Tourism Market Watch

For Georgia Today by Kakhaber Samkurashvili

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of Energy, Healthcare, Tourism, Agriculture, Wine, and Real Estate sectors in Georgia. As part of our energy sector coverage, we produce a monthly Tourism Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

The accommodation industry in Georgia continued rapid growth in 2016. The number of accommodation units at end-2016 is up 19.7% y/y, with bed capacity up 11.1% y/y to over 57,000. Hotels account for 63.9% of beds, followed by family hotels (16.8%) and guesthouses (13.1%). International branded hotels comprise 11.4% of total room supply in Georgia. The highest concentration of international brands is observed in Tbilisi (22.3% of total room supply) and Adjara (15.7%). The 2017-2019 pipeline of international branded hotels features almost 3,400 additional rooms in Tbilisi and over 1,600 in Batumi. Overall, there are almost 10,000 new hotel rooms, branded and non-branded, in the 2017-2019 pipeline of new accommodation units.

Leading global hotel brands display continued interest in the Georgian market. On December 19, 2016, Hilton announced the signing of a management agreement with Granat LLC for its flagship Hilton Hotels & Resorts brand hotel in Tbilisi. The investment is estimated at US$ 50.0mn, with the 206-room hotel set to open in early 2019. In its press release, Hilton cites “Tbilisi's diverse economy - with substantial international infrastructure investment, a burgeoning events calendar and leisure growth” as the reasons to introduce its flagship brand to the Georgian capital. Hilton is already present on the Georgian market, with Hilton Batumi, while Hilton Garden Inn Tbilisi Chavchavadze is currently under construction and set to open in 2018. On December 14, 2016, Rezidor Hotel Group (RHG) announced plans to open a 100-room Radisson Red in Tbilisi in mid-2019, with LLC Commerce Group as its local partner. Radisson Red is a new hotel concept by RHG, targeting millennials through art, music, and fashion. There are currently only two Radisson Red hotels in the world – in Brussels and Minneapolis.

Adjara Hospitality Group (AHG) continues to introduce innovative concepts on the Georgian hospitality market. The group has announced plans to construct an airport in Stepantsminda, in close proximity to its Rooms Hotel Kazbegi. As of December 2016, the company already operates the first air taxi in Georgia with its 5-seater Beechcraft airplane. AHG also announced plans to expand its presence on the Georgian accommodation market with the introduction of its own new 5-star hotel brand, Aviator, in 2017. The new hotel will be located near Rooms Hotel Tbilisi and Intercontinental Hotel, which is set to open by end-2017. This move follows AHG’s entry in the low-price segment of the accommodation market with its introduction of Fabrika. Fabrika is a Soviet sewing factory converted into a multifunctional cultural space targeting young visitors. It features 49 hotel rooms and a 335-bed hostel, which increased the number of hostel beds in Tbilisi by 26.2%. AHG is also expanding its Rooms Hotel chain with a Rooms Hotel Batumi, set to open in 2017.

International Arrivals to Georgia

The number of international arrivals was up 4.3% y/y to 0.49mn in December 2016. Out of the top five source markets, there was growth from Armenia (+9.5% y/y), Azerbaijan (+3.9% y/y), and Ukraine (+14.0% y/y), while arrivals were down from Russia (-2.3% y/y) and Turkey (-16.7% y/y). Arrivals from the EU were up 28.6% y/y to over 13,400 visitors.

