Georgian Economy Strong, Inflation Low, Short-term Consumer Credit Declines

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the second quarter of 2019. Here are the highlights of this month’s release:

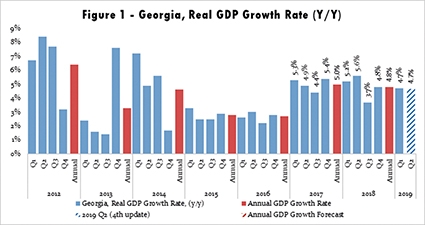

Highlights

• Geostat has released its GDP growth estimate for the first quarter of 2019. The Q1 growth stands at 4.7% , which is only 0.4 percentage points above the recent ISET-PI forecast.

• ISET-PI’s forecast of real GDP growth for the second quarter of 2019 stands at 4.7% - up from 4.6% in April.

• Based on March data, we expect annual growth in 2019 to be 4.6% in the worst-case or “no growth” scenario, and 5.6% in the best-case or “average long-term growth” scenario. Our “middle-of-the road” scenario (based on average growth over the last four quarters) predicts 4.9% real GDP growth in 2019.

• According to the recent Monetary Policy Report (May 2019), the National Bank of Georgia’s (NBG) forecast of real GDP growth remained unchanged at 5% in 2019. According to NBG, annual real GDP growth this year will be driven by improved trade balance, and increased consumption and investment spending supported by capital expenditures of the government and a moderate growth of loans.

According to Geostat’s recent release, the official estimate of growth for the first quarter of 2019, which is based on VAT taxpayers’ turnover data, now stands at 4.7%. The newly estimated Q1 figure is higher than initially anticipated by the ISET-PI forecast. Consequently, ISET-PI’s second quarter forecast has also been revised upward to 4.7%. The upward revision of the forecast is due to the increased national currency deposits, continuing money supply growth in Georgia and improved external statistics. However, restricted consumer credit and depreciated real effective exchange rate put a downward pressure on the forecast value.

The Volume of Deposits Went Up in Yearly Terms

The first set of variables that have had a significant positive effect on our forecast relate to national currency deposits in commercial banks. In March, all types of national currency deposits, from the most liquid - currency in circulation (up by 18.9% yearly) - to the least liquid - time deposits with a maturity of more than 12 months (up by 31.9% yearly) - experienced double-digit growth in annual terms. The largest yearly increase was again observed for national currency time deposits with a maturity of less than 3 months, which increased by 53.1%, relative to the same month of the previous year (but decreased by 4.4% monthly). Overall, national currency total deposits increased by more than 19.3% yearly. National currency deposit-related variables had a positive contribution to our GDP growth projection.

Furthermore, the total volume of foreign currency deposits went up by 15.6% compared to the same month of the previous year. The dollarization rates of non-bank deposits and loans decreased in monthly terms in March of 2019. Dollarization of deposits fell by 0.3 ppt, amounting to 62.0% (74.7% and 52.2% for individuals and legal entities, respectively), while loan dollarization declined by 0.3 ppt to 56.5%, compared to February of 2019. According to our model, deposit dollarization had a small, but positive impact on the real GDP growth.

Monetary Aggregates Continue Path of Growth

The other set of variables that had a significant positive effect on our forecast is related to currency in circulation. The Monetary Policy Committee of the National Bank of Georgia met in May, and decided to leave the monetary policy rate unchanged at 6.5%. However, all the monetary aggregates, including the largest - broad money (M3) - experienced significant yearly growth (M3 aggregate rose by 18.3% yearly). The largest increase was observed for monetary aggregate M1 (narrow money), which went up by 20.5% relative to the same month in the previous year. Moreover, currency in circulation itself increased by 13.4% in yearly terms.

It is noteworthy that in a modern economy, the greatest proportion of a money supply is in the form of deposited currency, which is created by commercial banks - banks accumulate the savings of individuals, firms and government entities, and provide funds for investment projects and consumption that contribute to higher GDP growth. Thus, rapid expansion of monetary aggregates contributed positively to our GDP growth forecast.

Moreover, the annual inflation in March 2019 constituted 3.7%, which was only slightly higher than the 3% NBG target. It is notable that increased excise tax on tobacco (one-time factor) was the main contributor to the annual inflation rate (contributing 1.3 ppt. to the annual inflation rate). In addition, the annual core inflation stood at a low 1.2%. This is good news for the Georgian economy, as low core inflation typically translates into lower overall inflation in the future.

