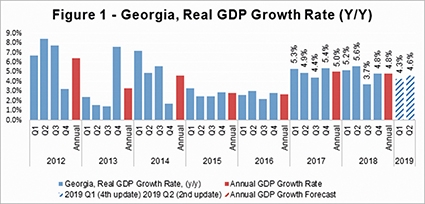

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the first and second quarters of 2019. These are the main features of this month’s release:

Highlights

• ISET-PI’s forecast of real GDP growth for the first quarter of 2019 stands at 4.3%. The second estimate of second-quarter growth forecast now stands at 4.6%.

• Based on January’s data, we expect annual growth in 2019 to be 4.4% in the worst-case or “no growth” scenario, and 5.5% in the best-case or “average long-term growth” scenario. Our “middle-of-the-road” scenario (based on average growth over the last four quarters) predicts 4.7% real GDP growth.

• ISET’s annual forecast is consistent with evidence coming from the National Bank of Georgia (NBG) and international development institutions. For example, the National Bank of Georgia’s expectation for real GDP growth remained unchanged at 5% in 2019. According to the recent monetary policy report, improved net export, enhanced consumption, and investment supported by government capital spending and moderate credit activity growth will positively contribute to real GDP growth . Moreover, the International Monetary Fund (IMF) has also decreased its growth forecast from 4.78% (estimated in October) to 4.6% in 2019. The IMF provided similar findings to the National Bank of Georgia, identifying some contributors to the real GDP growth: improved current account balance and the government’s high infrastructural spending. However, this authoritative institution identified threats coming from the recently introduced credit regulations and unstable economic conditions in the region.

Recently, Geostat published its rapid estimate of real GDP growth for January of 2019 and the estimated growth figure stands at 3.5%. The trade (mainly due to increased re-export of motor cars), hotel and restaurant, financial (mainly due to interest income obtained by commercial banks) and real estate sectors were the most important contributors to the real GDP growth in January, while the manufacturing and construction (mainly due to the notably reduced number of residential and commercial buildings built by construction companies ) sectors had a negative impact on the growth figure. Based on the available data, one can conclude that the main (negative and positive) drivers of the real GDP growth for 2019 were improved external statistics, expansionary monetary policy and increased monetary aggregates, deteriorated consumer and business confidence and restricted credit expansion.

External Factors – Threats and Opportunities

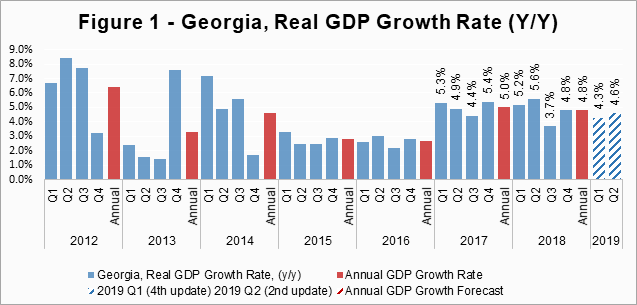

In 2018, economies throughout the region enjoyed moderate growth – the Armenian economy reached 5.8% annual growth, down from an impressive 7.5% in 2017. Russia advanced by 2.3%, which further stimulated the Georgian and Armenian economies through the trade, remittances, and tourism channels. Moreover, Azerbaijan is still far behind its peer countries, with an average annual growth rate of 1.4% in 2018. Kazakhstan, Belarus, and Ukraine advanced on average by 4.1%, 3.0% and 3.3%, respectively. There is still no data available on annual GDP growth for Turkey. However, Turkey’s economy shrunk notably in the third quarter of 2018 followed by a deterioration of consumption and business confidence that has already had negative consequences on Georgia’s economy (see Figure 2). Thus, economic and political instabilities of the countries situated in the wider region are potential external threats to the Georgian economy that might not be taken into consideration in our model yet.

In January 2019, exports grew by 7.2% year on year and this growth figure was mainly driven by significantly increased exports/re-exports of motor cars, cigarettes, and cigars to Azerbaijan recovered exports of wine and mineral waters to Russia and re-export of motor cars to Armenia. However, Georgian exports to Turkey, China (caused by reduced re-export of copper ores and concentrates) and the EU (due to decreased export/re-export of mineral or chemical fertilizers to Lithuania and decreased re-export of petroleum oils to France) experienced a notable decline. During the same period, imports decreased moderately by 1.1%. The trade deficit thus shrank by 6.1% compared to the same month in 2018 and reached 349.2 million USD. Overall, the reduction in the trade deficit made a significant positive contribution to the real GDP growth forecast.

Remittances and tourism, together with foreign direct investment (FDI), are among the main sources of foreign funds coming into Georgia. In January, remittances increased by 5.5% relative to the same month of the previous year. Once again, the main contributors to this growth were the USA, EU, Azerbaijan and Israel, while the reduction of money inflow from Turkey (-1.8 pp.) and Russia (-3.0 pp.) had a negative impact on the growth estimation. Regarding the number of visitors, Georgia experienced a 0.6% reduction in yearly terms. However, inbound tourism increased by 5.9% year on year. As Georgia is among those countries in which remittances and income from tourism form an important part of households’ income, their growth had a positive impact on the projected real GDP.

Internal Factors – Threats and Opportunities

Annual inflation in January 2018 constituted 2.2%, which was in line with the 3% NBG target. In addition, annual inflation on imported goods came down to 2%, while the core inflation rate stood at a low 0.6%. Low and stable inflation usually gives policymakers the opportunity to actively use monetary policy instruments to boost growth figures. Thus, the Monetary Policy Committee of the NBG met on January 30, 2019, and due to the reduced macroeconomic risk coming from the external sector and weak inflationary pressure from the aggregate demand, they decided to reduce the Monetary Policy Rate (MPR) by 0.25 percentage points to 6.75. This was the first time since July 2018 that the National Bank of Georgia conducted an expansionary monetary policy by reducing the policy rate. In addition, NBG has purchased foreign exchange in the amount of $85 million to improve its ratio of reserves/ARA metric .

In addition, nearly all of the monetary aggregates have experienced double-digit growth relative to the same month of the previous year. In particular, the largest M3 and M2 aggregates increased by 15.3% and 16.0% respectively in yearly terms, while the most liquid Currency in Circulation (CCIR) went up by 8.4% year on year (it is notable that monetary aggregates experienced a monthly reduction in January, as usual). According to economic theory, increased money supply encourages business expansion and consumer spending, which leads to a rise in aggregate demand.

Worsened business and consumer confidence were among the negative contributors (threats) to the real GDP growth forecast. According to ISET-PI’s latest publication of the quarterly Business Confidence Index (BCI), the index dropped by 7.4 percentage points in the first quarter of 2019 relative to the previous quarter (it is notable that the index deteriorated in yearly terms as well). The BCI drop was driven by a worsening in past performance and expectations in a number of business sectors. Interestingly, companies in the construction industry assessed their past performance most pessimistically, however, they display the most optimistic expectations. While private sector expectations tend to worsen, they continue to remain positive (see: http://iset-pi.ge/index.php/en/business-confidence).

In addition, in January 2019 ISET-PI’s Consumer Confidence Index (CCI) dropped insignificantly, by 1.1 index points monthly (but increased slightly yearly). While the reduction in the expectations index (by 5.3 points) – measuring expectations for the coming 12 months – outweighed the growth of the present situation index (by 3.1 points). People’s pessimism can be explained by January’s overconsumption and negative expectations related to unemployment, inflation, and the general economy (see: http://iset-pi.ge/index.php/en/consumer-confidence-index/2344-january-2019-post-christmas-hangover).

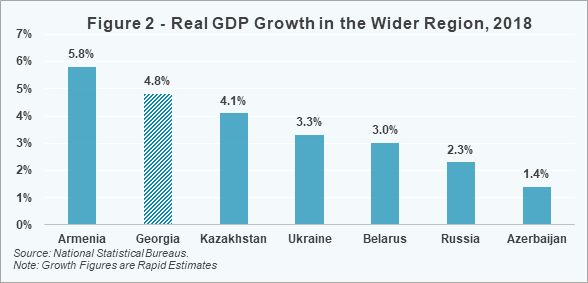

Lastly, new lending regulations could potentially have a negative impact on growth predictions. The first wave of regulations entered into force in May 2018. This regulation has introduced a ceiling of 25% of a commercial bank’s supervisory capital for loans issued without a prior comprehensive analysis of a consumer’s solvency. The second wave of more restrictive regulations has been in force since January 2019 (decree was mandatory for institutions which issue loans to individuals). The new regulation introduced principles of responsible lending, made solvency analysis necessary, and defined required payment-to-income (PTI) and loan-to-value (LTV) ratios such that the difference between the debtor’s net income and the loan is not less than the subsistence minimum . These regulations notably restricted credit expansion and have had negative implications on the growth figure. However, it is hard to capture the negative impact of the credit restrictions to GDP growth, as only one month has passed since the government introduced these more restrictive measures. Therefore, credit restrictions might be considered potential internal threats to the real GDP growth figure that might not be fully taken into consideration in our model yet.

In January 2017, Total Volume of Commercial Bank’s Consumer Credit decreased by 2.4% compared to the previous month and increased by only 4.2% relative to the same month of the previous year. The Credit Volume of Commercial Banks' Short Term Consumer Credits reduced by 50.7% and 57.7% in monthly and yearly terms respectively. Moreover, the main driver of this negative trend is Consumer Loans in National Currency, which decreased by 56.4% and 64.4% in monthly and yearly terms correspondingly . In contrast, the Credit Volume of Commercial Banks' Long Term Consumer Credits increased by 5.1% and 16.7% in monthly and yearly terms respectively. Overall, the consumer credit related variables had a slight negative impact on the growth forecast.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (the 1st vintage) is available about five months before the end of the quarter in question. The last forecast (the 5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych