Electricity Market Watch

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of key sectors of Georgian economy. As part of our energy sector coverage, we produce a monthly Electricity Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

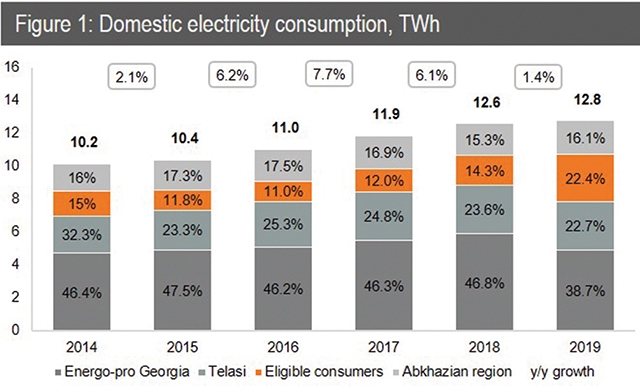

Electricity consumption and generation – summary of 2019

Domestic consumption of electricity increased by 1.4% y/y and reached 12.8TWh in 2019. The growth is far below expected, as well as last years’ similar figures. The slowdown in growth is mainly explained by climate conditions. Additionally, a 7.8% decrease in Georgian Manganese electricity consumption reduced overall consumption growth by 0.7 percentage points.

Electricity consumption dynamics of certain consumer groups are explained by legislative changes. Consumption by eligible consumers (also known as direct consumers) increased by 59.6% y/y, while distribution licensees’ consumption was down 11.6% y/y in 2019. From the group of distribution licensees, Energo-pro Georgia’s consumption reduced the most (-16.3% y/y), as several of its subscribers were registered as direct consumers. In line with the market deregulation started in 2018, all companies with an average monthly consumption over 5GWh were mandatorily registered as direct consumers. As a result, the number of direct consumers increased from two to a total 15 companies. Moreover, their share in overall domestic consumption increased from 12.0% in 2017, to 22.4% in 2019.

Despite the slowdown in consumption growth, electricity imports and thermal generation increased by 7.8% y/y and 34.3% y/y, respectively. This growth is associated with a 10.1% y/y decrease in hydro generation, attributable to bad hydrological conditions. In 2019, the share of hydro generation in the total supply was at a 10-year low of 66.3%.

Import of electricity increased by 7.8% y/y and reached 1.6TWh in 2019. Notably, for the first time this year, electricity was imported in July along with August – the months generally considered most suitable for export. A 68% of electricity was imported from Azerbaijan and the rest came from Russia (32% of total). The main import source during the January-August period was Azerbaijan, with 91.1% of total imports. From September to November, Azeri import was replaced by Russian, with a 75% share in total. This switch is explained by the cheaper electricity import price from Russia – the average import price in August, when electricity was fully imported from Azerbaijan, was USc 5.2/kWh, while the average import price in October, when 99% of electricity was imported from Russia, was USc 4.7/kWh (-8.8% difference).

Trade deficit widened by 24.2% y/y and reached a record high of US$ 70.5mn in 2019. The cost of import increased by 3.4% y/y and reached $78.3mn (on average USc 4.8/kWh), from which c. US$22mn was spent on imports from Russia. On the other side, revenue from electricity exports was at a 10-year low of $7.8mn. A 58.8% annual decrease of electricity exports to a mere 0.2TWh is explained by a deficit on the local market and the comparatively low profitability of export markets.

For the first time in 2019, electricity was included in the list of top 10 imported products. Its share in the country's total imports was 0.86% in 2019 and has been in this range (0.8%-0.9%) since 2017.

Tariff Modifications – Enguri, Vardnili and GSE

GNERC made significant tariff modifications for TPPs, Enguri, Vardnili and Georgian State Electrosystem. Moreover, the GNERC had approved the natural gas tariff for residential users by the end of 2019.

Tariffs for Enguri and Vardnili were reduced due to the postponing of planned renovations of 2019 to 2021-22. The Enguri tariff decreased by 25.3% from 1.818 Tetri/kWh to 1.358 Tetri/kWh, and Vardnili’s tariff almost halved from 4.002 Tetri/kWh to 2.206 Tetri/kWh. According to the GNERC methodology, the tariff for the regulated companies operating in the electricity sector is set for a three-year period, and their intermediate revision happens only if reality significantly deviates from the initial investment plan. The reason behind the 2020 tariff reduction was the postponed rehabilitation works on the Enguri tunnel and Vardnili’s electro-mechanical equipment, originally planned for 2019 and postponed until 2021 or 2022.

The decline in the Enguri tariff will also affect the prices on the balancing market. The Enguri HPP has the smallest regulated tariff on the market, which, according to current market rules, is used as a reference price for balancing electricity purchased by ESCO from deregulated small HPPs during the May-August period. Respectively, power plants not having a direct purchaser will receive 1.358 Tetri/kWh from ESCO (instead of 1.818 Tetri/kWh) during the May-August period of 2020. Notably, the September-April reference price was also changed recently but in the opposite direction, being increased by 15.9% y/y to 12.304 Tetri/kWh.

The transmission fee of the Georgian State Electrosystem was reduced by 23.4% y/y. The tariff for 2020 is set at 1.013 Tetri per kWh, down from 1.323 Tetri/kWh in 2018-19. Direct consumers, exporters and distribution companies will pay this tariff, along with other service charges. The reduction of this tariff will affect the total service charges and decrease it by 12.9%.

Tariff Modifications – thermal power plants

Tariffs for thermal power plants were set for 2020-22. Thermal power plants have two sources of income – tariff for generated electricity and guaranteed capacity fee:

1) The methodology for generated electricity tariff calculation changed from fixed annual tariffs to fluctuate monthly ones, but the principle of covering only variable costs remained the same. Notably, the gas purchase tariff was set by GNERC at $143 per 1,000 m3, as it was in the previous tariff period. Thus, radical changes in these tariffs are not expected, only a slight increase might be observed in light of the currency fluctuations.

2) With a guaranteed capacity fee, the investor pays back the investment costs and gets a predefined profit margin. On the other hand, it is a source of reserve for the system. Guaranteed capacity fee is received by TPPs for its readiness to produce electricity upon a dispatcher's command. Guaranteed capacity charges increased for all five power plants by 25.8% y/y for 3rd and 4th blocks, by 5.3% y/y for Gardabani and insignificantly for Mtkvari Energy and G-Power. According to preliminary data, in 2020, the thermal power plants will receive a total of GEL 170.5mn as guaranteed capacity. This amount is paid by consumers and exporters in proportion to the electricity consumed.

Importantly, the new Gardabani-2 Thermal Power Plant will operate under a different tariff regime and will not be a guaranteed capacity supplier. Its source of income is a 14-year guaranteed power purchase agreement at USc 5.5/kWh for 1,200kWh annual generation.

By Georgia Today by Mariam Chakhvashvili