Mass Family Gatherings in Georgia: Tradition of Waste or a Form of Insurance?

There is a Georgian joke that goes: “Relatives are the people you see whenever their number changes”. In other words, relatives all tend to gather when any of them gets married, gives birth or dies. As a result, we frequently observe Georgians organizing mass gatherings to either celebrate or mourn numerical “changes” in their families. While there is a recent trend among the wealthier and better educated people to switch to more intimate, smaller events, the poorer rural people continue to arrange Georgian supras of monumental proportions.

A FORM OF CONSPICUOUS CONSUMPTION?

When attending Professor Omer Moav’s lecture on Economic Growth which classified large Indian weddings as a form of “conspicuous consumption”, I started wondering whether the Georgian tradition of mass family events can also be considered in the same manner. Moav defined conspicuous consumption as consumption of goods which serves to show off one’s economic prowess without providing any positive economic benefits. He further argued, based on economics analysis, that it is the poor who are more likely to engage in acts of conspicuous consumption in order to pretend that they are not who they are (poor).

Prima facie the grand Georgian supras seem to fit this definition: the poor who organize mass funerals could have invested their scarce resources in much more profitable ways, for instance by investing in own health or education for their children. Organizing funeral feasts for hundreds of guests by the poor could be thought of as a form of showing off. What also makes these events akin to conspicuous consumption is the fact that this tradition is increasingly losing favor with the wealthier and better educated Georgians.

IS IT SOMETHING ELSE?

Despite many similarities there is one feature that clearly distinguishes these Georgian mass gatherings from typical cases of conspicuous consumption: the fact that guests, including relatives, neighbors and other acquaintances are expected to make a sizeable financial contribution. This kind of arrangement makes these events more like an insurance scheme, rather than “bling-bling” consumption.

A Georgian family would normally keep a detailed record of guest contributions at an event such as a funeral or a wedding, being prepared to reciprocate in case of need. Given the long-term nature of the resulting financial commitment, it is not surprising that wedding and funeral contributions are enshrined in the Georgian tradition. One might even perceive such payments or gifts as a membership “fee” for being a part of a “club” brought together by kinship or social bonds.

However, I would argue that the emergence of this type of club behavior is driven by the insurance motive: you help others when they are in need and thus expect to get help when it is needed for you. As I found out, similar community-based insurance schemes in the form of funeral contributions can also be found in the likes of Ghana, Ethiopia, Tanzania and other developing countries.

WHY INSURANCE?

Insurance is a form of risk management that is primarily used to hedge against the risk of a contingent, uncertain loss. People crave for safety when facing uncertainty, and death is a rather uncertain event (at least as far as timing is concerned). The ancient Romans are said to have been the first civilization to use insurance to cover the costs of funerals. Today, people who do not want to overburden their offspring with funeral expenses may take life insurance. A community-based insurance through the tradition of funeral contributions may be a handy alternative.

Some categories of people are less likely to purchase a formal life insurance. These are: the poor who cannot afford an insurance product; people belonging to strong and supportive family units; people who do not place trust in financial institutions and would rather participate in a community-based insurance arrangement with people they trust (relatives, neighbors, etc.), or people who have superstitions associated with death and are reluctant to consider any associated arrangements in advance.

Weddings also pose a financial challenge for families and are difficult to plan sufficiently in advance. As financial markets are yet to come up with a wedding insurance (at least in Georgia), poor families have the choice of having a large, community-supported wedding; a modest, affordable wedding; or no wedding at all.

Economic analysis has it that the poor are more likely to opt for funerals and weddings financed by community-based insurance schemes and will therefore tend to arrange mass social gathering. Similarly, the more educated families (who have fewer superstitions about death), and higher-income individuals, are more likely to switch to market-based insurance (or save).

FROM FUNERAL CONTRIBUTIONS TO LIFE INSURANCE

There is a lively debate within Georgia whether the tradition of “qelekhi” – the feeding of guests before, during or after a funeral – should be retained or not. For the older generations, this tradition is meant to show respect to the deceased. At the same time, many younger people may consider such meals and associated drinking to be a direct insult to the mourners. For many, compassion from hundreds of people is not a necessary condition for the mourning of a loved one. Moral considerations about “qelekhi” aside, funerals would have been far cheaper without this tradition. In any event, more modest qelekhi attended by a smaller number of guests, would help cut the costs incurred by the relatives of the deceased.

The tradition of qelekhi is more likely to survive in large, tightly knit, poor communities where it plays a more important insurance role and where defection (refusal to contribute) is more costly to the individuals involved. In wealthier and more educated urban circles, families are more likely to free themselves from the need to accept or make funeral contributions. By relinquishing this communal bond, such families undertake to finance own family contingencies with their savings or with the help of insurance.

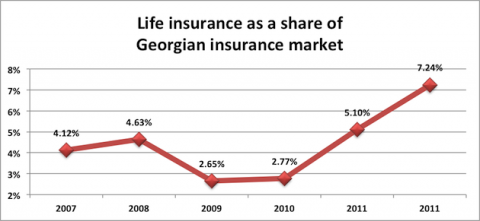

As Georgians grow wealthier over time, they will be more likely to switch from informal community-based insurance to life insurance products offered by insurance companies. This has been the trend elsewhere in the world, and to some extent may be already happening in Georgia, judging by the share of life insurance in total insurance.

Nino Doghonadze

![]()