Excess Inflation Drags Down 2020 GDP Forecast

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the first and second quarters of 2020. Here are the highlights of this month’s release:

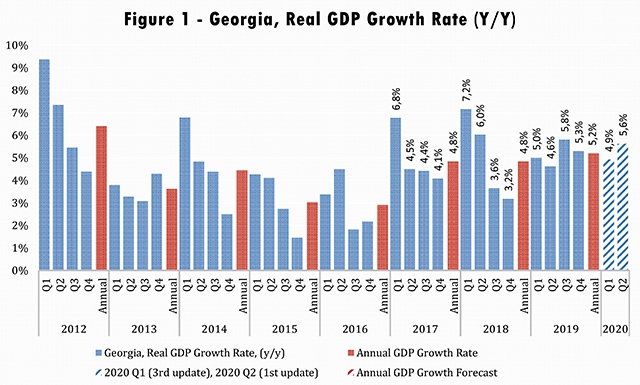

HIGHLIGHTS

• GeoStat has published its rapid estimate of real GDP growth for the fourth quarter of 2019. Their estimated growth stands at 5.3%, which is 0.7 percentage points above ISET-PI’s most recent forecast. The annual real GDP growth for 2019 amounted to 5.2%.

• The real GDP growth rate reached 5.1% year-on-year for January 2020.

• ISET-PI’s forecast for the first quarter of 2020 now stands at 4.9%—up from 4.3% in January. The second quarter growth forecast currently stands at 5.6%.

• Based on the data from December, we expect annual growth in 2020 to be 5.0% in the worst-case scenario, and 6.1% in the best-case or the average long-term growth scenario. Our middle-of-the-road scenario (based on average growth in the last four quarters) predicts a 5.4% increase in real GDP.

According to ISET-PI’s recent forecast, GDP growth for the first quarter of 2020 increased from 4.3% to 4.9%. This correction can be explained by the fact that it is the first time our model has taken into consideration the rapid estimate of Q4 GDP growth. As already mentioned in our previous publication, estimated real GDP growth in the fourth quarter of 2020 amounted to 5.3%, which is 0.7 percentage points above our predicted 4.6%.

Otherwise, looking at the economic landscape from the standpoint of the December data, several variables changed significantly and affected growth predictions in different ways. Improved external statistics and an increased number of deposits are the main contributors to the GDP growth, while the annually depreciated (monthly appreciated) Real Effective Exchange Rate (REER) and excessive inflation had negative effects on growth predictions .

IMPROVED EXTERNAL STATISTICS

The first variable which has had a significant positive effect on the predicted real GDP growth is related to the external sector. Georgia’s exports continued to expand, increasing by 18.7% yearly in December 2019, while imports were up by 12.8%. The trade deficit, however, deepened by 8.9% yearly, and amounted to 536.7 million US dollars. Furthermore, double-digit growth in the export statistics was driven by increased re-export of motor cars to Armenia and Ukraine, together with raised export of copper scrap and wastes to Belarus, and medical devices and instruments to Poland. There was no change in exports to Russia and a slight decrease in exports to Azerbaijan (due to decreased export of cigarettes). The improvement in trade statistics was mainly due to better economic conditions in the entire region.

Furthermore, remittances increased by 14.2% yearly, raising people’s disposable income, consumption, and real GDP growth. The main contributors to this increase were Kyrgyzstan (215.9% yearly, contributing 2.2 percentage points to total growth), the European Union (16.4% yearly), including Italy (19.3% yearly), Greece (14.8% yearly) and Germany (27.4% yearly). Russia and EU countries accounted for 63% of total money inflows.

In addition, the number of international visitors increased by 16.3% yearly, while the increase in tourist numbers (visitors who spent 24 hours or more in Georgia) amounted to 15.5%. In summary, increased money inflow and the dramatically higher number of visitors and tourists in the corresponding month made a significant positive contribution to the growth forecast.

INCREASED NUMBER OF DEPOSITS

The other set of variables with a significant positive effect on our forecast relate to national and foreign currency deposits in commercial banks. In December, all national currency deposits (except short-term time deposits [less than 3 months]) experienced significant growth in annual terms. In particular, national currency demand deposits saw an annual increase of 6.6%. Additionally, national currency time deposits increased by 7.0% annually. The only variable that experienced a notable yearly decline was time deposits of less than 3 months (by 18.3% yearly). Consequently, national currency total deposits increased by 11.1% yearly.

Foreign currency total deposits increased by 15.8% compared to the same month of the previous year. Furthermore, foreign currency demand and time deposits increased by 13.0% and 14.6% yearly, respectively. Deposit dollarization increased to 64.1%, compared to 63.6% in the same period the previous year (and 63.9% the previous month). According to our model, these trends in national and foreign deposits have had a significant positive contribution to real GDP growth.

MONTHLY APPRECIATED REAL EFFECTIVE EXCHANGE RATE

In December, the Georgian lari appreciated monthly in real terms against all main trading partners’ currencies. The most significant appreciations were observable with respect to the Turkish lira (3.7% monthly) and US dollar (2.6% monthly). In addition, the Real Effective Exchange Rate (REER) appreciated by 1.9% relative to the previous month, but depreciated by 5.3% relative to the same month in the previous year (this pattern was shared with the Nominal Effective Exchange Rate). Notably, during December of 2019, NBG did not sell or purchase foreign exchange reserves and increased the Monetary Policy Rate by 0.5 percentage points to 9%. Overall, REER-related variables had a small negative contribution to real GDP growth projections.

EXCESS INFLATION

According to our model, the main negative contributor to growth was the increased consumer price level, compared to the same month of the previous year. In December, annual inflation of consumer prices amounted to 7%, which is notably higher than the targeted 3%. About 0.9 percentage points of CPI inflation were due to higher tobacco prices, driven by the one-time increase in excise tax, while food prices contributed 3.5 percentage points with 12.8% annual growth. The measure of core inflation amounted to a relatively moderate 3.7%. The National Bank’s contractionary monetary policy (increased Monetary Policy Rate, reduced reserve requirements in dollars, etc.) is expected to bring annual inflation to the target level by the second half of 2020. Our forecasting model identifies the high inflation rate as a main negative contributor to future GDP growth.