ISET | Coronavirus Realities: Dismal Q2, Q3 Forecasts May Not Be Low Enough

ISET-PI has updated its Georgian real GDP growth rate forecast for the second and third quarters of 2020. Here are the highlights of this month’s release:

HIGHLIGHTS

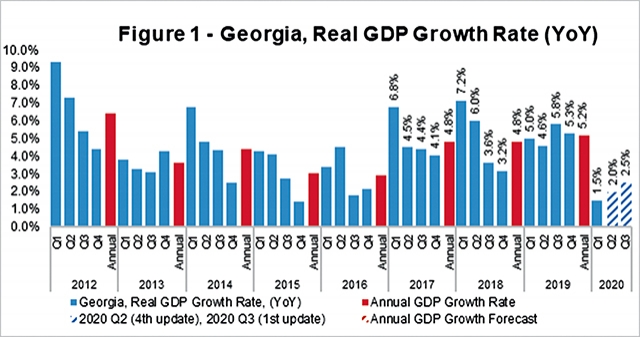

• Geostat has released its rapid estimate of real GDP growth for the first quarter of 2020, which stands at 1.5%;

• The estimated real GDP declined by 16.6% in April 2020 y-o-y and by 3.6 percent in the first four months of 2020. In April, the estimated real growth compared to the same period of the previous year posted negative in almost all activities, except mining and quarrying. Moreover, VAT payers’ turnover, used in rapid estimations of economic growth, dropped by 32.8% annually over the same period;

• ISET-PI predicted 2.0% and 2.5% growth for the second and third quarters of 2020, respectively, based on March 2020 data. This does not yet fully account for the negative impacts of the COVID-19 pandemic on the national economy;

• Consequently, the annual growth in 2020, from March data, is expected to be 2.1% in the worst-case scenario, and 2.5% in the best-case or an average long-term growth scenario. Our middle-of-the-road scenario (based on the average growth in the last four quarters) predicts a 2.3% increase in real GDP;

• COVID-19 is expected to impact the Georgian economy via tourism, remittances, trade, lower domestic production and service provision due to the strict social-isolation measures. According to the National Bank of Georgia (NBG) and the International Monetary Fund (IMF), Georgia’s annual real GDP growth forecast for 2020 amounts to -4%.

National and foreign currency deposits

In March, all national currency deposits (except current accounts) experienced notable growth in annual terms. In particular, national currency total deposits increased by 10.5% y-o-y, while foreign currency total deposits increased by 32.1%, compared to the same month of the previous year. The dollarization rates of non-bank deposits initially increased to 66.7% in March and then decreased to 65.9% in April. Our model suggests these trends in national and foreign deposits have had a significant positive contribution to real GDP growth.

Decline in domestic consumption due to behavioral and policy changes

I.e. people staying home as a precaution or as a requirement. A significant reduction in household consumption (e.g., spending on transportation, clothing, electronics, and domestic services) will likely have resulted in an overall slowdown of GDP growth.

Decline in domestic investment

Uncertainty and deteriorating business sentiments will stall commercial investment planning. Expectations of a global recession could become self-fulfilling if ‘business-as-usual’ does not resume within the next few months. If companies expect a slowdown in demand, they will also delay investment, and thus GDP will decline further.

External merchandise trade

In the face of the harsh measures, countries have taken to overcome the COVID-19 pandemic, trade of all commodities, except food and medicine, are projected to decline; depending on the duration of the shock. In March, Georgia’s exports declined by 22.1% y-o-y, while imports decreased by 13.4%. The trade deficit, however, shrank by 6.8% y-o-y, and amounted to 403.1 million US dollars.

Furthermore, deterioration of external trade was even more pronounced in April (not yet reflected in the model). Where Georgian exports declined by 27.9% compared to the same month of the previous year, driven by the reduced exports/re-exports of motor cars, cigarettes, and medicines to Azerbaijan; alongside declining export of wine and mineral water to Russia; the export/re-export of cars, alcoholic beverages, and mineral water to Ukraine; and the re-export of cars to Armenia. There was however a slight increase in the export of ferro-alloys to the United States.

During the same period, the import of goods decreased by 38.5%, driven by petroleum and related fuel products from Russia and Azerbaijan, motor cars from the United States and Germany, and reduced imports from Turkey and China. As a result, the trade deficit shrank by 46% compared to the same month in 2019 and amounted to 234.8 million US dollars.

Remittance inflows

Since all countries will suffer economically in the aftermath of the health and oil price crises, we expect a significant slowdown in remittance inflows from the rest of the world. The remittances decline will hit Georgia particularly hard as it is among one of the top receiving countries for foreign transfers.

Furthermore, in April remittances decreased by 43.3% y-o-y, reducing disposable income, consumption, and real GDP growth. The main contributors to the decline were the Russian Federation (-15.5 ppts y-o-y), Israel (-4.7 ppts y-o-y), Greece (-4.5 ppts y-o-y), Italy (-3.7 ppts y-o-y), the United States (-3.6 ppts y-o-y), Turkey (-1.8 ppts y-o-y), and Spain (-1.8 ppts y-o-y). Nevertheless, the European Union and Russia remain the top originators of financial inflows, accounting for 60.4% of total remittances.

International visits and tourism

Tourism arrivals and receipts are expected to decline sharply as a result of numerous travel bans, and due to precautionary behaviors. In addition, in April, the number of international visitors decreased by 93.8% y-o-y. While the decline in tourist numbers (visitors who spent 24 hours or more in Georgia) amounted to 92.3%. Consequently, the decreased monetary inflow and the dramatically reduced number of visitors and tourists made a significant negative contribution to the growth forecast.

The exchange rate

In March, the Georgian lari sharply depreciated in monthly terms against all main trading currencies. While in the following month, transactions in the foreign exchange market declined substantially and the Georgian lari slightly appreciated against other currencies, except the Russian ruble. The Real Effective Exchange Rate (REER) depreciated by 2.6% and 1.1% relative to the previous months in March and April, respectively (this pattern was also seen in the Nominal Effective Exchange Rate). Overall, REER-related variables had only a small negative contribution to the real GDP growth projections.

World prices

The final variables to have a negative contribution on the growth figure are the Metals Price Index (PMETA), the Agricultural Raw Materials Index (PRAWM), and the Europe Brent Spot Price (COP) . Metal forms a significant share of Georgia’s exports, while food and oil are one of the main import items. Therefore, a global decrease in the price of metal will likely deteriorate the Georgian economy, whereas a decrease in the price of agricultural products is more likely to be beneficial. In March and April, metal prices, in annual terms, decreased by 15.3% and 19.7%, respectively, while raw agricultural material prices declined by 6.2% and 7.8%, respectively in annual terms. The Europe Brent Spot Price FOB (dollars per barrel), decreased from 55.7 in February to 18.4 in April, and then increased slightly to 29.4 in May. Adding the PMETA, PRAWM, and the COP indicators to the model decreases the growth forecast in both quarters.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We have constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (the 1st vintage) is available around five months before the end of the quarter in question. The last forecast (the 5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych