Colliers Int'l Georgia Launches 'Recov.ge' to Support Real Estate Players during Pandemic

The global pandemic has significantly impacted almost all fields of the economy, including the real estate sector. Given the conditions of uncertainty, due to the ongoing effects of the pandemic, real estate players are looking for solutions.

Colliers International Georgia, a leading commercial real estate services company, providing a full range of services to real estate occupiers, developers and investors on a local, national and international basis, has launched a new non-commercial platform named recov.ge, aimed at supporting the real estate industry to recover with a minimum loss from the outcomes of COVID-19. Through this platform, the company shares its deep knowledge and expertise with those involved in various economic activities, the goal being to strengthen and inform them throughout this difficult period. On this platform, users can learn about the impact of COVID-19 on the Georgian real estate market and take a look at a dynamic analysis of the office, residential, retail & leisure, and hotel sectors. Along with a sectoral analysis, the platform offers an overview of the country’s tourism and economy, perspectives for domestic tourism, the impact of COVID-19 on neighboring countries, and an analysis of the most exposed sectors from which Georgia has benefited from foreign direct investment. These sectoral and general overviews and dynamic analyses assist platform users to make informed decisions.

The observations available on the website are based on foreign best practices, the expertise of Colliers International Georgia and other international offi ces, as well as continual interaction with industry players. The analysis and outlooks refer to two main periods:

• THE ISOLATION PERIOD: The different degrees of isolation within Georgia and worldwide;

• THE UPCOMING PERIOD OF RECOVERY: Getting back to the old rhythm of life; The recovery stage of global and local economies as they adjust to the new reality.

Notably, Colliers International added the 2018-2019 sectoral studies to the platform, which made the year-old and current positions on Georgia’s real estate market easier to visualize. Further, work is underway to make the platform more interactive, giving representatives of the field the chance to participate in surveys, offer opinions, and take part in group discussions and practical courses.

With these features, the platform aims to shine a spotlight on the critical issues, and expose the ongoing challenges; to determine the aspects in which industry players need governmental support, and the directions in which they need recommendations from Colliers.

This platform is a space with the potential to become an incubator of ideas; which will, in the short-term, act as a functional core, and in the long-term as a rehabilitative haven for the industry.

The platform is being updated constantly by the employees of Colliers International, who have been working tirelessly during the pandemic period to provide maximally useful and relevant information to those in need by using their knowledge and reliable experience.

The informative studies conducted by the company include some important insights and findings about the current conditions, inflicted damage and future recovery prospects of the Georgian economy. In particular, the research concludes that in recent years, the real estate market as a whole has been growing steadily.

Events caused by the spread of COVID-19 virus all over the world and in Georgia have stopped this growth. Restrictions caused by the pandemic since March have affected all sectors.

• More than 70% of Georgia's tourism is income from international tourists. In the absence of tourism, the hotel and food sectors, especially those focused on international tourists, have been and will be significantly affected. However, it should also be noted that in parallel with the pandemic, the intensification of local tourism has turned out to be a significant relief for resort areas this year.

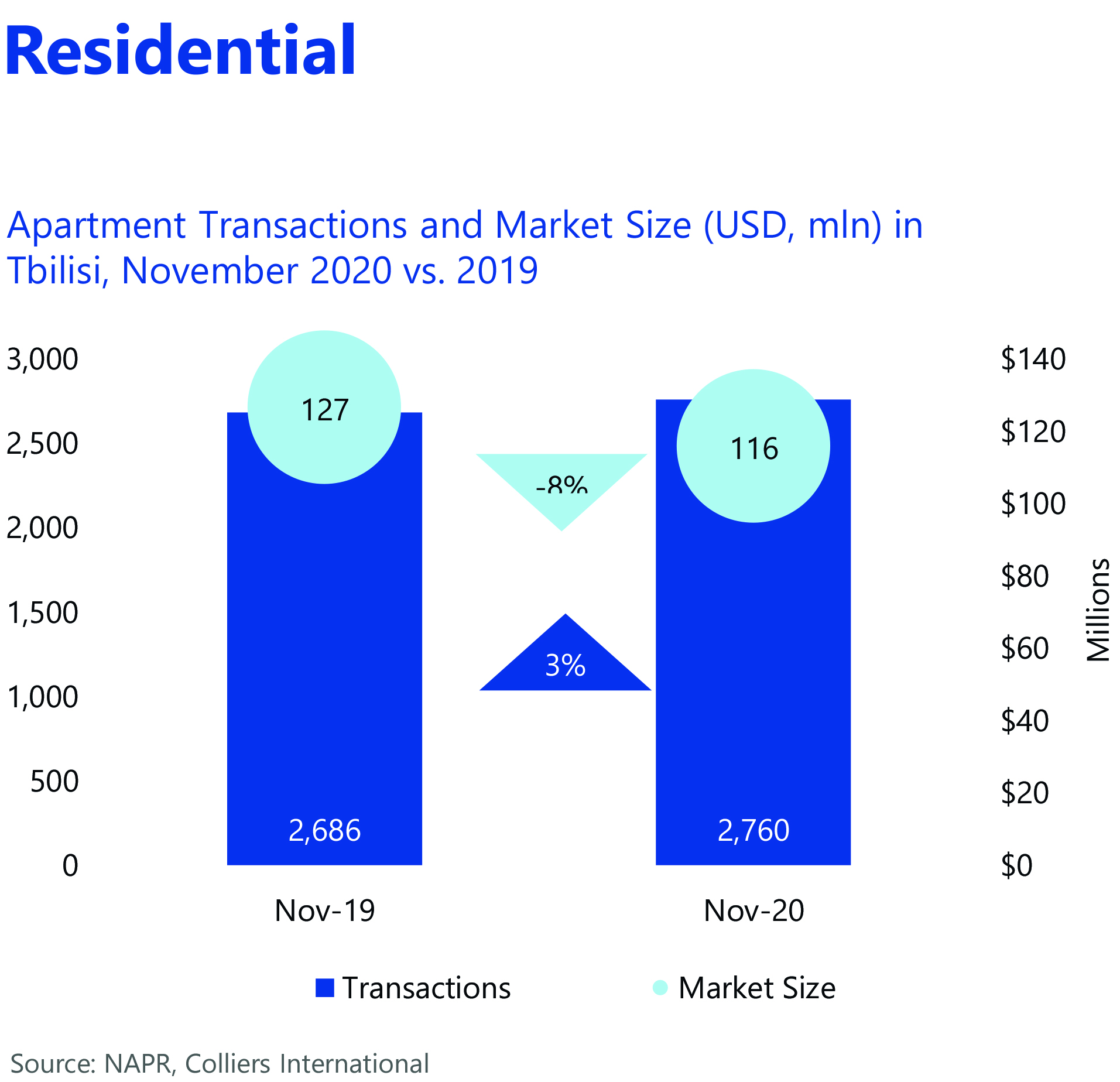

• The positive trend in the market recovery is the residential real estate market. In Tbilisi, in October 2020, 2,760 transactions were registered, which is 3% more than the previous year. Regarding the market volume, a 4% decrease was recorded, with a volume of $116 million. The medium and premium segments of newly built apartments are 26% and 49% lower than the same period last year. As for the economy segment, the number of transactions increased by 14% and reached 2,318.

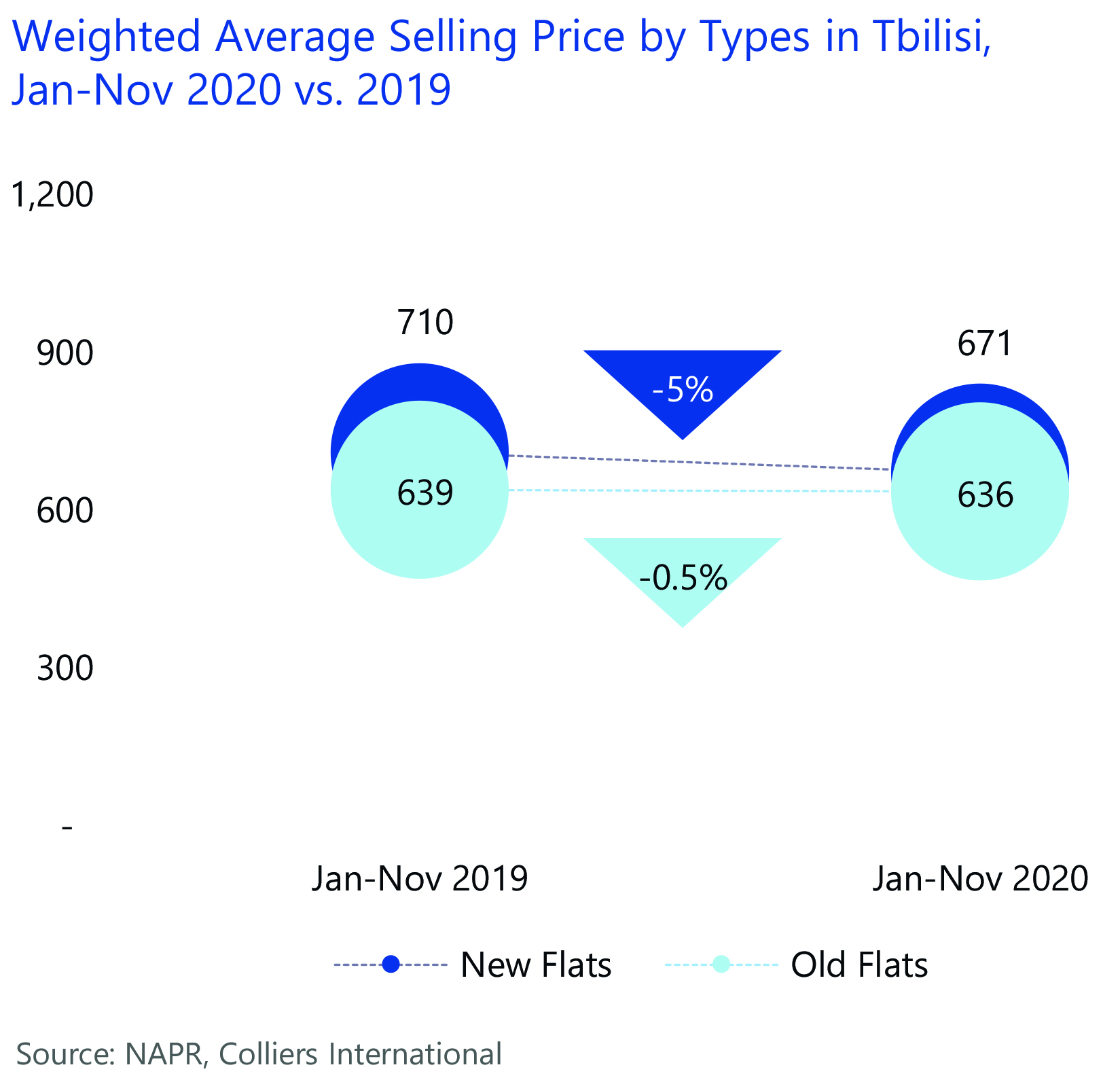

The number of newly built apartments is 17% less than the same period last year, while the number of transactions registered on old apartments decreased by 26% to 7,816 units. In January-November 2020, the market size of newly built apartments decreased by 22% compared to the same period last year and amounted to $753 million. And in the case of older apartments, a 27% decrease was observed and the market size was $309 million. In January-November 2020, the volume-weighted average sale price of newly built apartments decreased by 5% compared to the previous year and amounted to $671 per sq.m. Regarding old apartments, the volume-weighted average price decreased slightly, by $3 per sq.m., to $636. From March 22 to November 30, 2020, the number of transactions registered on newly built apartments signifi cantly decreased in most parts of Tbilisi. Slight decreases were observed in the Nadzaladevi and Didube districts, 6% and 9%, respectively. The exception was Gldani, where the number of transactions increased by 32%. In contrast to newly built apartments, the number of transactions registered on old apartments signifi cantly reduced in all districts of Tbilisi. The biggest drop was observed in the districts of old Tbilisi, such as Chugureti -45% and Mtatsminda -44%.

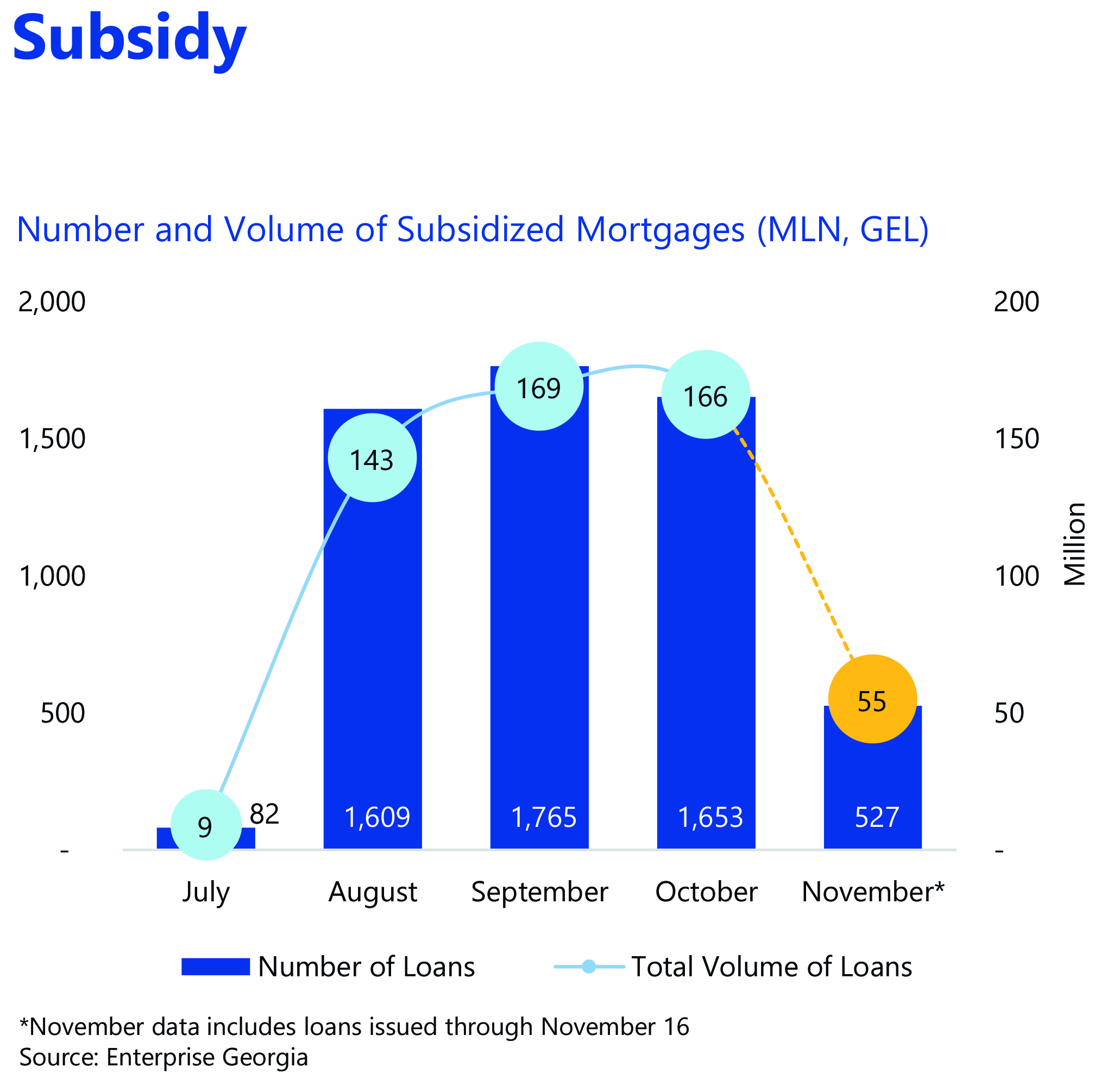

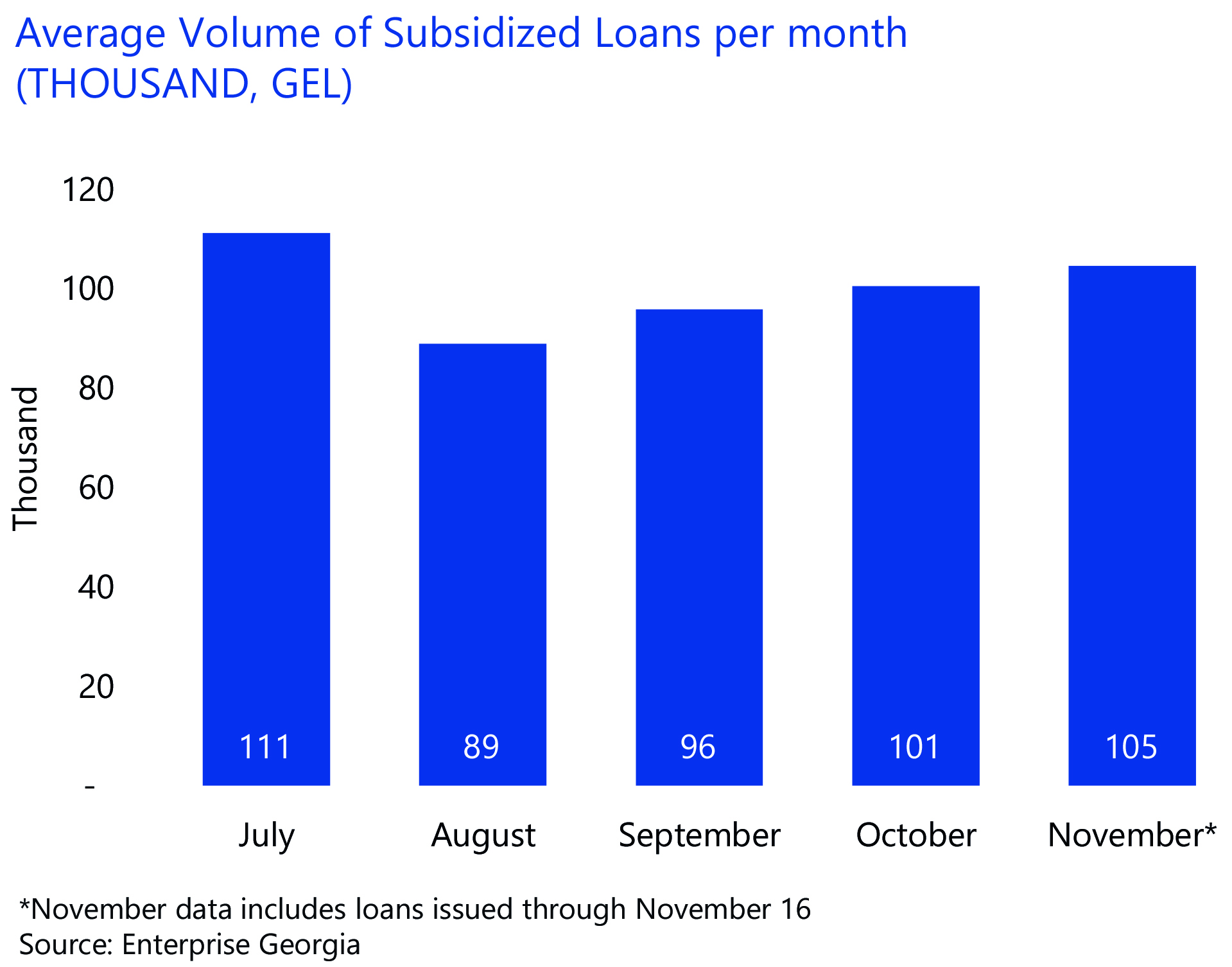

The state subsidy program "Mortgage Loan Support Mechanism" was launched on July 1, 2020. Under the program, it is possible to use a 4% annual mortgage interest rate subsidy for 5 years. The maximum loan repayment period was 240 months. A total of 5,636 loans were issued under the program from July 1 to November 16, with a total volume of approximately GEL 543 million.

The peak month during this period was September, when a total of 1,765 loans were subsidized, totaling GEL 169 million. Regarding the average volume of loans, this figure ranges from 89 thousand to 110 thousand GEL. Based on the above, the subsidy program mainly helps the economic segment of the residential market. According to the National Bank, in total, subsidized loans account for 30-35% of mortgage loans issued during this period.

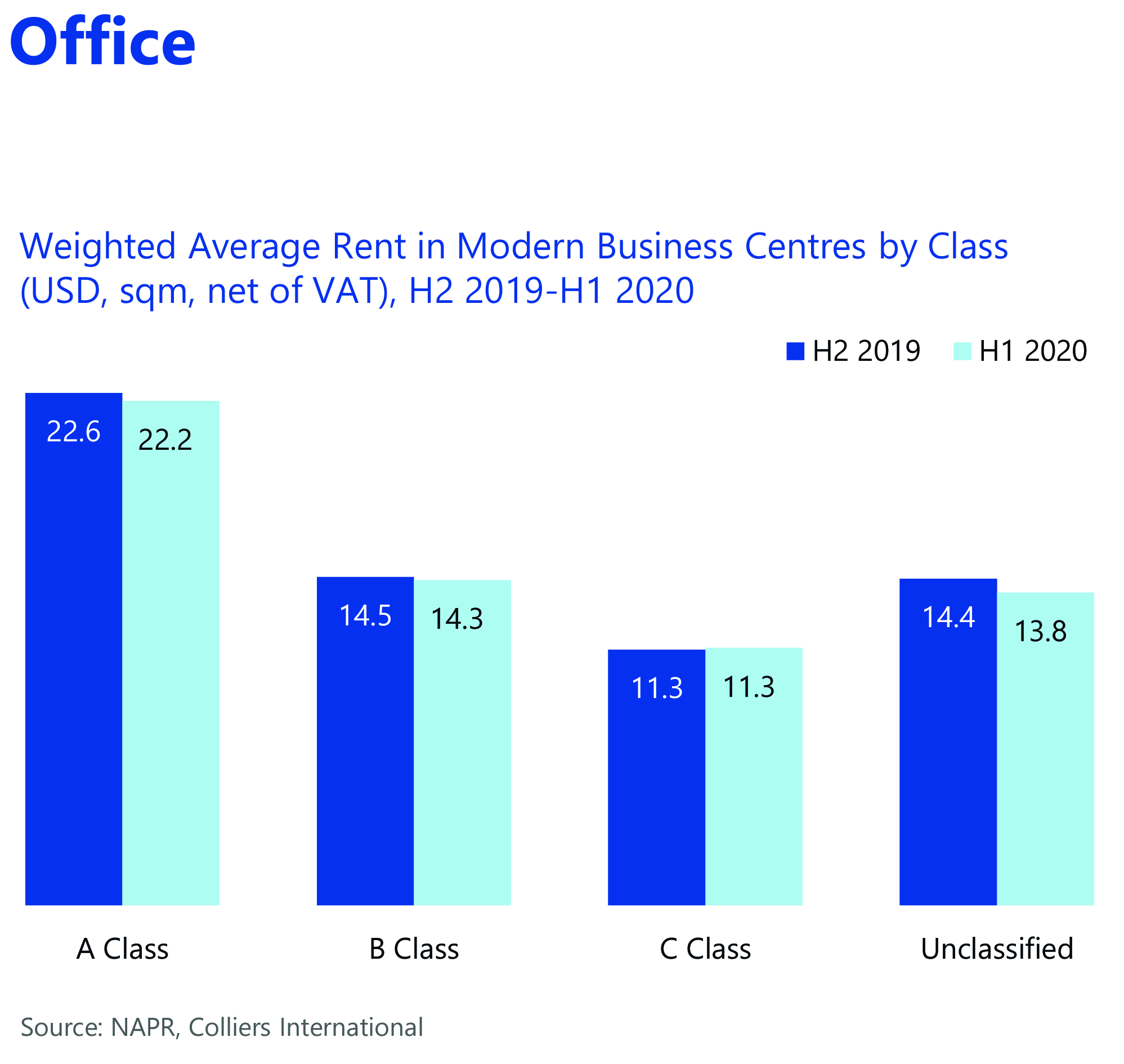

In 2020, the supply of offices increased significantly with the opening of new business centers on Chavchavadze Avenue, Vake district, although the pandemic changed their opening plans in terms of time. In general, when tenants and landlords of business centers communicate, there is a trend of relocations and rental price revisions. Bilateral movement from high class to middle class, and from low and middle class to high class, is expected. However, the real movement will appear early next year.

In early 2020, weighted average leases fell the most in unclassified business centers, by 4% to $13.8 per square meter. The figure fell by 2% in Class A business centers to $22.2, with a 1% decrease in Class B to $ 14.3 per square meter, while in Class C the figure remained unchanged at $11.3. Prices for new lease agreements in business centers have reduced in the range of 10% -30%.

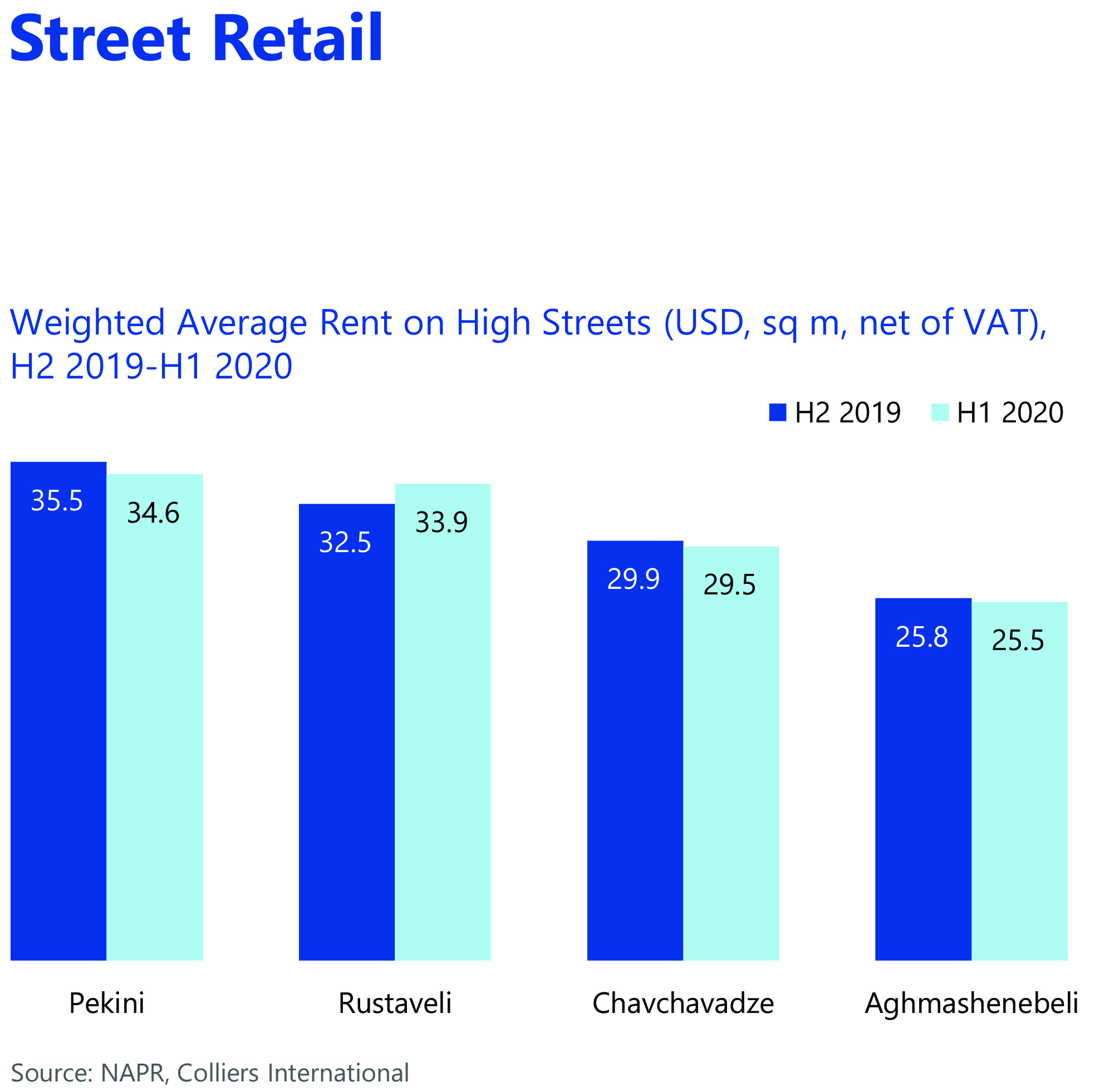

Regarding commercial real estate, the power of negotiation is on the side of the tenants, and here flexibility becomes the main game rule in the relationship. In the first half of 2020, the vacancy rate on major streets increased significantly, with about 60 units of retail space being vacated, totaling 7,000 sq.m. The weighted average lease also reduced, the reduction in existing lease contracts being in the range of 10% -20%, while in new contracts it ranges from 25% -35%. Shopping malls also face challenges.

In the first half of 2020, there were no significant changes in terms of vacancy rate in shopping malls, although it was largely due to the fact that during the pandemic and state of emergency, preferential discounts were made for tenants by mall operators, and in some cases they were exempted from monthly fees completely. Naturally, it is difficult to make predictions about 2021. Developments will depend on the degree of restrictions, the availability of medical solutions, and currency fluctuations.

Colliers forecast concludes:

2020 - uncontrolled pandemic

2021 - controlled spread

2022 - medical solution

2023 - return to NEW NORMAL