No Credit, No Party! How to Guarantee Stable Growth

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the first and second quarters of 2019 and these are the main features of this month’s release:

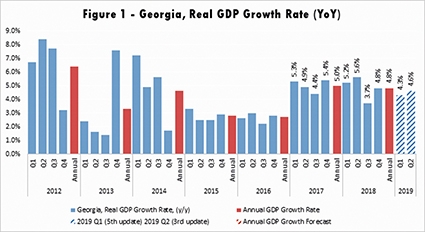

Highlights

• ISET-PI’s forecasted real GDP growth for the first two quarters of 2019 remain at 4.3% and 4.6%, respectively.

• Geostat has released its rapid estimate of real GDP growth for February 2019. Their estimated growth stands at 4.6%, while the average real GDP growth for January-February 2019 reached 4.1%.

• Based on February’s data, we expect 2019 annual growth to be 4.4% in the worst-case or “no growth” scenario, and 5.5% in the best-case or “average long-term growth” scenario. Our “middle-of-the road” scenario (based on the average growth over the last four quarters) predicts 4.7% real GDP growth.

Based on data from February 2019, our forecast for the first two quarters of 2019 has not changed significantly. The majority of explanatory variables in our model have remained quite stable throughout February. The most meaningful changes were observed in those variables related to the Deposits of Various Maturities in Commercial Banks, Monetary Aggregates, Consumer Credit and the External Sector.

National Currency Deposits of Various Maturities in Commercial Banks

The first set of variables with a significant positive contribution to the real GDP forecast relate to national currency deposits within commercial banks. The stock of total deposits in commercial banks amounted to 22.9 billion GEL by the end of February - 19.5% higher than in the same month of the previous year. The stock of national currency deposits, in particular, grew by a notable 19.3%, while the stock of foreign currency deposits increased by 14.8%. The largest yearly increase was observed for time deposits in the national currency with less than 3 months and greater than 12 months maturity, which, compared to the same month of the previous year, increased by 53.1% and 31.9%, respectively.

Additionally, the dollarization rate of commercial bank deposits decreased by 0.2 percentage points compared to the previous month, equaling 62.3% in February 2019. Dollarization deposits reached 74.8% and 53.1% correspondingly for individuals and legal entities. Therefore, the variables related to national currency deposits had a positive contribution to our GDP projections.

Monetary Aggregates and Consumer Credit

The other set of variables that had a significant positive effect on our forecast are related to monetary aggregates. All monetary aggregates, including the largest, Broad Money (M3), and the smallest, Narrow Money (M0), experienced significant yearly growth - 18.2% and 10.3%, respectively. Moreover, currency in circulation increased by 13% yearly. It is notable that the National Bank of Georgia (NBG) bought 101.3 million USD of foreign currency reserves in February. Furthermore, the Monetary Policy Committee of NBG met in March and decided to reduce the monetary policy rate by 0.25 percentage points to 6.5% (expansionary monetary policy), which is expected to further increase the money supply in the future. Rapid expansion of monetary aggregates has positively contributed to the growth forecast.

As we mentioned in our previous report, new lending regulations could potentially have a negative impact on short-term growth predictions. In February 2019, the Total Volume of Commercial Banks’ Consumer Credit increased by only 0.2% monthly and 3.5% yearly. However, the Credit Volume of Commercial Banks' Short-Term Consumer Credits reduced by 1.3% and 59.3% in monthly and yearly terms, respectively (the main driver behind this negative trend being consumer loans in the national currency). Whereas, the Credit Volume of Commercial Banks' Long-Term Consumer Credits increased by 0.3% monthly and 16.4% yearly. Overall, the variables related to consumer credit have had a slightly negative impact on the growth forecast.

The External Sector

The final variable which has had an extensive, positive impact on the predicted real GDP growth is related to external sector statistics. Georgian exports continued to expand, increasing by 19.0% yearly in February, while imports developed by only 0.6% annually. Consequently, the trade deficit declined by 9.3% yearly to 376.5 million USD. Moreover, other important external sector variables, such as remittances (10.2% increase) and the number of tourists (5.1% increase) maintained their growth trend, while the number of international visitors reduced moderately by 1.2%, compared to the same month of the previous year. Our model revealed that external sector variables had a significant and positive effect on the real GDP growth projections.

Foreign Direct Investment, however, shrunk by 62.3% in the fourth quarter of 2018, compared to the same month of the previous year. According to the preliminary data, released by the National Statistics Office of Georgia (Geostat), the key reasons behind decreasing FDI were the completion of a pipeline project (implemented by British Petroleum), transferring ownership to some companies from non-resident to resident units, and the reduction in liabilities to non-resident direct investors. Furthermore, the economic sectors chiefly depressing FDI growth were transport and communication (-18.5 ppt), construction (-15.4 ppt), and energy (-11.4 ppt), where the only sectors that positively contributed to growth were hotels and restaurants (+2.1 ppt), and agriculture and fishing (+0.4 ppt). Due to data limitations (FDI statistics are published quarterly with a notable time lag), we are not able to take the FDI data into consideration in our econometric model. Therefore, the notably deteriorated FDI inflow might cause considerable downward pressure on our forecasted values.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (the 1st vintage) is available about five months before the end of the quarter in question. The last forecast (the 5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych