Georgia Achieves “Best Case Scenario” Growth Rate of 5.2% Predicted One Year Ago

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the fourth quarter of 2019 (the final update) and the first quarter of 2020. Here are the highlights of this month’s release:

HIGHLIGHTS

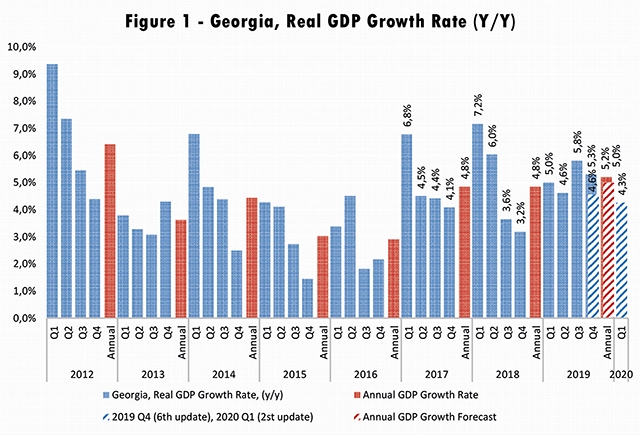

• Geostat has published its rapid estimate of real GDP growth for the fourth quarter of 2019, and their estimated growth stands at 5.3%, which is 0.7 percentage points above ISET-PI’s most recent forecast.

• The real GDP growth rate reached 3.8% year-on-year for December 2019.

• Utilizing the latest data, annual real GDP growth in 2019 amounted to 5.2% (the first rapid estimate). By February of 2019 (the very first forecast), our model predicted 4.4% and 5.2% real growth in the “middle-of-the-road” and “best-case” scenarios respectively . Moreover, our annual GDP forecasts of 4.9% (since November) and 5% (in January, very last forecast), were revealed to be quite accurate.

• According to the most recent (second vintage) forecast for 2020, the growth rate in the first quarter is predicted to be 4.3%.

The Georgian statistics office, Geostat, has released its preliminary estimate of GDP growth for the fourth quarter of 2019. Its estimated growth figure is 5.3%, which is 0.7 percentage points higher than ISET-PI’s forecast. As a result, the first rapid estimate of the annual real GDP growth for 2019 amounted to 5.2%. It is worth noting that Geostat updated its methodology for estimating real GDP, which has resulted in an upward revision of quarterly growth rates for 2019. This explains our recent annual forecast’s (fairly small) deviation from the actual growth rates. Moreover, the second update of the growth rate in the first quarter of 2020 is predicted to be 4.3%, which is 0.1 percentage points higher than the previous update.

In addition, a number of variables demonstrated significant monthly and yearly changes in November. In particular, increased volume of domestic and foreign currency deposits, improved external statistics, slightly depreciated real effective exchange rate and excessive inflation had a significant impact on the growth predictions.

DOMESTIC AND FOREIGN CURRENCY DEPOSITS

The first set of variables that have had a significant positive effect on our forecast relate to national currency deposits in commercial banks. In November, all types of national currency deposits (except time deposits with a maturity of less than 3 months, which grew by 6.8% annually)—from the most liquid (currency in circulation (up by 40.1% yearly)) to the least liquid (time deposits with a maturity of more than 12 months (up by 73% yearly)) — experienced double-digit growth in annual terms. As a result, total national currency deposits increased by 20.4% year-over-year.

Significant annual increases were observed in the amounts of foreign currency deposits, which experienced 18.1% growth in annual terms. These pronounced growth figures can be partially explained by the notable yearly depreciation of the lari against the currencies of major trading partners, but the growth rate remains positive even after excluding the exchange rate effect. Furthermore, total deposits (including national and foreign currency deposits) increased by 19.5% year-over-year. As a result, deposit dollarization, which had been on a declining trajectory for the first half of 2019, started gaining new momentum in the second half of the year reaching 64% in November (increased by 0.04 ppts monthly, but grew by 2.1 ppts compared to April 2019 (mainly due to exchange rate effect), the month with the lowest dollarization measure in all of 2019).

EXTERNAL STATISTICS

The first month of the fourth quarter of 2019 shows strong growth in the wider region. According to the estimates for October, most countries in the region showed improvement compared to the same period in the previous year. The Armenian economy reached remarkable 7.7% annual growth. Furthermore, the economies of Russia and Kazakhstan advanced by 3.1% and 5.4% respectively. Meanwhile, Azerbaijan experienced 2.1% annual growth in the tenth month of 2019. Thus, improved economic conditions in the wider neighborhood stimulated the Georgian economy through the channels of trade, remittances, and tourism. However, the effect of reduced tourism flows due to Russia’s prohibition of flights to Georgia has still not been reflected in the model’s database.

As a result, Georgia’s external statistics continue to improve. Exports grew by 25.2% year-over-year in November of 2019 and were driven by significantly larger exports/re-exports of copper ores and concentrates to China and Belarus, together with increased exports of wine and mineral water to Russia, motor cars and trucks to Armenia and Ukraine, and cigarettes and cigars and motor cars to Azerbaijan. During the same period, imports increased by 4.2%. The trade deficit thus shrunk by 8% compared to the same month in 2018 and amounted to 436.8 million US dollars.

In addition, both remittances and tourism showed significant yearly increases in November. Money transfers increased by 13.3%. These were driven by a rise in remittances from Kazakhstan (134.5%), Kyrgyzstan (167.2% with 2.1 ppts contribution in total growth), Italy (18.8%), Greece (8.3%), Germany (27.1%), and Turkey. However, remittances from Russia declined notably (1.3 ppts negative contribution to the total growth of money inflow).

The number of international visitors to Georgia increased by 11.9% in November compared to the same month the previous year, while the number of tourists increased by 10.3% annually and accounted for 62% of all international visitors. According to the model, both tourism and remittances made a significant positive contribution to the GDP growth forecast.

DEPRECIATED REAL EFFECTIVE EXCHANGE RATE

In November, the Real Effective Exchange Rate (REER) remained the same relative to October 2019, and depreciated by 6% relative to the same month the previous year. Depreciation of the REER is typically associated with domestic export goods gaining competitiveness on foreign markets, but it also translates into increased prices on imported goods. Notably, the lari real exchange rate depreciated with respect to the national currencies of two major trading partners—Turkey and Russia—and appreciated with respect to the euro and dollar in monthly terms. While the lari depreciated with respect to the currencies of all major partners in annual terms. Overall, REER-related variables had a small negative contribution to the real GDP growth projections.

HIGH INFLATION

At the same time, the cost of living, as measured by the Consumer Price Index (CPI) and the Khachapuri Index, increased notably in November compared to the same month of the previous year. Despite the fact that the National Bank of Georgia has already employed all of its instruments to control inflation (conducted contractionary monetary policy), annual inflation remained at a high level: 7% in November (while the inflation target is 3%). About 0.9 ppts of CPI inflation were due to higher tobacco prices, while food prices contributed 3.8 ppts with 14.1% annual growth. The measure of core inflation amounted to a relatively moderate 3.5%. Our forecasting model identifies the high inflation rate as a main negative contributor to future GDP growth.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (the 1st vintage) is available about five months before the end of the quarter in question. The last forecast (the 5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych