Electricity Market Watch

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of Energy, Healthcare, Tourism, Agriculture, Wine, and Real Estate sectors in Georgia. As part of our energy sector coverage, we produce a monthly Electricity Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

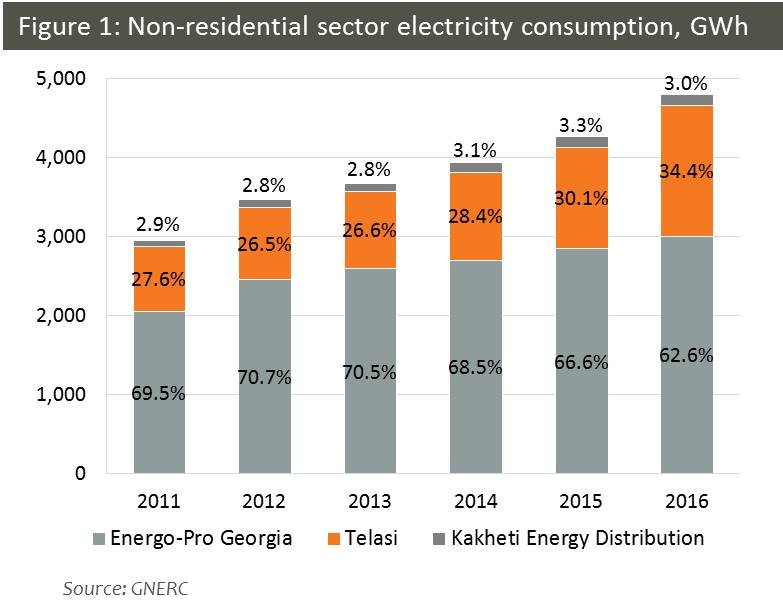

Non-residential sector leads electricity consumption growth in 2016

Electricity consumption by the residential sector, which accounted for one-third of the electricity supplied by distribution companies, was down 1.6% y/y in 2016. The rest was consumed by non-residential subscribers, whose usage was up 12.5% y/y in 2016 and contributed 5.2 percentage points to the overall 6.2% increase in Georgia’s electricity consumption.The key drivers of growth were new commercial entities added to the distribution grid. Telasi posted the largest increase (+28.7% y/y) in the non-residential sector, followed by Energo-Pro Georgia (+5.7% y/y) and Kakheti Energy Distribution (+2.9% y/y). Commercial users have the right to purchase electricity via bilateral agreements, but most of them prefer to go through the distribution companies, largely because of existing price regulations.

Net metering initiative gains followers

Eight users across various regions in Georgia (0.15MW total capacity) have taken advantage of the net metering mechanism, introduced in the legislation last year. Based on changes in legislation, energy consumers are allowed to install micro power plants (less than 0.1MW of installed capacity) that use renewable energy sources (mainly solar panels) to meet their own energy needs and supply surplus energy to the DSOs (Telasi, Energo-Pro, or Kakheti Distribution). The amount of energy consumed and supplied will be netted on an annual basis for settlement with the DSO. According to a recent initiative, revenues generated by supply of electricity from micro power plants will not be subject to taxation. Successful implementation of the initiative should support development of the sector.

TPPs consumed less natural gas in 2016

Natural gas consumed by TPPs was down 19.5% y/y in 2016, while electricity generated by TPPs decreased by only 6.0% y/y. Commissioning of the more efficient Gardabani combined cycle power plant at the end of 2015 was the main driver of this improvement. Gardabani CCGT accounted for half of TPP-generated electricity in 2016, partially substituting for the less efficient Mtkvari TPP and Tbilsresi blocks, which operated at full capacity in previous years.

Electricity Consumption and Generation – March 2017

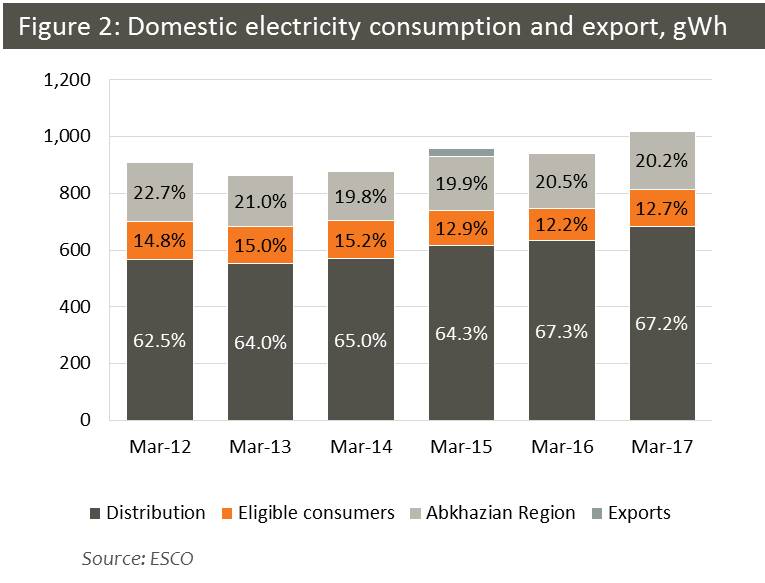

Domestic consumption increased 8.4% y/y in March 2017, with distribution companies driving the growth. Consumption of distribution companies increased 8.2% y/y: consumption was up 7.7% y/y by Telasi, 8.5% y/y by Energo-Pro, and 7.3% y/y by Kakheti Energy Distribution. The Abkhazian region’s electricity usage was up 6.8% y/y, while consumption by eligible consumers was up 12.4% y/y. Electricity exports were negligible. Electricity transit from Azerbaijan to Turkey amounted to 4.0 GWh in March 2017, down 84.1% y/y. The large reduction in transit was largely the result of lower transit capacity due to the high level of electricity imports.

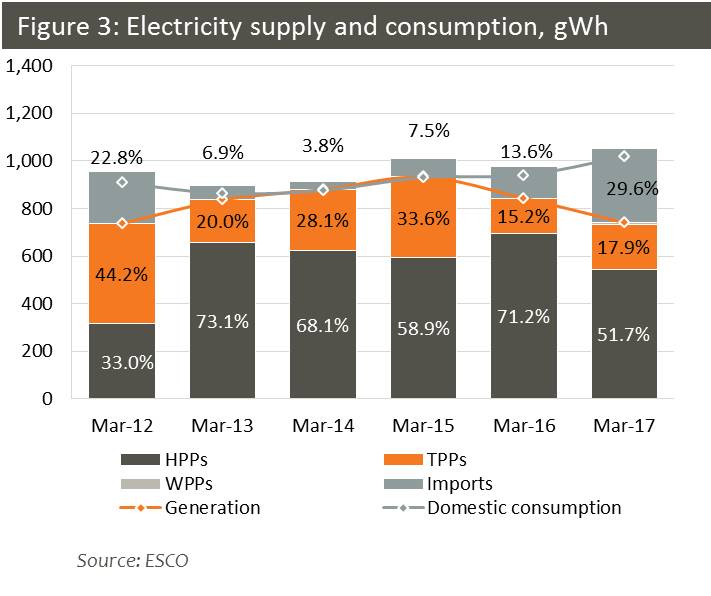

Total electricity supply from domestic sources was down 12.2% y/y, while imports more than doubled (+133.6% y/y) in March 2017. Only half (51.7%) of domestic consumption needs was met by hydro generation; the rest was satisfied by thermal (17.9%) and imported (29.6%) electricity, while the newly built wind power plant accounted for 0.8% of total electricity supply.

Unfavorable hydrological conditions negatively affected hydro generation

The main reasons for the change in the electricity supply mix were bad hydrological conditions affecting most HPPs and a decreased water level in the Enguri dam due to the HPP’s 10-day closure in February. Total hydro generation decreased 21.7% y/y, with generation down 34.6% y/y by Enguri/Vardnili and 21.6% y/y by other regulated HPPs. Despite bad hydrological conditions, deregulated HPP generation was flat (+0.4% y/y), mainly due to the addition of Dariali HPP (108.0MW), Khelvachauri HPP (47.5 MW), and other new HPPs (9.4MW) to this group at the end of 2016.

The drop in hydro generation was partially compensated by TPPs, which posted a significant increase (+26.5% y/y), albeit from a very low base in March 2016 (-56.2% y/y). Only one TPP, the Gardabani CCGT, operated at full power for the entire month, while other TPPs mainly provided reserve for the system. The guaranteed capacity fee was down 59.0% y/y to USc 0.34/kWh, with guaranteed capacity provided by each of the five sources for the entire month.

Electricity imports at a historical high

The share of electricity imports in total electricity supply was at a historical high of 29.6% in March 2017. More than half of the imported electricity came from Azerbaijan (56.8%), with the rest imported from Russia (27.0%) and Armenia (16.2%). 61.6% of the Abkhazian region’s consumption was satisfied by Enguri/Vardnili generation, while the rest was met through imports from Russia via the Salkhino line.

Electricity Prices in Georgia

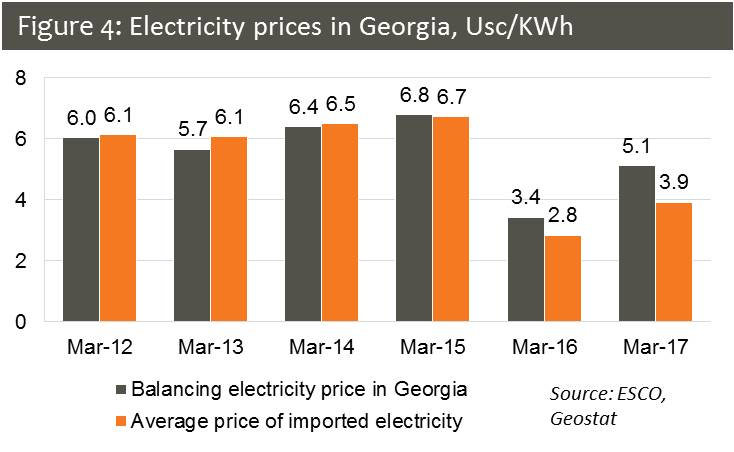

The average price of imported electricity in Georgia was USc 3.9/kWh, up 38.0% y/y from the fully subsidized price of USc 2.8/kWh in March 2016 (-57.7% y/y). The main reason for such low prices in the last two years was the subsidized price of electricity imported from Russia (via the Salkhino line) to meet the Abkhazian region’s continuously increasing demand.

Wholesale market prices in Georgia increased 48.5% y/y to USc 5.1/kWh33.8% of total electricity supplied to the grid in March 2017 was traded through the market operator, with the rest traded through bilateral contracts. The increases in the price and share of balancing electricity were due to the high level of imports in March 2017.

By Mariam Chakhvashvili