External Statistics Show Positive Signs

March 2019 showed strong growth in the wider region. According to the estimates for March 2019, most of the countries in the region showed significant improvement compared to the same period in the previous year. The Armenian economy reached a remarkable 7.6% annual growth. Furthermore, Russian and Azerbaijani economies advanced by 2.1% and 3% respectively (see Figure 2). Thus, improved economic conditions in the wider neighborhood stimulated the Georgian economy through trade, remittances, and tourism channels. However, economic and political instability of the countries situated in the wider region (e.g. Turkey and Iran) are potential external threats to the Georgian economy that might not be taken into consideration in our model yet.

Overall, Georgia’s external statistics continue to improve. In March of 2019, total exports grew by 12.3% year over year (slightly decelerated growth rate compared to the previous year), driven by the export/re-export of copper and copper ores (31.0% yearly), export of ferro alleys (22.5% yearly), re-export of motor cars (59.9% yearly) and export/re-export of packaged medicines (114.5% yearly).

Among the external trade developments to watch is the decline in the import of merchandise goods. In the reporting period, imports of merchandise goods decreased by 12.3%, mainly driven by petroleum and petroleum gases (declined by 37.0%). The great majority of the other main product categories experienced notable yearly increase, but still not enough to outweigh reduced import of the petroleum and petroleum gases. As a result, the trade balance improved by 25.0%, compared to the same month in 2018. It is notable that net export is improving in yearly terms since January 2019 (see Figure 3).

Furthermore, remittances and tourism, together with foreign direct investment (FDI), are among the main sources of foreign funds coming into Georgia. In March, remittances increased by 4.5% relative to the same month of the previous year. Once again, the main contributors to this growth were the United States (increased by 13% yearly, contributing 1.3 ppt to the annual growth figure), EU (increased by 18.9% yearly – Italy, Greece and France were the main drivers of this growth figure) and Ukraine (increased by 34.7% yearly), while the reduction of money inflow from Turkey (-1.9 pp.) and Russia (-2.2 pp.) had a negative impact on the growth estimation. The number of all types of international visitors in March of 2019 increased by 4.6% year over year and exceeded 619,300 people. Out of these, 65% were classified as tourists, and the growth rate of these visits reached 4.3% annually. As Georgia is among those countries in which remittances and income from tourism form an important part of households’ income, their growth had a positive impact on the projected real GDP.

Real and Nominal Exchange Rates Experienced Moderate Depreciation

The real effective exchange rate (REER) depreciated by 0.3% relative to April, and by 0.1% relative to the same month of the previous year. The depreciation of the REER is typically associated with reduced value of the domestic export in the very short-run period and gaining competitiveness of export production in the foreign markets later. Notably, the lari real exchange rate appreciated with respect to the national currencies of two major trading partners – Turkey and Russia. The GEL/TRY and GEL/RUB real exchange rates appreciated compared to the same month of the previous year by 10.9% (appreciated by 2.6% monthly) and 2.3% (depreciated by 1.5% monthly) respectively. In contrast, the lari real exchange rate experienced a slight depreciation against the US dollar and the euro (falling on average by 0.7% and 0.8% respectively in monthly terms). Overall, REER-related variables had a small negative contribution to the Q2 real GDP growth projections.

Credit Restrictions Reduced Short Term Consumer Credits

As we mentioned in our previous report, new lending regulations could potentially have a negative impact on short-term growth predictions. The average annual interest rates on the short-term consumer loans at first declined from 20.0% in December 2018 to the 12.7% in February 2019, but then increased notably to 17.5% in March 2019 (long-term consumer credit had a similar pattern). In March 2019, the total volume of commercial banks’ consumer credit increased by only 2.7% yearly and even declined by 1% monthly. However, the volume of commercial banks' short-term consumer credits declined by 59.8% in yearly terms, and increased by only 2.4% monthly (the main driver behind this negative trend being consumer loans in the national currency). Whereas, the volume of commercial banks' long-term consumer credits increased by 16.1% yearly and declined by 1.3% monthly. Overall, the variables related to consumer credit have had a slightly negative impact on the growth forecast.

By Davit Keshelava and Yasya Babych