Electricity Market Watch

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of Energy, Healthcare, Tourism, Agriculture, Wine, and Real Estate sectors in Georgia. As part of our energy sector coverage, we produce a monthly Electricity Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

For Georgia Today by Mariam Chakhvashvili

Georgia Renewable Power Company (GRPC): Significant plans in renewable energy project development

GoG has declared its intent to sign an MoU with JSC Caucasian Wind Company for the feasibility study of wind power plants (WPPs) in Tbilisi, Martkopi, and Tkibuli. The approximate installed capacity of each WPP is 100MW, while the exact capacity and required investment will be known after the completion of the 18-month feasibility study. The company is also planning to develop four additional WPPs. JSC Caucasian Wind Company is an SPV established by GRPC, subsidiary of BGEO Group, for the development of wind power projects in Georgia. GRPC is also pursuing the development of ten solar power plants and several HPPs through various SPVs.

Excluding GRPC’s wind project pipeline, there is approximately 822MW of wind projects under development MoUs, which would generate approximately 3 tWh of electricity. Feasibility studies, to be finalized in the next couple of years, will establish the final number of projects to advance to the construction and operation phase, with adjusted installed capacity and generation figures.

Enguri HPP temporarily halts operations to prepare for rehabilitation works in 2018

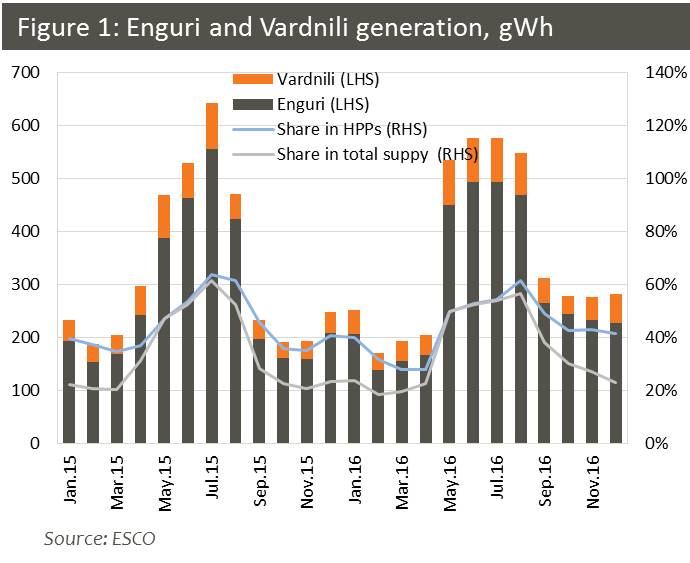

Enguri is the largest HPP in Georgia, owned by Enguri Ltd, a state-owned company. The Enguri dam is the sixth largest dam in the world and included on the list of national cultural heritage. A series of renovations were completed on the Enguri HPP from 2006, specifically on the dam and electro-mechanical equipment. The fourth phase of rehabilitation, which mainly includes works on the 15km tunnel through the Enguri dam to the power house, is scheduled for 2018 and will require approximately EUR 33mn. An EBRD loan, along with EU NIF funding, will be used to finance the completion of the Enguri HPP renovation program. The first part of the project envisages the selection of a consultancy, which will deliver the final design and timeline of the renovation works. The tender procedure for the selection of a consultancy is expected to commence by the end of March 2017. In order to give consultants the opportunity to evaluate future works and submit competent bids, Enguri HPP halted operations for several days starting February 19th, allowing experts to walk through the tunnel.

Enguri HPP, together with Vardnili HPP, which mainly uses the water flowing from Enguri, satisfies approximately 35% of total annual electricity demand (22% excluding the Abkhazian region). On average, 46% of electricity generated from Enguri and Vardnili is used to satisfy the consumption of the Abkhazian region, while the rest is used to meet domestic consumption needs and/or exported. When Enguri is temporarily shut down, daily demand is satisfied through electricity imports from Azerbaijan, Armenia, and Russia (for the Abkhazian region).

Electricity Consumption and Generation – January 2017

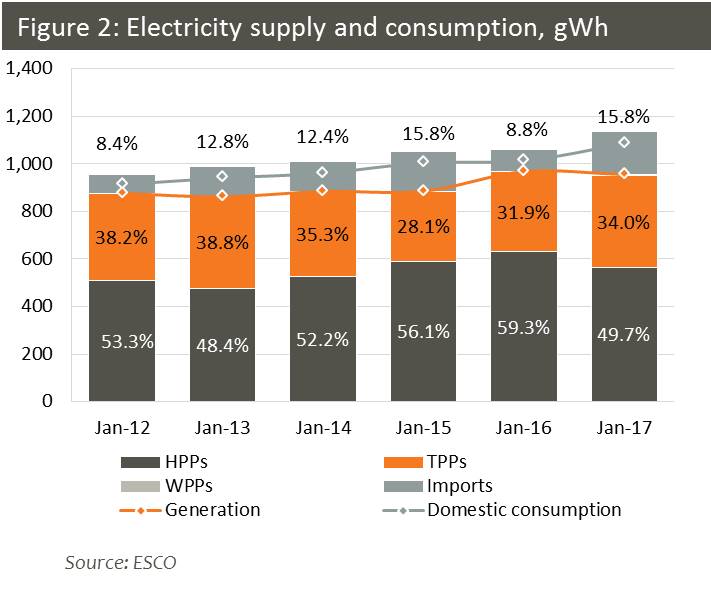

Domestic consumption increased 7.2% y/y in January 2017, with Telasi (+10.5% y/y) and eligible consumers (+17.9% y/y) driving the growth. DSO consumption increased 5.8% y/y: consumption was up 2.7% y/y by Energo-Pro, 7.7% y/y by Kakheti Energy Distribution, and 10.5% y/y by Telasi, which has posted 20%+ annual growth rates for the past five months. Consumption of the Abkhazian region was up 6.9% y/y and accounted for 94.8% of the electricity generated by Enguri and Vardnili. Consumption by eligible consumers was up significantly (+17.9% y/y), albeit from a low base in January 2016 (-24.7% y/y). The largest eligible consumer, Georgian Manganese (78.5% of direct consumption), posted 24.9% y/y growth, also from last year’s low base (-28.3% y/y), and contributed quite significantly to energy demand growth in January 2017 (1.7 percentage points). Electricity exports were negligible, while electricity transit from Azerbaijan to Turkey amounted to 9.7gWh in January 2017.

Domestic consumption needs in January 2017 were met in roughly equal parts by hydro generation (49.7%), on the one hand, and thermal (34.0%) and imported (15.8%) electricity, on the other. The newly built wind power plant accounted for 0.6% of total electricity supply. Total electricity supply from domestic sources was down 1.3% y/y. Hydro generation decreased 10.4% y/y, mainly due to low generation of regulated power plants (-29.3% y/y), excluding Enguri and Vardnili, whose combined production was up 5.6% y/y. The drop in hydro generation was compensated by thermal power (+13.8% y/y) and imports. The amount of imported electricity almost doubled (+92.3% y/y), but from a very low base in January 2016 (-43.9% y/y), and increased only 7.8% compared to January 2015. Most of the imported electricity came from Azerbaijan (96.3%), with the rest (3.7%) imported from Russia, via the Salkhino line, at the beginning of January 2017 to supply the Abkhazian region in island mode. Guaranteed capacity fee was down 21.9% y/y to USc 0.66/kWh. Guaranteed capacity was provided by each of the five guaranteed capacity sources for most of the month. Mtkvari Energy and Gardabani CCGT operated at full power for the entire month, while Blocks 3 and 4 and GPower were mainly providing reserve for the system.

Wholesale electricity prices in January 2017

Wholesale market prices in Georgia decreased 7.5% y/y to USc 5.1/kWh, just 0.4% above the Turkish market clearing price in January 2017. Turkish electricity prices decreased 3.0% y/y to USc 5.0/kWh from a very low base in January 2016 (-32.5% y/y). 27.8% of total electricity supplied to the grid in January 2017 was traded through the market operator, with the rest traded through bilateral contracts.