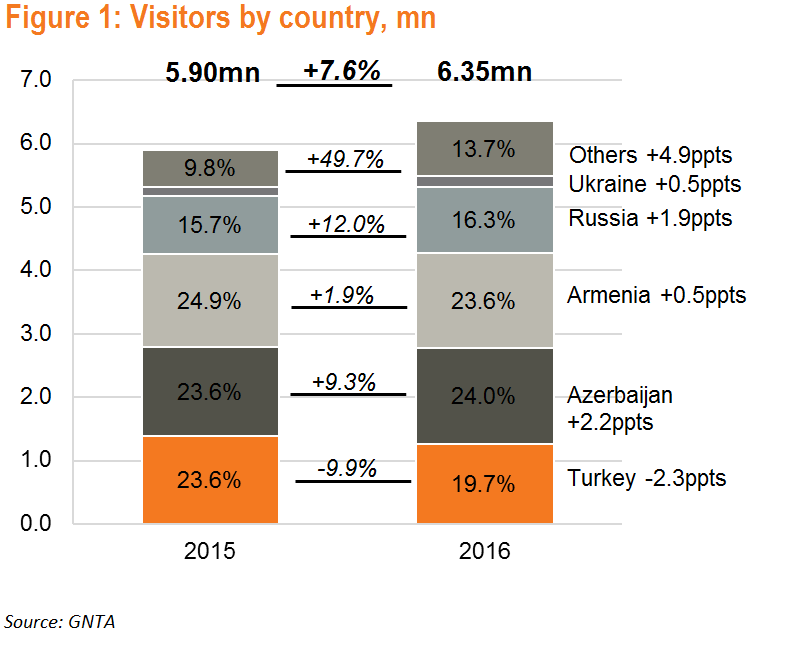

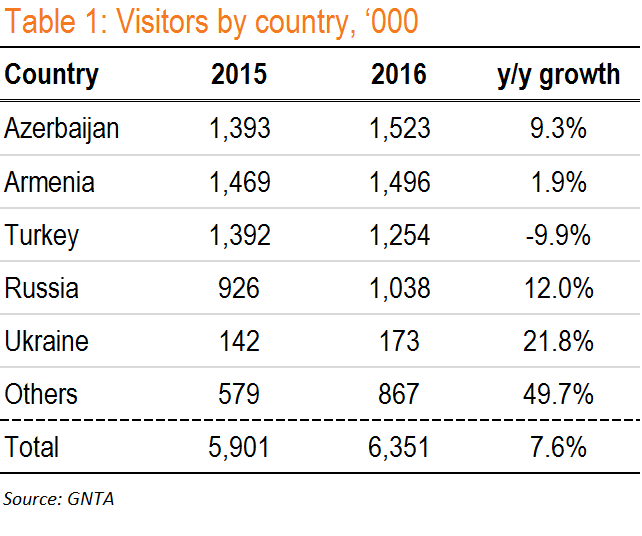

The number of international arrivals was up 7.6% y/y to 6.35mn visitors in 2016. The number of visitors increased from all major countries except for Turkey (-9.9% y/y) in 2016. Russia and Ukraine posted double-digit growth rates, while Azerbaijan (+9.3% y/y) was the single largest contributor to overall growth. Travel inflows were up 11.7% y/y to US$ 1.68bn in 9M16. Based on our estimates, travel inflows will reach approximately US$ 2.1bn in FY16.

While the top four source markets accounted for 83.6% of international arrivals in 2016, secondary source markets also posted robust performances. Ukraine, the 5th largest source market, posted a 21.9% y/y increase in 2016. The number of Iranian visitors is up almost 5.9x to 148,000, while the number of Israeli visitors during the same period is up 1.6x to over 92,000 visitors.

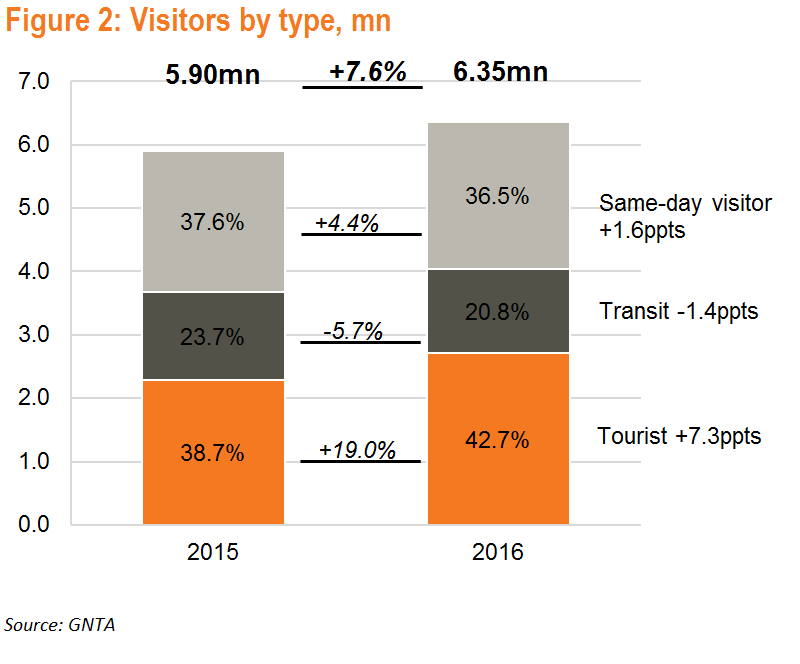

The tourist category continues to drive arrival growth in December 2016. The number of overnight visitors (‘tourist’ category) was up 14.8% y/y and accounted for 36.6% of total international arrivals. Same-day arrivals posted modest growth of 5.1% y/y, while the number of transit visitors declined 15.8% y/y in December 2016. The number of tourist arrivals is up 19.0% y/y to 2.7mn in 2016, compared to 2.3mn in 2015. The number of same-day visitors is up 4.4% y/y, while the number of transit visitors is down 5.7% y/y in 2016.