February Data: Deteriorating Economy, Good Outlook for 2021 Recovery

ISET-PI has updated its Georgian real GDP growth rate forecast for the first and second quarters of 2020. Here are the highlights of this month’s release:

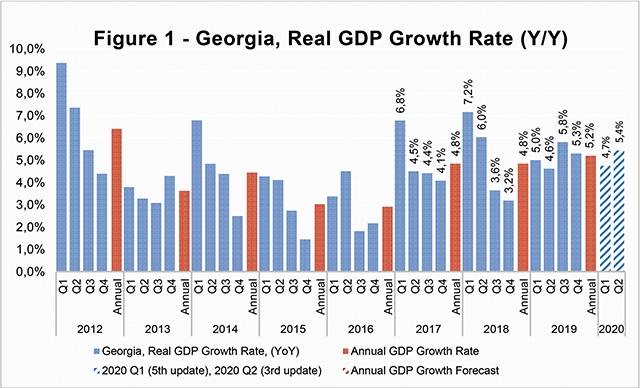

HIGHLIGHTS

• Geostat has released its rapid estimate of real GDP growth for February 2020. The estimated growth stands at 2.2%, while the average real GDP growth for January-February 2019 reached 3.7%.

• ISET-PI predicted 4.7% and 5.4% growth for the first and second quarters of 2020 respectively, based on February 2020 data. This data does not yet fully account for the negative impacts of COVID-19 pandemic on the national economy.

• Consequently, the annual growth in 2020 based on February data was expected to be 4.8% in the worst-case scenario, and 5.9% in the best-case or an average long-term growth scenario. Our middle-of-the-road scenario (based on the average growth in the last four quarters) predicted a 5.2% increase in real GDP.

• COVID-19 is expected to impact the Georgian economy via tourism, remittances, trade, lower domestic production and service provision due to the strict social-isolation measures. While we cannot estimate this impact precisely, we can consider several scenarios, according to which the real GDP growth is expected to decrease significantly, depending on the length and severity of the pandemic.

Growth Projections

Most of the international organizations lowered their forecasts of Georgia’s real GDP growth for 2020, while expecting a quick recovery in 2021. According to the Asian Development Bank’s (ADB) recent Asian Development Outlook, COVID-19 and monetary tightening will slow the growth rate to zero percent this year, picking up to 4.5% in 2021. Georgia’s real GDP growth forecast is the lowest among ADB countries (for detailed information see the figure 2). Furthermore, World Bank revised its forecast of Georgia’s real GDP growth downward. The new predictions vary from -0.2% (the worst case) to 2% (the best case) in 2020. The International Monetary Fund (IMF) has the most conservative prediction among the international organizations: -4% in 2020, while the same measure for 2021 is expected to reach 3%.

ISET-PI has recently released a Policy note detailing its own projections of the impact of COVID-19 under different scenarios. The global pandemic scenario estimates Georgia’s annual GDP growth to be at least 4.5 percentage points lower than the current forecast. This adjustment would put the country’s GDP growth in 2020 closer to 0.65% in the middle-of the-road scenario.

External Trade

In the face of the harsh measures that countries have taken to overcome the COVID-19 pandemic, trade of all commodities, except food and medicine, is projected to decline, depending on the duration of the shock. In February, exports decreased by 0.5% in yearly terms, however imports increased by 8.4% yearly. As a result, the trade deficit deepened by 14.8% year-on-year, and amounted to 440.1 million USD. Furthermore, deterioration of the external trade was even more pronounced in March. Georgian exports declined by 22.1% compared to the same month of the previous year, driven by reduced exports to Russia (-43.1% y-o-y; -7.2 ppts), Armenia (-45.1% y-o-y; -3.7 ppts), Ukraine (-35.6% y-o-y; 2.6 ppts), Romania (-88.4% y-o-y; -4.5 ppts), and USA (-89.3% y-o-y; -5.8 ppts). The largest decline was observed in the exports of capital goods (-76.4% y-o-y), fuel and lubricants (-41.4% y-o-y), and transport equipment (-37.7% y-o-y). Imports declined by 13.4%, driven by China (-38.4% y-o-y; -4.1 ppts), Turkey (-7.5% y-o-y; -1.2 ppts), Armenia (-39.2% y-o-y; -1.2 ppts), and Russia (-11% y-o-y; -1 ppts).

Remittances and Tourism

Since all countries will suffer economically in the aftermath of the pandemic and the oil price crisis, we expect significant slowdown in remittance inflows from the rest of the world. The remittances decline will hit Georgia, one of the world’s top receivers of foreign transfers, particularly hard. Money inflow showed a significant slowdown (grew by only 9.5%) already in February and even decreased by 9% in annual terms in March. The decline was driven by lower remittances from Russia (-28.3% y-o-y; -7.2 ppts), Italy (-8.7% y-o-y; -1.2 ppts), Israel (-10.2% y-o-y; -1 ppts), and Turkey (-0.1% y-o-y; 0 ppts).

Tourism arrivals and receipts are expected to decline sharply as a result of the numerous travel bans and due to precautionary behaviors. By March (after the ban on passenger flights), international visitor trips had already declined by 58.6% annually, while the number of tourist stays (overnight) experienced a 56.1% reduction in annual terms. In terms of international travel, the largest decline in trips was from Azerbaijan (-62.9% y-o-y; -11.9 ppts), Russia (-66.5% y-o-y; -10.6 ppts), Armenia (-61.1 y-o-y; -8.3 ppts), and Turkey (-%45.4% y-o-y; -5.5 ppts). Notably, the share of Tourism in Georgia’s GDP was 8.1% in 2019 (GNTA 2019).

Inflation and Exchange Rate

The deterioration in the external statistics created significant pressure on the exchange rate. In March, the Real Effective Exchange Rate (REER) depreciated by 2.6% relative to the previous month, and by 4.6% compared to the same month of the previous year. Moreover, Depreciation of the REER is typically associated with domestic export goods gaining competitiveness on foreign markets, but it also translates into increased prices on imported goods. Notably, the lari real exchange rate (RER) depreciated with respect to the national currencies of all the major trading partners except Russia: the GEL/USD real exchange rate depreciated by 5.4% monthly, the GEL/EUR real exchange rate by 7.3% monthly, and the GEL/TRY real exchange rate by 1.8% monthly, while the GEL/RUB real exchange rate appreciated by 8.3% in monthly terms. Annual inflation in March 2020 constituted 6.1%, which was higher than the 3% NBG target, while the annual inflation of food prices reached 13.4%.

Expectations

In the second quarter of 2020, ISET-PI’s Business Confidence Index (BCI) decreased by 53.0 index points reaching an all-time low of -27.2 points. Business confidence deteriorated significantly across all sectors. The largest decline was observed in retail trade, followed by the service industry. The decrease in BCI was driven by worsened past performance as well as drastically pessimistic future expectations.

The main factors that limited business activities for firms of all sizes remained lack of demand and limited access to finance. "Other" factors have also become a significant hindrance. These “other” factors would capture all negative economic effect resulting from the state of emergency declared in the country due to COVID-19. While the Georgian government has already presented the plan for gradually lifting the restrictions, the implementation of this plan will depend on the epidemic situation in the country.

Consumer Confidence Index (CCI) has also declined significantly by 13.6 index points compared to February 2020 (from -19.5 in February to -33.1 in March). This is the weakest and lowest figure since March 2017. The analysis shows deterioration in consumer’s present situation assessment as well as their expectations about the future.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We have constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (the 1st vintage) is available about five months before the end of the quarter in question. The last forecast (the 5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych