Global Slowdown & Geopolitical Tensions May Affect Georgia’s Growth Expectations

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the third and fourth quarters of 2019. Here are the highlights of this month’s release:

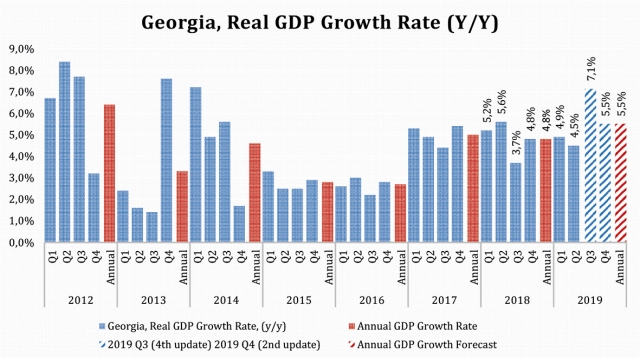

HIGHLIGHTS

• Recently, Geostat has released the preliminary estimate of real GDP growth for the second quarter of 2019, which now stands at 4.5%. This is only 0.3 percentage points below ISET-PI’s recent forecast.

• ISET-PI’s forecast of real GDP growth for the third quarter of 2019 stands at 7.1%—0.4 percentage points lower than last month’s prediction. The first estimate for the fourth quarter growth forecast stands at 5.5%.

• Based on July’s data, we expect annual growth in 2019 to be 5.5%. Although the annual growth forecast equals the estimate of the previous report’s worst-case scenario, we still expect a downward correction of the annual GDP growth numbers towards the end of the year, since we have not fully taken into consideration impeded tourist inflows, deteriorated foreign direct investments and increased risk of negative external shocks. In addition, the National Bank of Georgia revised its expectation for real GDP growth down from 5% to 4.5% in 2019. According to the Monetary Policy Report, among the reasons behind the prediction’s downward revision is the rise of external sector risks.

The Georgian statistics office, Geostat, has released its preliminary estimate of GDP growth for the second quarter of 2019. Its estimated growth figure is 4.5%, which is 0.3 percentage points lower than ISET PI’s forecast. As a result, our projected real GDP growth for the third quarter of 2019 has been revised downward to 7.1%. According to Geostat, electricity, gas and water supply (11.5% yearly), hotels and restaurants (14.1% yearly), transport (17.9% yearly), communication (10.8% yearly) and real estate, renting and business activities (16.9% yearly) were the sectors with the largest contribution to the annual real GDP growth in the second quarter of 2019. While the mining and quarrying (-7.7% yearly), manufacturing (-4.5% yearly), construction (-4.6% yearly) and education (-7.9% yearly) sectors had a negative contribution to the Q2 growth figure.

In addition, a number of variables demonstrated significant monthly and yearly changes in July. In particular, improved external statistics, depreciated real effective exchange rate, increased inflation, and increased volume of domestic and foreign currency deposits had a significant impact on the growth predictions.

IMPROVED EXTERNAL STATISTICS

The second quarter of 2019 shows strong growth in the wider region. According to the estimates for Q2 2019, most of the countries in the region showed improvement compared to the same period in the previous year. The Armenian economy reached remarkable 6.6% annual growth. Furthermore, the economies of Russia and Kazakhstan advanced by 1.4% and 3.4% respectively. Meanwhile, Azerbaijan experienced 2.4% annual growth in the first half of 2019. Thus, improved economic conditions in the wider neighborhood stimulated the Georgian economy through the trade, remittances, and tourism channels. However, the effect of reduced tourism flows due to Russia’s prohibition of flights to Georgia still has not been reflected in the model’s database.

Notably, exports grew by 17.5% year-over-year in July of 2019, driven by significantly larger exports/re-exports of copper ores and concentrates to Romania and Spain, increased exports/re-exports of motor cars, alcoholic beverages and medicaments to Ukraine, and accelerated export of ferro alloys, mineral water, and centrifuges to Russia. However, exports of copper ores and concentrates to China declined notably. During the same period, imports declined by 4.4%, driven by reduced import of petroleum and petroleum oils, motor cars, medicaments, and cigars, cheroots, cigarillos and cigarettes. It is notable that the world prices of crude oil decreased by 13.9% yearly, which explains in part the reduced import of petroleum products. As a result, the trade deficit shrank by 16.1% compared to the same month in 2018, and reached 435.3 million USD.

Both remittances and tourism showed significant yearly increases in July of 2019. Money transfers rose by 7% in the seventh month of 2019, driven by remittances from Kyrgyzstan (+98% or 0.7pp), Poland (+64.9%), Ukraine (+46.5%), Italy (+26.5%), Greece (+13.3%). Remittances from the Russian Federation and Turkey experienced a slight yearly decline and had negative contributions of 2.8 and 1 percentage points respectively to the total growth of remittances. Nevertheless, Russia remains the top country of origin for money inflows, accounting for 25% of total remittances. The share of money inflow from the European Union amounted to 35% of the total.

The number of international visitors increased by only 4.3% in July, compared to the same month of the previous year, while the number of tourists increased by 1% annually and reached 65% of total international visitors. The negative shock of the prohibition of flights from Russia has already started to be reflected in the data, but the impact will be even stronger in the following reports of the GDP forecast. Overall, trade, tourism, and remittances had a significant positive contribution to the GDP growth forecast.

Nevertheless, foreign direct investment (FDI) in Georgia amounted to 187 million USD in the second quarter of 2019, which is 53.7% lower than the adjusted data from Q2 2018. According to Geostat, the main reasons for decreasing FDI included completion of a pipeline project, reduction in liabilities to non-resident direct investors, and reduction of the amount of reinvestment. In addition, FDI experienced notable reductions in the energy (37.6% yearly), construction (91% yearly), transport (58.6% yearly), communication (162.3% yearly), real estate (63.7% yearly) and financial (-153.8% yearly) sectors, while FDI increased notably in agriculture (231.7% yearly [but still remains a very small part of overall FDI]) and manufacturing (97.3%). The recent trends in FDI are not taken into consideration in our model yet.

EXCHANGE RATE EFFECT AND INFLATION

The real effective exchange rate (REER) depreciated by 4.1% monthly in July, and by 11.7% relative to the same month of the previous year. While the nominal effective exchange rate (NEER) depreciated by 4% monthly and 11.7% yearly. The depreciation of the REER and NEER is typically associated with reduced value of domestic exports in the very short-run period and gaining competitiveness of export production in foreign markets later.

Notably, the lari real exchange rate depreciated with respect to the national currencies of the major trading partners. The GEL/TRY and GEL/RUB real exchange rates depreciated compared to the same month of the previous year by 8.7% (depreciated by 6.7% monthly) and 14.3% (depreciated by 4.9% monthly) respectively. In addition, the lari real exchange rate experienced a notable depreciation against the US dollar and the euro (falling on average by 3.4% and 2.3% respectively in monthly terms). Overall, REER-related variables had a small negative contribution to the Q2 real GDP growth projections.

In July, the annual inflation rate reached 4.6%, which is 1.6 percentage points higher than the targeted 3%. The main contributor to the annual price increase was the increased excise tax on tobacco (making the excise tax equal on filtered and unfiltered cigarettes) and increased food prices, which contributed to annual inflation by 0.9 and 2.2 percentage points respectively (it is worth noting that increased bread prices contributed 0.5 percentage points to annual inflation). However, one should note that this type of tax hike (excise on tobacco) can increase only the level of prices, not the inflation rate going forward (it is a one-time factor) and this effect is expected to be exhausted next year. Core inflation (inflation excluding the most volatile petroleum and food prices) remains at a low level of 1.9%, while the annual inflation of imported goods reached 4.8%.

The recent lari depreciation with respect to the currencies of the major trading partners most probably will lead to increased prices of imported products, which would further exacerbate the upward pressure on prices and inflationary expectations emerge. Hence, the National Bank of Georgia increased the Monetary Policy Rate (MPR) by 0.5 percentage points in September, reaching a level of 7%, which restricts borrowing and is expected to have a negative impact on the future growth rate. According to the model, the inflation rate has a negative contribution to the growth forecast.

INCREASED VOLUME OF DOMESTIC AND FOREIGN DEPOSITS

The other group of variables that experienced remarkable monthly and yearly changes and made a significant positive contribution to the Q3 and Q4 forecasts was the volume of domestic and foreign currency deposits in commercial banks. In particular, the total volume of domestic currency deposits increased by 10.2% annually, while the total volume of foreign currency deposits went up by 24.7% compared to the same month of the previous year. The growth of foreign currency deposits is mainly driven by the sharp depreciation of the national currency. Nevertheless, growth rates are still pronounced even after excluding the exchange rate effect. In the case of domestic currency deposits, growth is mainly driven by demand deposits and long-term time deposits. While in the case of foreign deposits, nearly all of the categories experienced notable annual growth. Deposit dollarization increased by 1.1 percentage points monthly and 0.7 percentage points yearly. The deposit-related variables had a positive contribution to the real GDP growth.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (the 1st vintage) is available about five months before the end of the quarter in question. The last forecast (the 5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych