Oil Prices: Falling Again

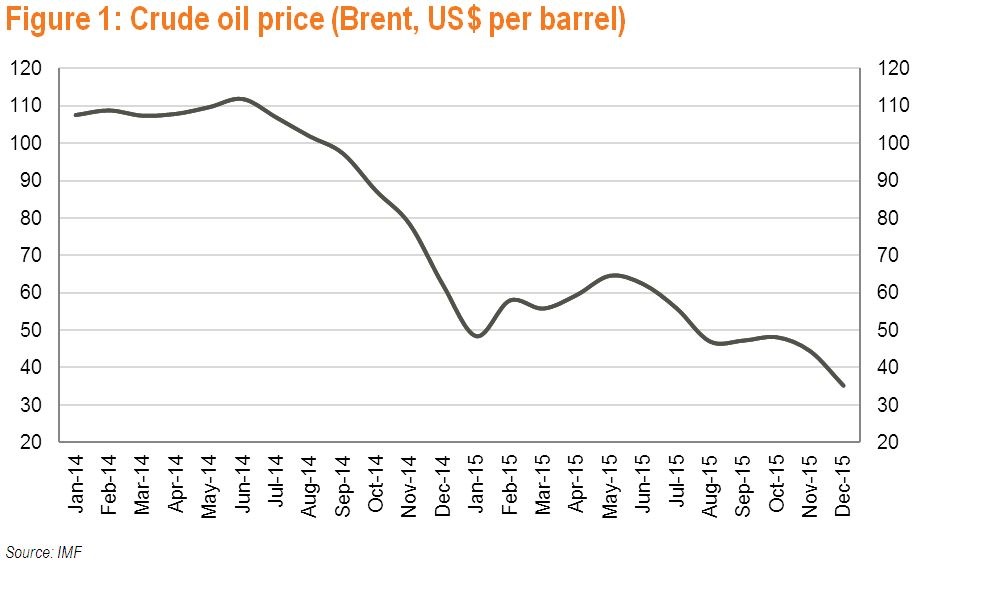

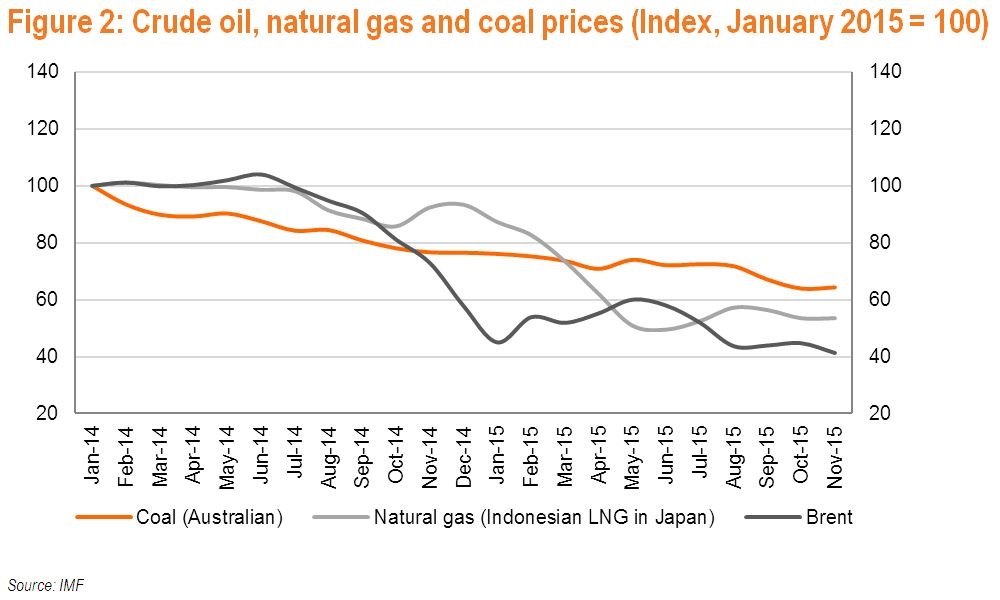

Oil prices keep falling, below all previous projections and expectations. The price of Brent crude sank to US$34.8 per barrel on December 21, the lowest level since May 2004. This is 44% and 69% percent lower than the prices in June 2015 and June 2014, respectively. Natural gas and coal prices followed the trend, but fell by less as these fossil fuels are generally priced through oil-indexed contracts with some lag. Such a sharp drop in oil prices is not unique. Reflecting various geopolitical, economic and security factors, “Black Gold” prices have fallen sharply three times in the near past: in 1985-86, in 1990-91, and in 2008-2009.

Low oil prices are good for the global economy, because they translate into lower cost of production, thus boosting profits and savings and enabling higher investments. A period of low oil prices is also a good time for the reduction of energy subsidies which were at US$548 billion (0.7 percent of the world GDP) at end-2013.

Projecting medium to long-term oil prices has often proved to be an unsuccessful endeavor because of the variety and complexity of factors affecting the price movement. Instead, let’s look at the reasons behind the recent oil price collapse and try to understand if low prices are likely to persist.

Why did oil prices plunge?

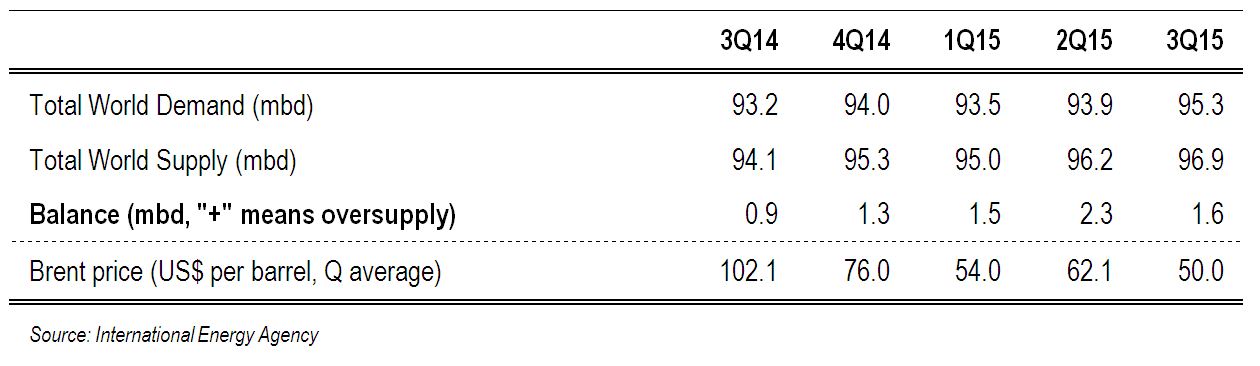

Slowdown of the global economy is the main demand factor behind the fall in oil prices. Global economic growth is projected to decelerate from 3.4% in 2014 to 3.1% this year, implying a weakening demand for oil. More importantly for the oil sector, 2015 growth in emerging economies—main consumers of the growing oil production—is projected to decline for the 5th consecutive year to 4% compared to 4.6% in 2014. Based on the BP database, the annual oil consumption growth in 2014 fell to 0.9% compared to an average annual growth of 1.8% during 2010-2013. The IEA estimates global oil demand in the last quarter of 2015 to increase by only 1.3 million barrels per day (mbd) from a year earlier, which is significantly lower than the 2.1 mbd annual demand growth registered in the third quarter of this year.

Emergence of US shale oil appears to be the strongest supply factor that contributed to the drop in oil prices. Thanks to the so-called "shale revolution", a new horizontal drilling technology that enables extraction of oil from tight rock formations, the US has added about 4 million barrels (about 5% of 2014 oil production) of unconventional crude to oil markets over the last four years, making the US the world’s largest oil producer in 2014. Shale oil production has a considerable advantage over conventional oil drilling. It requires a relatively low capital cost and has a much shorter life cycle (3 years) between the first investment and production compared to a decade or longer needed for conventional oil drilling. Moreover, unconventional shale oil producers can adjust output levels reasonably quickly to changing demand.

A shift in the strategic behavior of the Organization of Petroleum Exporting Countries (OPEC), accounting for 40% of the world’s oil supply, is another important contributor to the current supply glut. OPEC, and in particular Saudi Arabia, abandoned its traditional role as the global oil market's swing producer—a supplier with spare capacity that can influence market prices by adjusting output—by leaving the production quotas unchanged in the face of growing non-OPEC supplies a year ago. Some analysts argued that Saudi Arabia’s decision was aimed at slashing the profits, and ultimately the oil production, of the US shale oil producers with relatively high extraction costs. While falling oil prices will force some shale oil producers out of business, Rystad Energy, an oil and gas consulting company offering analysis of the global databases, is of the view that US shale production has so far remained economical despite the drop in oil prices as the breakeven price—the minimum price level at which extracting oil remains profitable—for shale oil has also been falling every year. OPEC’s decision to maintain its collective production target unchanged in its recent meeting kept the oil market oversupplied and pushed the prices further down.

Some geopolitical events also supported the increase in oil supply. Against many analysts’ expectations, crude oil production recovered quickly in Libya despite unrest and elevated security concerns. Invasion of Iraq by the Islamic State militants in June 2014 did not disrupt the oil production of OPEC’s second largest producer as the conflict did not spread to the south, where the country’s largest oilfields are located. Furthermore, Russian crude oil production has recently reached a post-soviet record high despite sanctions following the Russia-Ukraine conflict.

Overall, while both supply and demand factors played a role, the supply side factors appear to have weighed more on the recent drop in oil prices.

What’s next?

Given the dominance and size of the supply factors in the recent collapse of oil prices, oil producers’ investment decisions will largely shape the longevity of the current low oil price cycle. A long period of high hydrocarbon prices can create preconditions for them to fall: high oil prices encourage massive investments in new production capacities that can lead to a sharp increase in production and result in global oversupply of oil. The residual oil is stockpiled, providing comfort to oil consumers and pushing oil prices down. According to the Rystad Energy analysis, the current oil supply glut and collapse in oil prices are direct consequences of overinvestment by the oil and gas industry in 2013 and the first half of 2014. Oil and gas companies invested as much as 900 billion USD in exploration, drilling, field development, and field maintenance in 2013. OECD crude oil inventories, according to the IEA, were at a record high 3 billion barrels at end-September 2015.

Based on the same logic, falling oil prices should lead to lower capital investments in the oil sector and impact future oil production with some lag. Rystad Energy reports that fearing plunging oil prices, global oil companies have cancelled or deferred about US$175 billion future upstream investments by mid-2015. Overall, global exploration and production spending has been cut by US$250 billion in 2015 versus 2014 and a further US$70 billion reduction is projected for 2016. These cutbacks will eventually slow down the growth of oil supply and put upward pressure on oil prices. Expected higher growth of emerging economies in 2016 (4.5 percent) will also push up global demand for oil.

Three additional factors could influence the global oil prices in the near future. First, last week the US congress removed the 40-year old export ban on crude oil exports. This means that US producers will soon be able to export light crude oil to already oversupplied international markets. Second, Iran’s likely return to the global oil market in 2016 is expected to increase global supply of oil, causing global oil prices to ease. Third, the US Federal Reserve Bank’s recent increase of the policy interest rate is likely to keep the US dollar strong, which will also support low oil prices.

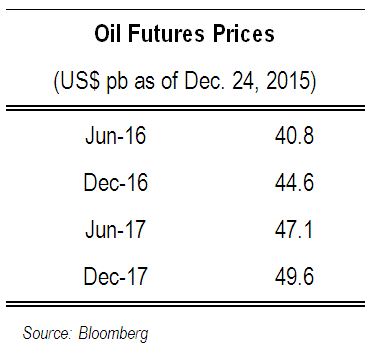

The above factors suggest that while gradually recovering from the current level, oil prices can be expected to stay relatively low for some time. A good way to sense where the oil prices are heading is to look at the futures’ prices as they reflect market participants’ expectations. The Brent futures contracts dynamics as of today show that the market participants expect a slow recovery in oil prices. The moderately upward sloping futures prices will supposedly discourage risky and bold investment in the oil sector, but provide enough incentives to carry on the ongoing projects and start investing in new viable ones.

Last, but not least

While supporting global growth, low oil prices, unfortunately, promote usage of energy intensive technologies in industry and agriculture, thus causing environmental damage from production of fossil fuels and increasing emissions of carbon dioxide and other greenhouse gases. More importantly, low hydrocarbon prices provide little incentive to policymakers to fund research and development of renewable (hydro, solar, wind) sources of energy and cleaner energy technologies. Introduction of a tax on carbon is often suggested by economists to reduce the environmental damage from carbon emissions. Until this happens, however, let’s hope that the recently adopted United Nations Climate Change Conference Paris declaration, which aims to transform the energy sector by accelerating investments in cleaner technologies and energy efficiency, will bring tangible results even in the environment of low oil prices.

Koba Gvenetadze (Galt and Taggart)

Disclaimer: on leave from the International Monetary Fund (IMF). The views presented in this article do not represent those of the IMF or its Executive Board.