Improved Trade Balance & Resilient External Sector Keep Georgia’s Annual Growth Projections in Line with Last Year’s Performance

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the fourth quarters of 2019. Here are the highlights of this month’s release:

HIGHLIGHTS

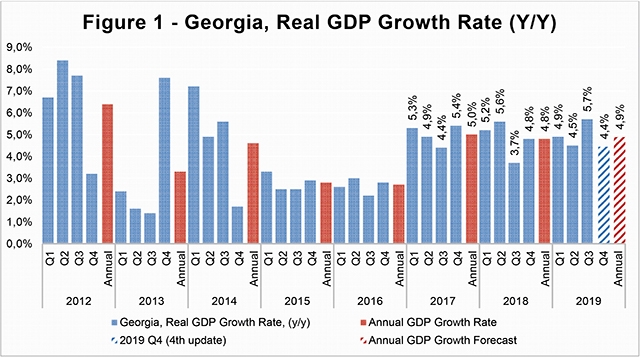

• Recently, GeoStat has released its preliminary estimate of real GDP growth for the third quarter of 2019. The Q3 growth rate now stands at 5.7%, which is 1.4% below the ISET-PI’s last forecasted value. As a result, the estimated real GDP growth for the first nine months of 2019 amounted to 5.0%.

• ISET-PI revised its forecast of real GDP growth for the fourth quarter of 2019 to 4.4% - down from 5.5% in September.

• Based on September’s data, we expect annual growth in 2019 to be 4.9%. This number is in line with the National Bank of Georgia’s growth forecast for 2019 (the forecast remained unchanged at 4.5%). According to the latest Monetary Policy Report, there are two groups of factors which pull growth in opposite directions: (1) the tightened monetary policy (to prevent emergence of the inflationary expectations) negatively affecting the growth forecast, and (2) improved trade balance and strong fiscal stimulus positively contributing to the growth estimation.

According to GeoStat’s recent release, the official estimate for the third quarter of 2019 (based on VAT taxpayers’ turnover data) now stands at 5.7%. The newly estimated Q3 figure was lower than initially anticipated by our forecast. Consequently, the ISET-PI Q4 forecast has also been revised downward to 4.4%. Thus, the revision of the forecast has to do with the update of the Q3 growth estimate rather than significant changes in the model’s core explanatory variables. Yet, a few variables in the model did change substantially, both in annual and in monthly terms. In particular, increased national and foreign currency deposits, improved trade balance (positive influence), depreciated nominal and real effective exchange rate and high inflation (negative influence), which notably exceeded the targeted inflation, had a significant impact on the growth predictions.

National and Foreign Currency Deposits

The first set of variables that have had a significant positive effect on our forecast relate to the national and foreign currency deposits in commercial banks. Almost all types of deposits increased significantly both in yearly and monthly terms. In particular, the total volume of domestic currency deposits increased by 12.2% annually, while the total volume of foreign currency deposits went up by 18.2% compared to the same month of the previous year. The growth of foreign currency deposits is mainly driven by the sharp depreciation of the national currency. Nevertheless, growth rates are still pronounced even after excluding the exchange rate effect.

Trade Balance

External sector had a positive effect on the GDP forecast. In September, Georgia’s export of a merchandize goods increased only moderately by 0.5% relative to the same month of the previous year. This was largely driven by an increased export/re-export of copper ores and concentrates to Romania, significantly larger export of mineral fertilizers to Republic of Lithuania, increased re-exports of motor cars and trucks to Ukraine and Armenia. However, Georgian exports of ferro alleys to Russia and export/re-export of motor cars and cigarettes to Azerbaijan experienced a notable drop in September. During the same period, import experienced slightly higher 4% growth year-over-year. However, the trade balance (net-export) improved by 0.5% (trade deficit was reduced to 446.3 million US Dollar).

In addition, remittances and tourism inflows continue growth in September. Money inflow increased by 13.9% compared to the same month of the previous year (mainly driven by increased remittances from Kazakhstan (101% yoy), EU (21.7% yoy) including Italy (27.2% yoy), Greece (12.3% yoy)and Germany (29.2% yoy), and small increase of the money inflow from USA, Israel and Turkey), while the number of tourists (visitors staying in Georgia for more than 24 hours) increased only by 0.6% yearly (growth rates decreased notably after banning flights from Russia), while the number of international visitors raised by 2.7% year-on-year. Overall, an improved trade balance, increased money inflows, and a dramatic rise in the number of visitors and tourists in September had a significant positive impact on our growth forecast.

Nominal and Real Effective Exchange Rate

Georgian lari depreciated against nearly all of the trading partner currencies in September. The most significant depreciation was observable with respect to the Russian ruble (3.4% in month and 15.5% in annual terms) and Turkish lira (3.2% in month and 19.8% in yearly terms). The GEL/USD exchange rate depreciated by 0.3% and 13.0% monthly and yearly respectively, while the GEL/EURO exchange rate depreciated by 6.5% yearly and appreciated by 0.7% monthly.

The depreciation of the Real Effective Exchange Rate (REER) had a negative contribution to the Q4 real GDP growth projections. REER depreciated by 0.4% monthly and 11.2% yearly in September (see the graph below). The lari real exchange rate (RER) depreciated yearly with respect to the national currencies of the United States (7.9%), Russia (13.5%), the EU (1.8%), and Turkey (22.7%). Theoretically, the negative impact of REER depreciation should not be surprising, given that the overall impact of REER on real GDP growth is ambiguous (on the one hand, cheaper national currency contributes to higher prices for imported goods, but on the other hand real depreciation increases competitiveness of Georgian exports in the longer run). Nevertheless, the negative impact of lari depreciation in September was likely small and counterbalanced by significant growth in the external sector variables.

High Inflation

The recent depreciation of the lari against the currencies of major trading partners has already led to increased prices of imported products, which further exacerbated the upward pressure on prices. The annual inflation of the consumer price index (CPI) amounted to 6.4% in September (notably higher than the targeted 3%), while the main contributors were increased prices on tobacco and alcohol (driven by increased excise tax on tobacco and accounted for 0.9 ppts of annual inflation) and raised food prices (driven by exchange rate depreciation and increased food prices in the world market , and accounted for 3.3 ppts of annual inflation). The core inflation also reached to 3.2% in September. Hence, the National Bank of Georgia increased the Monetary Policy Rate (MPR) twice in September by 0.5 percentage points each, and once in October by 1 percentage point, reaching a level of 8.5%, which restricts borrowing and is expected to have a negative impact on the future growth rate.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (the 1st vintage) is available about five months before the end of the quarter in question. The last forecast (the 5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych