Electricity Market Watch

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of Energy, Healthcare, Tourism, Agriculture, Wine, and Real Estate sectors in Georgia. As part of our energy sector coverage, we produce a monthly Electricity Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

Georgian gov’t decides to sell the newly commissioned wind power plant to private investors

The wind farm is currently owned by “Qartli Wind Farm” Ltd, whose shareholders are state-owned companies Georgian Energy Development Fund (GEDF) and Georgian Oil and Gas Corporation (GOGC). Shares of the Qartli wind farm will be sold via public auction, after an evaluation by an independent audit company. The terms of the auction will be announced after the final audit report is issued. The WPP has supplied on average 0.5% of monthly electricity demand since it commenced operations in November 2016.

EU4ENERGY regional office opened in Tbilisi on March 10, 2017

EU4Energy is a four-year European Union technical assistance project launched in June 2016. The overall objective of the 3rd component of EU4ENERGY, with a budget of EUR 6.8mn, is to improve the beneficiary countries' legislative and regulatory environment in the energy sector, in line with their EU obligations and best practices. For Moldova, Ukraine, and Georgia, the focus is on improving the energy legislative and regulatory framework and implementing policy recommendations, in line with the Energy Community Treaty / Association Agreements / DCFTA requirements. For other beneficiary countries (Belarus, Armenia, Azerbaijan), the focus is on EU best practices in selected areas. The regional office in Tbilisi will coordinate the EU4ENERGY project’s activities aimed at improving the legislative and regulatory framework of the energy markets in Armenia, Azerbaijan, and Georgia. A second regional office covering Belarus, Moldova, and Ukraine will operate in Kyiv. The current governance project is part of the wider EU4ENERGY EUR 21mn initiative, which also includes Central Asian countries and is comprised of five components.

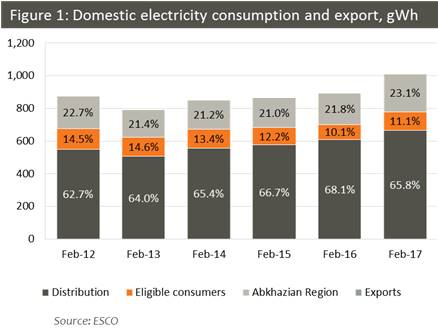

Domestic consumption increased 13.0% y/y in February 2017

Domestic consumption increased 13.0% y/y in February 2017, with the Abkhazian region and eligible consumers driving the growth. Consumption of distribution companies increased 9.1% y/y: consumption was up 8.3% y/y by Telasi, 4.9% y/y by Kakheti Energy Distribution, and 10.0% y/y by Energo- Pro. Consumption of the Abkhazian region was up 19.9% y/y and accounted for 23.1% of domestic consumption. Consumption by eligible consumers was up significantly (+24.8% y/y), albeit from a very low base in February 2016. The largest eligible consumer, Georgian Manganese (81.1% of direct consumption), posted 33.1% y/y growth, also from last year’s low base, and contributed significantly to the overall growth in energy demand in February 2017. Electricity exports were negligible, while electricity transit from Azerbaijan to Turkey amounted to 16.3 GWh in February 2017.

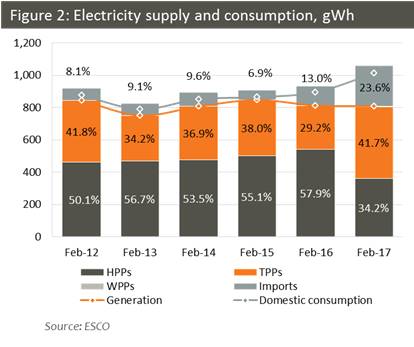

Growth in domestic consumption met mostly through imported electricity

Total electricity supply from domestic sources was flat (-0.5% y/y), while imports more than doubled (+106.2% y/y) in February 2017. Only one third (34.2%) of domestic consumption needs was met by hydro generation; the rest was satisfied by thermal (41.7%) and imported (23.6%) electricity, while the newly built wind power plant accounted for 0.5% of total electricity supply.

The main reasons for the change in the electricity supply mix were bad hydrological conditions affecting most HPPs, and Enguri HPP’s 10-day closure. The HPP halted operations to allow experts interested in the Enguri tunnel rehabilitation consultancy tender to walk through the tunnel and evaluate the scope of work. Total hydro generation decreased 33.1% y/y, with generation down 39.5% y/y by Enguri/Vardnili, 35.8% y/y by other regulated HPPs, and 11.9% y/y by deregulated HPPs.

The drop in hydro generation was compensated by TPPs (+62.2% y/y) and imports (+106.2% y/y). Most of the TPPs operated at full power for the entire month, while GPower and one of Tbilsresi blocks mainly provided reserve for the system.

Almost half of the imported electricity came from Azerbaijan (47.3%), with the rest imported from Russia (42.6%) and Armenia (10.2%). The rationale for this diversification of import sources was to ensure security of supply while the Enguri HPP was halted. 44.5% of the Abkhazian region’s consumption was satisfied by Enguri / Vardnili generation, while the rest was met through other sources, including imports from Russia via the Salkhino line.

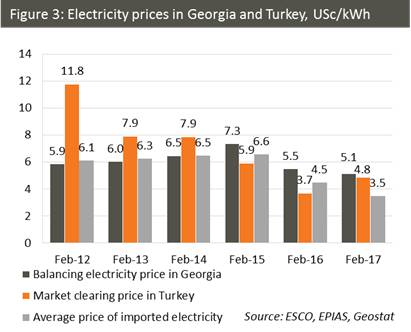

Electricity Prices in Georgia and Turkey

Wholesale market prices in Georgia decreased 7.0% y/y to USc 5.1/kWh, 5.7% above the Turkish market clearing price in February 2017. Turkish electricity prices increased 30.8% y/y to USc 4.8/kWh from a significantly low base in February 2016. 31.8% of total electricity supplied to the grid in February 2017 was traded through the market operator, with the rest traded through bilateral contracts.

The average price of imported electricity in Georgia decreased 22.6% y/y, notably from the very low base in February 2016. The main reason for such a meaningful decrease was the subsidized price of imported electricity from Russia (via the Salkhino line), which was mainly directed to the Abkhazian region to meet its continuously increasing demand.

Mariam Chakhvashvili for Georgia Today