Georgia’s Economy in May: So Far So Good, “Gavrilov Effect” Yet to Be Seen

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the second and third quarters of 2019. Here are the highlights of this month’s release:

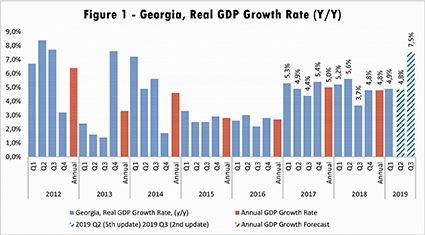

• ISET-PI’s growth projections for the second and third quarters of 2019 were revised upward by less than 0.1 percentage points. They now stand at 4.8% and 7.5% respectively.

• Geostat has increased the estimate of the average real GDP growth for the first quarter of 2019 to 4.9% (by around 0.2 percentage points).

• Recently, Geostat published its preliminary estimate of real GDP growth for May 2019, which now stands at 4.7%. Consequently, the estimated real GDP growth for the first five months of 2019 is 4.9%.

• Based on May’s data, we expect annual growth in 2019 to be 5.5% in the worst-case or “no growth” scenario, and 5.9% in the best-case or “average long-term growth” scenario. Our “middle-of-the road” scenario (based on average growth over the last four quarters) predicts 5.6% real GDP growth in 2019.

Based on the available data, the growth forecast for the second and third quarters of 2019 reached 4.8% and 7.5% respectively. These high forecast figures can be explained by the fact that quarterly growth rates typically follow a certain pattern, captured by ISET-PI’s empirical forecast model. Thus, the higher-than usual growth in the first quarter may result in an overly optimistic forecast about the next quarter’s performance. Indeed, ISET PI’s forecasts for Q2 and Q3 are largely influenced by the high Q1 actual growth. Yet, looking at the economic landscape from the standpoint of the May data, several variables changed significantly and affected growth predictions in different ways. In particular, favorable economic conditions in the neighboring countries, improved trade balance, remittances, and international tourism contributed to the overall growth projections, while higher-then-targeted inflation and restricted consumer lending dampened the growth forecast.

The beginning of 2019 showed strong growth in the wider region. According to the rapid estimates of real GDP growth, most of the countries in the region experienced significant acceleration of economic activities in the first four months of 2019. The Armenian economy advanced by 7.3% annually, while the Russian and Azerbaijani economies grew on average by 1.2% and 2.8%, respectively. Thus, improved economic conditions in the wider neighborhood stimulated the Georgian economy though trade, remittances and tourism channels.

In May 2019, Georgia’s total exports grew by 3.5% year over year (slightly decelerated growth rate compared to the earlier months of 2019), driven by the export/re-export of copper ores and concentrates (6.0 percentage points contribution to the overall export growth), higher re-exports of motor cars and packaged medicine (both accounts for 8.8 percentage points of the total export growth). Export of ferro alleys and wine to Russia, however, contributed negatively to the export statistics. The main destination markets for Georgian export products were Russia (14%), Azerbaijan (13%), Bulgaria (13%), Armenia (8%), Ukraine (7%) and Turkey (7%) accounting for 62% of total exports.

During the same period, imports of merchandise goods declined by 7.3%, driven by the import of petroleum and petroleum gases (negative contribution to the total import growth figure by around 1.1 percentage points), motor cars and telephone devices. The main trading partners of Georgia for imports were Turkey (19%), Russia (11%), China (10%), USA (6%) and Germany (5%), accounting for the 51% of total imports. As a result, the trade deficit narrowed by 14.4%, yearly to 417.7 million USD.

Both remittances and tourism showed significant yearly increases in May 2019. Money transfers surged by 11.8% in the fifth month of 2019, driven by remittances from the United States of America (1.5 percentage points), Ukraine (51.2% annual growth), European Union (28.2%) including Italy (28.4%), Greece (24.6%), and Spain (24.1%). Notably, remittances from the Russian Federation (-1.7 percentage points) and Turkey (-1.5 percentage points) experienced a slight yearly decline. Nevertheless, Russia remains the top country of origin for money inflow, accounting for 24% of total remittances. The number of all type of visitors in May of 2018 increased by 14.2% year over year. Out of these, 69% were classified as tourists, and the growth rate of these visits reached 18.0% annually. According to our model, both tourism and remittances had a significant positive contribution to the GDP growth forecast. However, From July 8th, Russia banned all passenger flights to and from Georgia, under the orders of Russian President Vladimir Putin. The „tourism embargo“ is not reflected in the data yet, but is expected to have a negative impact on real GDP growth in 2019.

On the negative side, the increase in Consumer Price Index (CPI) dampened our growth predictions. In May, the annual inflation rate reached 4.7%, which is 1.7 percentage points higher than the targeted 3%. The main contributors to the annual price increase were: excise tax on tobacco (making the excise tax equal on filtered and unfiltered cigarettes ) and increased food prices, which contributed to annual inflation 1.3 and 2.3 percentage points respectively. However, one should note that this type of tax hike (excise on tobacco) can increase only the level of prices, not the inflation rate going forward (it is a one-time factor) and it is expected to be exhausted next year. It is worth mentioning that core inflation (inflation excluding the most volatile petroleum and food prices) remains at a low level of 1.1%. Our forecasting model still identifies the inflation rate increase as a negative contributor to future GDP growth.

It is notable that we usually include Metals Price Index (PMETA) and the Agricultural Raw Materials Index (PRAWM) as explanatory variables in our forecast. The reason for adding these series is that metals form a significant share of Georgia’s exports, while food is one of the main import items. Therefore, a global increase in the price of metals should help the Georgian economy, while an increase in the price of agricultural produce is more likely to hurt it. In May 2019, metal and agriculture prices decreased by 9.4% and 3.3% respectively in annual terms. As was the case with other variables this month, the changes in these series turned out to have a very small (but overall negative) effect on our forecasted GDP growth in the second and third quarters.

As mentioned in our previous report, new lending regulations could potentially have a negative impact on short-term growth prospects. In May 2019, the total volume of commercial banks’ consumer credit increased by only 2.8% and 1.1% in yearly and monthly terms respectively. However, the volume of commercial banks' short-term consumer credits decreased by 63.7% in yearly terms (the main driver behind this negative trend being consumer loans in national currency). Whereas, the volume of commercial banks' long-term consumer credits increased by 16.9% yearly. Overall, the variables related to consumer credit have had a slightly negative impact on the current growth forecast.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (the 1st vintage) is available about five months before the end of the quarter in question. The last forecast (the 5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych