ISET GDP Forecast | Trade Balance & Inflation Rate Improvements in Georgia

ISET-PI has updated its real GDP growth forecast for the fourth quarter of 2020 and the first quarter of 2021. Here are the highlights of this month’s release:

HIGHLIGHTS

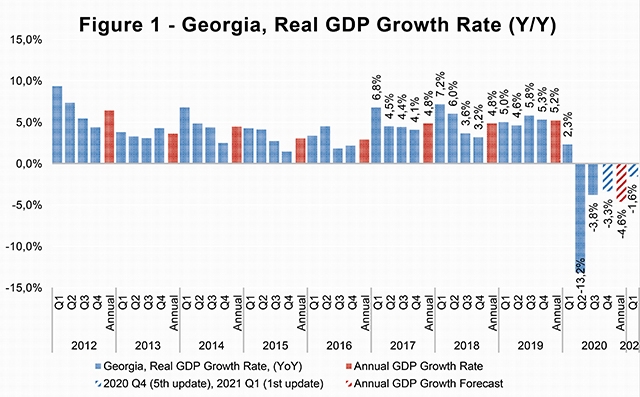

• The real GDP growth rate amounted to -3.9% year-on-year for October 2020. Consequently, the estimated real GDP for the first ten months of 2020 was -5.1%.

• Recently, GeoStat released its preliminary estimate of real GDP growth for the first and second quarters of 2020. The Q1 and Q2 growth rates were revised downward to 2.2% (by 0.1 ppt) and -13.2% (by 0.9 ppt) respectively.

• As a result of the update, the growth forecast for Q4 of 2020 remained unchanged, at -3.3%. ISET-PI’s second forecast for Q1 of 2021 puts GDP growth at -1.6%.

• Based on October’s data, we expect annual growth in 2020 to be -4.6%, which is 0.2 percentage points lower than the previous forecast.

According to ISET-PI’s recent forecast, GDP growth in the first quarter of 2021 decreased from -1.4% to -1.6%. This correction can mostly be explained by GeoStat’s downward revision of the Q1 and Q2 growth rates (by 0.1 and 0.9 percentage points respectively). Otherwise, from the standpoint of the October data, several variables changed significantly, which affected the growth predictions.

National and Foreign Currency Deposits.

The first set of variables with a moderate effect on our forecast relates to national and foreign currency deposits in commercial banks. All categories of national currency deposits (except currency in circulation) experienced growth in annual terms, while declining on a month-to-month basis in October. In particular, national currency demand deposits saw an annual increase of 3.5%, while time deposits increased by 73.6% annually. Consequently, national currency total deposits increased by 27.1% yearly. In the same time period, time deposits decreased by 0.6% in monthly terms, while demand deposits and currency in circulation decreased by 4.2% and 9.2% respectively compared to the previous month.

In contrast to domestic currency deposits, foreign currency total deposits increased relatively moderately by 19.4% compared to the same month of the previous year. In the same time period, nearly all categories of foreign currency deposits increased by more than 10% annually. The annual growth of foreign currency deposits is mainly driven by the sharp depreciation of the national currency. Nevertheless, growth rates are still pronounced even after excluding the exchange rate effect. As a result, deposit dollarization increased by 0.6 percentage points monthly and decreased by 1.7 percentage points yearly. Despite the positive annual trends, deposit-related variables still had a slight negative contribution to real GDP growth based on our model.

VAT Turnover.

As far as other variables of interest, VAT turnover in October decreased by 3.8% yearly and increased by 13.8% monthly. Consequently, this variable had a negative contribution to real GDP growth.

Real Effective Exchange Rate.

In October, the real effective exchange rate (REER) appreciated slightly by 0.8% monthly and largely remained stable in yearly terms. Notably, the lari real exchange rate depreciated with respect to the euro and dollar by 0.6% and 0.7% respectively in monthly terms and by 10% and 5.5% respectively in yearly terms. In contrast, REER appreciated with respect to the two major trading partners: Turkey (by 2.4% monthly and 17.1% yearly) and Russia (by 1.4% monthly and 11% yearly). Depreciation of the REER is typically associated with domestic export goods gaining competitiveness on foreign markets, but it also translates into increased prices on imported goods. Overall, REER-related variables had a small negative contribution to the real GDP growth projections.

Foreign Trade.

In October, Georgia’s exports experienced a slight 2.2% annual decline, which was mainly driven by decreased export/re-export of motor cars and trucks and alcohol spirits to Armenia; motor cars, tobacco, and carbon steel rods to Azerbaijan; motor cars, medicines, natural grape wines, and mineral waters to the Kyrgyz Republic; and ferro alloys and frozen lamb/goat meat to Iran. At the same time, Georgian exports to China (due to increased export/re-export of precious metals as well as copper ores and concentrates), and Saudi Arabia (due to increased export of living animals) increased substantially.

During this period, the import of goods decreased by 23.5%, driven by a reduction in petroleum and fuel product imports from Russia (mostly due to a significant annual reduction of crude oil prices on the international market). Among other affected imports were: motor cars from the USA; copper ores and concentrates from Brazil; oil coke-bitumen and paving slabs from Iran; and motor cars from Germany. In contrast, Georgian imports of precious metals and concentrates from Armenia; oil and copper ores and concentrates from Azerbaijan experienced yearly growth. Consequently, the trade deficit shrank dramatically by 34.8% yearly, and amounted to $393.5 million. Overall, trade-related variables had a positive contribution to the GDP growth forecast.

Money Inflow.

After a significant slowdown in remittance inflows in the beginning of the year, money inflows have been on the path to recovery since June. In October, remittances increased by 18.6% annually and reached $181.7 million. The main contributors to this increase were Ukraine (by 151.9% YoY, contributing 4.3 ppts), Italy (by 30.9% YoY, 4.2 ppts), USA (by 39.5% YoY, 3.9 ppts), Greece (23.6% YoY, 2.5 ppts), Germany (by 74.6% YoY, 2.2 ppts), Azerbaijan (by 145.1% YoY, 2.1 ppts), and Turkey (by 26% YoY, 1.4 ppts). Whereas money inflows decreased from the Kyrgyz Republic (by 83.1% YoY, -1.7 ppts), Russia (by 7% YoY, -1.7 ppts) and Kazakhstan (by 44% YoY, -0.9 ppts). The recovery of remittance flows made a significant positive contribution to the growth forecast.

International Visits and Tourism.

Tourism arrivals and receipts declined sharply as a result of numerous travel bans, as well as due to precautionary behaviors on the part of potential tourists. In October, the number of international visitors decreased by 92.5% yearly (driven by Russia [-17.1 ppts], Azerbaijan [-17.4 ppts], Armenia [-16.8 ppts] and Turkey [-10.2 ppts]) , while the decline in tourist numbers (visitors who spent 24 hours or more in Georgia) amounted to 88%. Overall, dramatically declining numbers of visitors and tourists, along with a sharp decrease in touristic spending, has made a significant negative contribution to the growth forecast.

Inflation.

In October, annual inflation of consumer prices amounted to 3.8%, which is only slightly higher than the targeted 3%. Notably, inflation converged to the targeted value at the end of 2020. Approximately 1.5 percentage points of CPI inflation were related to higher food prices (5.4% annual increase), while tobacco prices contributed 0.4 percentage points (13.5% annual growth). However, decreased oil prices (16.7% annually) made a notable negative contribution (0.6 ppts) to the annual inflation measure. The latter trend is mostly a reflection of significantly weakened oil prices on the global market (Europe Brent Spot Price (COP) decreased by 32.7% yearly). Overall, CPI-related variables had a positive contribution to the GDP forecast.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We have constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time passes. Our first forecast (the 1st vintage) is available around five months before the end of the quarter in question. The last forecast (the 5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych