Electricity Market Watch

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of key sectors of Georgian economy. As part of our energy sector coverage, we produce a monthly Electricity Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

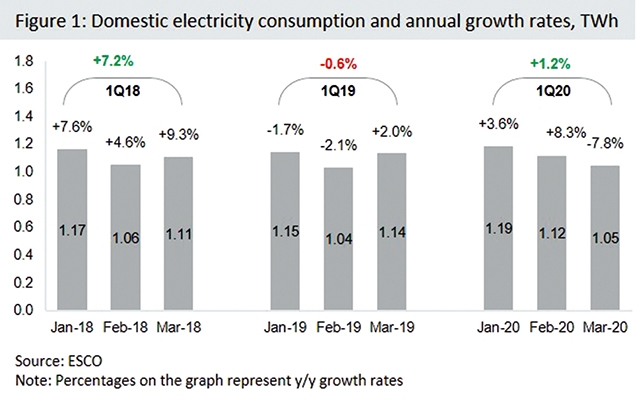

Electricity consumption and generation – First quarter of 2020

The Ministry of Economy expects the decrease in electricity consumption caused by Covid-19 to continue until Sep-20. Electricity consumption was down by 7.8% y/y in Mar-20 due to partial lockdown caused by the Covid-19 pandemic. The impact on electricity consumption will be sharper in April 2020, when full lockdown was in place. However, based on the updated annual forecast of the Ministry of Economy and Sustainable Development (adopted on April 24, 2020), the annual decrease in consumption in April is expected at 5.9%, less than actual growth figure for March. The same document forecasts negative growth of electricity consumption to continue until Sep-20, resulting in a 0.8% drop in annual electricity consumption in 2020 (to 12.7TWh).

Domestic consumption of electricity increased by 1.2% y/y and reached 3.4TWh in 1Q20. The growth is far below the expected 5% y/y growth, but higher than the 0.6% y/y decrease of 1Q19. Electricity consumption was up 3.6% y/y and 8.3% y/y in January and February, respectively. The growth was mainly attributable to eligible consumers.

Electricity consumption was down by 7.8% y/y in March 2020, caused by the partial lockdown due to Covid-19. From the 2nd half of March, the lockdown affected cafes, restaurants, hotels, shopping malls, and places for public gathering. Importantly, electricity consumption of eligible consumers was unaffected by the Covid-19 lockdown as large industrial users continued their everyday operations.

Electricity consumption dynamics of certain consumer groups in 1Q20 are explained by legislative changes. Consumption by eligible consumers (also known as direct consumers) increased by 52.8% y/y, while the distribution of licensees’ consumption was down 11.2% y/y in 1Q20. From the group of distribution licensees, Energo-Pro Georgia’s consumption reduced the most (-17.2% y/y), as several of its subscribers were registered as direct consumers. In line with market deregulation, started in May 2018, all companies with average monthly consumption over 5GWh were mandatorily registered as direct consumers. As a result, the number of direct consumers increased from 2 to a total 15 companies. Moreover, their share in overall domestic consumption increased from 9.8% in 1Q18 to 19.4% in 1Q20.

78.7% of the demand on electricity was satisfied by local generation in 1Q20, the rest was imported from Russia and Azerbaijan. Thermal generation was down by 11.7% in 1Q20 from a very high base in 1Q19 (+42.1% y/y). Wind generation (+9.2% y/y) accounted for a mere 0.7% of the total supply.

Generation from hydro power plants was down by 1.9% y/y and satisfied 46.4% of total demand in 1Q20. This decrease is attributable to unfavourable hydrological conditions, mostly affecting generation of January and February, down by 21.7% y/y and 12.9% y/y, respectively. After the start of the rainy season and snow melt, hydrogeneration was up by 30% y/y in Mar-20, but the growth was not enough to compensate the decline of 2M20.

Increased consumption in the Abkhazia region (+8.0% y/y) fully absorbed the generation of Enguri and Vardnili (-10.9% y/y) in 1Q20 and created a need for electricity imports from Russia through the Salkhino interconnection line.

Import of electricity increased by 39.6% y/y and accounted for 21.3% of total supply in 1Q20.

54.1% of electricity was imported from Azerbaijan and the rest came from Russia (45.9% of total). The most significant increase of imports took place in Feb-20 (+119% y/y), compared to 17.9% y/y and 4.3% y/y growth figures in Jan-20 and Mar-20, respectively. Notably, electricity imports for the Abkhazia region via the Salkhino line accounted c. 1/3 of total electricity imports and c.70% of imports from Russia.

The cost of electricity imports was up by 25.7% y/y and reached US$ 29.0mn in 1Q20.

The difference between the growth rates of imports volume and value is explained by comparatively low cost of electricity imports via the Salkhino line for the Abkhazia region. The same reason caused a reduction in the average import price from USc 4.3/kWh to USc 3.9/kWh (-10.0% y/y).

Balancing electricity price in Georgia was USc 5.4/kWh (+5.8% y/y) in 1Q20. A 25.9% of total electricity supplied to the grid was traded through the market operator (ESCO), with the rest traded through bilateral contracts. The balancing electricity price mostly derived from import price and guaranteed power purchase agreements (PPA) tariffs, accounting for 61.0% and 36.4% of total balancing electricity, respectively.

Turkish electricity prices averaged USc 4.8/kWh in 1Q20 (+0.8% y/y), 11% below the Georgian balancing electricity price.

Market reforms are moving forward

Policymakers are meeting their deadlines set by newly adopted energy law for market reforms. Government of Georgia has adopted concept design of electricity market; Georgian Energy and Water Regulatory Commission adopted licensing rules for Transmission System Operators and made changes into some legislative acts, including grid code.

According to the concept design of the electricity market:

Power trading on day-ahead, intraday, bilateral and balancing markets should start by Jul-21. Before then, the trading will continue in form of bilateral agreements, as it is today. Power Exchange Company, established in Dec-19 as joint venture of ESCO and GSE, is working with Nord Pool Consulting on creation of trading platforms and supporting operational rules. They promise to launch the platforms first in July 2020, and after a year of testing, full-scale operations will begin.

A public service provider at the wholesale level (probably ESCO) will be in charge of price stability on the market and supply of electricity to the Abkhazia region. The public service provider is allowed to trade on power markets if needed, but the main mechanism they will use for price stability is a contract for differences, when they compensate the difference between regulated or promised price and market clearing price. This company will be the price stability guarantor for:

• Power plants with the power purchase agreements or any other support schemes offered by government in the future;

• Universal service providers (the companies supplying households and other end-users);

• Regulated power plants (e.g. Enguri)

• Guaranteed capacity providers (e.g. TPPs)

Balancing and ancillary services market will start operation in Jul-21. TSO will define the requirements and the list of service providers. Imbalance fees and settlement rules will also be established by then.

By Mariam Chakhvashvili