Electricity Market Watch

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of Energy, Healthcare, Tourism, Agriculture, Wine, and Real Estate sectors in Georgia. As part of our energy sector coverage, we produce a monthly Electricity Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

The Ministry of Energy releases Georgia’s Energy Strategy 2016-2025

Ministry of Energy has just released Georgia’s Energy Strategy for 2016-2025. Both the ministry and the regulator (GNERC) were actively involved in the two-year process of developing the strategy document, with NGOs and industry experts contributing in the document review process.Liberalization of energy markets, move to day-ahead trading, approximation to EU’s Third Energy Package, and modernization and development of transmission and distribution infrastructure are some of the key themes. The strategy stresses the importance of expanding installed capacity in order to reduce the country’s dependence on imported energy resources. Aside from hydro resources, the potential of alternative energy source development, such as wind, solar, biomass and geothermal is also discussed. Notably, upgrading system capacity is key to securing the integration of wind and solar into the grid. Importance of strategic HPPs, such as Nenskra, Khudoni, and Namakhvani, for the upgrade of system capacity is highlighted. The natural gas reservoir near Tbilisi is an integral part of the strategy, as it will strengthen Georgia’s energy security by creating a buffer in case of natural gas shortage. The reservoir is to be built by GOGC, while interested investors can obtain minority stakes. Lastly, strengthening international relations is highlighted as an important step on Georgia’s path to becoming a regional electricity transit and renewable energy trade hub.

Agreement with the Energy Community to be ratified in early 2017

The membership agreement with the European Energy Community is expected to be ratified by the Georgian parliament in early 2017. Prior to the parliamentary hearing, Georgia has to be admitted as a full member during the Energy Community ministerial in October. Upon full membership and parliamentary ratification, Georgia will be obligated to start implementing a set of new legislative documents. Compliance areas will include, but not be limited to, liberalization of energy markets, supply quality and security, energy efficiency, and environmental considerations.

Guaranteed power purchase period reduced for Tkibuli 150 CFPP

The PPA for Tkibuli 150, a coal-fired power plant (CFPP), has been amended. The guaranteed PPA period was reduced from 20 to 15 years and the number of guaranteed purchase months from twelve to nine (August through April). The amendment was signed by both parties on July 4th and made public by the ministry in early August. The installed capacity allowance was also amended from 150 MW to 150-300 MW, but the PPA is capped at a 150 MW capacity. The guaranteed purchase prices were left unchanged at USc 7.9 per kWh in year 1 and increasing to USc 9.2 per kWh in years 12 and after.

Wind power to hit the grid end of 2016

A generation license was granted to Qartli WPP, expected to launch in test mode in October 2016. The construction process is almost complete. The WPP is made up of six wind turbines, each with 3.45 MW installed capacity. Project costs amounted to US$ 34.3mn. EBRD financed US$ 24mn through a senior loan and the rest was financed by the state-owned Georgian Energy Development Fund (GEDF). GEDF is working on four other wind projects, partnering with the Turkish Calik Wind on two of them. However, upgraded transmission infrastructure and increased system capacity are necessary precursors to alternative energy development on a significant scale. The current network capacity for wind and solar power plants is 50 MW, but expected to reach 400 MW by 2025, according to the new energy strategy document.

Nation’s largest dam expected to close for three to four months in 2018

Enguri HPP will halt operations for two to three weeks in 2017 and for three to four months in 2018 due to planned renovation. The renovation works are usually completed every ten years. Enguri supplies a substantial amount of Georgia’s electricity, varying from 150 gWh (up to 20%) in the winter months to 550 gWh (over 50%) in the summer months, and 100% of the Abkhazian region’s electricity consumption. Measures will have to be taken to bridge the gap during these months. Notably, in the beginning of 2016, when the Abkhazian region experienced an electricity shortage due to lower water levels in the Enguri reservoir, GoG struck an agreement with Russia to import electricity at a discounted price – a likely option for the Abkhazian region during the renovation.

Domestic consumption rallies as Georgian Manganese gets back to business as usual

Domestic consumption increased 6.8% y/y in July 2016, with DNOs and eligible consumers the major growth drivers. Consumption of eligible consumers was up 12.1% y/y, with Georgian Manganese (+25.9% y/y) driving the growth, while GWP’s consumption decreased 3.9% y/y. GM’s high growth can largely be attributed to the low base in July 2015, when consumption was down 28.5% y/y due to unfavorable conditions on global ferro-alloy markets. DNO consumption increased 5.6% y/y, with the greater Tbilisi area posting an impressive 17.5% y/y growth rate from an already high base in July 2015 (+ 5.7% y/y). Usage of Energo-Pro subscribers was flat (+0.7% y/y), while Kakheti Energy Distribution usage was down 3.2% y/y. Consumption of the Abkhazian region was up 9.2% y/y, after strong growth in June (+14.8% y/y) and three consecutive months of flat or negative growth figures before that.

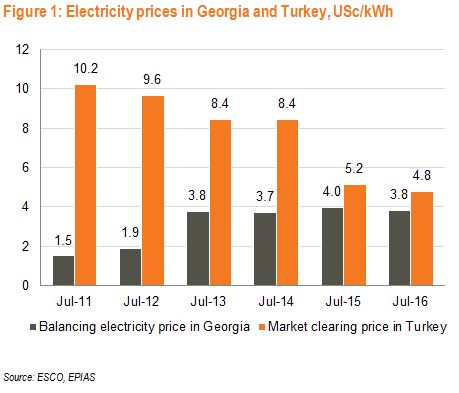

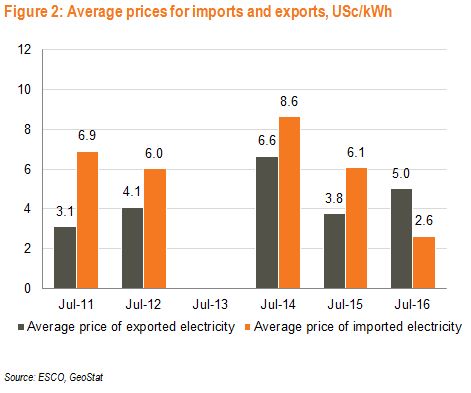

Turkey still the most attractive market for Georgian electricity exports

Electricity exports decreased 22.3% y/y in July 2016, with Russia driving the decline. Exports to Russia decreased 93.7% y/y from 63.3 gWh in July 2015, while exports to Turkey increased 21.9% y/y to 99.0 gWh, partly compensating for the drop in exports to Russia. This dynamic can be explained by the fact that average export prices to Turkey were up and average market price for electricity on the Russian market (USc 2-3/kWh) was below both Georgian and Turkish prices. Furthermore, domestic consumption in Georgia increased, while generation was largely flat, incentivizing the generators to either sell their electricity domestically or export to Turkey, before exporting to Russia. Subsequently, 76.8% of exports were directed to Turkey, 3.1% to Russia, 17.6% to Armenia (+5.8% y/y), and the rest, a negligible amount, to Azerbaijan.

Average price for Georgian electricity exports up 33.4% y/y

Average export price of Georgian electricity to Turkey increased 10.8% y/y (USc 5.0/kWh) in July 2016, despite a 7.0% y/y decrease in the market clearing price on the Turkish market (USc 4.8/kWh). Notably, Turkish prices decreased further from a significantly low base. The weighted average wholesale price in Georgia was down 4.7% y/y to USc 3.8. 2.5% of total electricity supplied to the grid was traded through the market operator, with the rest traded through bilateral contracts. The average export price of Georgian electricity was USc 5.0/kWh, up 33.4% y/y.

Tamara Kurdadze (Galt and Taggart)