Georgia’s Growth Prospects before COVID-19, & How Things Might Change

ISET-PI has updated its Georgian real GDP growth rate forecast for the first and second quarters of 2020. Here are the highlights of this month’s release:

HIGHLIGHTS

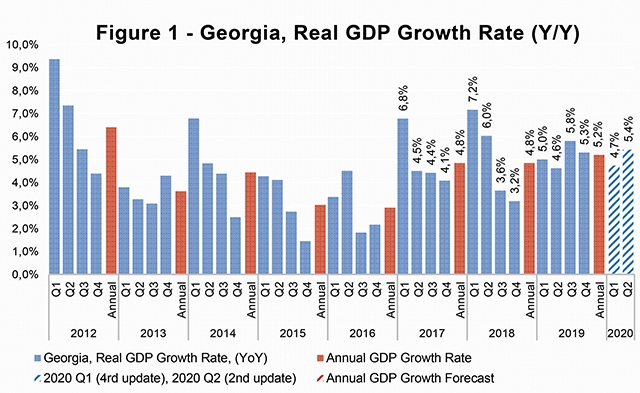

• The annual real GDP growth for 2019 amounted to 5.2%, while the real GDP growth rate reached 5.1% year-on-year for January 2020.

• Before taking into consideration the negative consequences of COVID-19 on the real GDP growth forecast, ISET-PI predicted 4.7% and 5.4% growth for the first and second quarters of 2020 respectively, based on data from January 2020.

• Consequently, the annual growth in 2020 was expected to be 4.8% in the worst-case scenario, and 5.9% in the best-case or an average long-term growth scenario. Our middle-of-the-road scenario (based on the average growth in the last four quarters) predicted a 5.2% increase in real GDP.

• After considering the negative impacts of COVID-19 on Georgia’s economy, via tourism, remittances, trade, and restricted domestic production and service provision due to the strict social-isolation measures, the real GDP growth is expected to decrease notably, depending on the length and severity of the pandemic.

• It is projected that the real GDP may decline by 0.82 percentage points if there is no international, outbound, or domestic tourism between March-May of 2020. While it could reach 1.87 and 5.37 percentage points if the restrictions last until July or December, respectively.

• Taking into consideration the correlation between the growth rates of Georgia and its partner countries, and Bloomberg’s real GDP growth scenarios of change for the world’s leading countries, Georgia’s real GDP growth in 2020 could vary from 0.82% to 3.91% (assuming a 5% baseline growth).

• Based on various scenarios of net decline in money transfers (from a 10% to a 50% decline), the share of household real consumption spending (considering the exchange rate and inflation) may change from +0.3% to -5.5%.

Read on for the possible effect of the COVID-19 pandemic on the Georgian economy.

Consumption and Investment

Decline in domestic consumption due to behavioral and policy changes – i.e. people staying home as a precaution or as a requirement. Moreover, currency depreciation and possible price spikes (due to herding behaviors and potential disruptions in supply chains) are expected to have a negative effect on consumption and investment. Household consumption accounts for 66.7% of the Georgian GDP (Geostat, 2018). A significant reduction in household consumption (e.g., spending on transportation, clothing, electronics, and domestic services) would therefore result in an overall slowdown of GDP growth. Decline in domestic investment – uncertainty and deteriorating business sentiments will stall business investment decisions. Expectations of a global recession could become self-fulfilling if ‘business-as-usual’ does not resume in the next few months. If companies expect a slowdown in demand, they will also delay investment, and GDP will decline further. Investment (gross fixed capital formation) accounts for approximately 28% of Georgia’s GDP.

Tourism

Decline in tourism and related businesses – tourism arrivals and receipts are expected to decline sharply as a result of the numerous travel bans, and due to precautionary behaviors. By February, international visitor trips had already declined by 0.6% annually, while the number of tourist stays (overnight) experienced a relatively moderate 4% yearly growth. In terms of international visitor trips, among the top 10 countries, the largest decline in trips was observed in Armenia (-18.2% YoY), Russia (-25.0% YoY), Iran (-8.7% YoY), and in India (-9.9%), and there was a decline of 59.5% yearly in China. According to our preliminary calculations, the Georgian economy lost between 3-9% of potential tourism revenue in February. Since tourism industries account for 11.3% of Georgia’s GDP (GNTA 2018), and this share has had an increasing trend over the last three years (2016-18), a direct hit to the industry will substantially impact GDP. The GDP losses associated with the following scenarios lave been calculated below:

Remittances

Decline in remittance inflows – since all countries will suffer economically in the aftermath of the health and oil price crises, we expect significant slowdown in remittance inflows from the rest of the world. The remittances decline will hit Georgia particularly hard as it is among the top receiver countries of foreign transfers. For instance, in 2019, money transfer inflows accounted for 9.8% of GDP. Various scenarios for just how much Georgia is set to lose in monetary inflows are presented in the table below:

Growth Spillovers

The spillover effect on other sectors – a drop in demand for goods and services in the region, in China, the EU, and in the US, will affect the overall economy via trade and production linkages. While it is difficult to predict how Georgia’s economy will react to a global shock of such magnitude, some preliminary estimations may already be determined. Georgia’s growth rate over the last 20 years correlates notably to several neighboring economies. One of the greatest correlations is, unsurprisingly, with Russian economic growth. In order to discover how a slowdown across the world’s top economies will affect Georgia, we have followed three economic scenarios relating to major world economies, as reported by Orlik et al. (March 6, 2020, Bloomberg.com). The numbers reflect growth rate changes relative to the baseline (no virus outbreak).

Production

Production disruptions – domestic production will suffer as a result of forced business closures and the inability of workers to get to work, as well as disruptions to trade and business as a result of border closures, travel bans, and other restrictions on the movement of goods, people, and capital. The overall impact on production may be mitigated by the fact that in some sectors (particularly in manufacturing) production can be ramped up in later periods to compensate for lower production (providing closures do not last too long).

Fiscal and Monetary Policy

Georgia’s public finances are in a tolerable enough shape to handle a crisis. Public debt to GDP ratio is not very high (44.9% in 2018), and the government budget deficit is also below 3% of the GDP. One of the most important tools in overcoming the crisis and achieving a fast recovery could lie in increased fiscal expansion. Georgia’s government has already announced its boosting capital expenditure (CapEx) projects, aimed at providing additional economic incentives.

While other countries push for fiscal stimulus and monetary expansion, Georgia is facing uncertainties in terms of inflationary expectations. As discussed, this limits NBG’s ability to stimulate the economy under the current circumstances. Annual inflation in January-February was 6.4%, significantly higher than the 3% target. Going forward, a sharp decline in aggregate demand would reduce the pressure on inflation, while a depreciating nominal effective exchange rate will exert upward pressure. Therefore, the possibility to reduce the monetary policy rate depends on which effect will dominate in the future. In the meantime, NBG is approaching IMF to increase access to funding under its Extended Fund Facility program. Alongside the additional funds from other international donors, this will positively affect the economy, strengthen the nominal effective exchange rate and, consequently, curb inflation.