Tourism Market Watch: APRIL

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of Energy, Healthcare, Tourism, Agriculture, Wine, and Real Estate sectors in Georgia. As part of our tourism sector coverage, we produce a monthly Tourism Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

By Kakhaber Samkurashvili

Completion of international branded hotels in Georgia is behind schedule

Expected completion dates for 11 of the 26 international branded hotels in our 2016-2018 pipeline (see our June 2016 tourism report, Shifting into High Gear) have been pushed back by a year. That represents 36.7% of the hotel rooms included in the aforementioned pipeline. The delays vary significantly across regions. For Tbilisi, only two of 14 hotels have been postponed, whereas four of the six in Batumi and five of the six in other regions have been officially delayed by a year. The delays can be largely attributed to regional instability in 2016, along with the currency fluctuation and election year in Georgia. Even so, the international branded hotel stock is expected to increase by 1,203 rooms (+69.9%) in Tbilisi and 224 rooms (+24.1%) in Batumi by the end of 2017. With new hotel projects announced since June 2016, there are now a total of 19 international hotels in the pipeline for Tbilisi, nine in Batumi, and nine in other regions.

The hotel pipeline in Georgian regions outside of Tbilisi and Batumi remains strong, with the Kakheti region attracting a lot of interest

Adjara Group Hospitality has announced plans to enter the Kakheti market with a 40-room farm hotel concept in Sagarejo. A 100-room Golden Tulip in Telavi is expected to be completed by end-2017 and a 120-room Radisson Blu in Tsinandali by end-2018. The Partnership Fund signed a partnership agreement with Lopota Resorts and will invest US$ 5.4mn in the expansion of the resort, which will include the addition of 85 hotel rooms and a 300-person conference room, along with other amenities to the complex.

Two international midscale brands entered the Georgian market in 2017

Maqro construction unveiled its second international midscale brand, Ibis Styles, in Tbilisi, after introducing Mercure Tbilisi Old Town in 2015. The 3-star Ibis Styles opened its doors in April and features 118 rooms. Another international midscale brand, Wyndham Hotel, opened in Batumi in February, adding 146 rooms to the stock of branded hotel rooms. Rooms Hotel and Best Western VIB are also expected to open in Batumi in 2017.

The share of visitors arriving by air to Georgia is increasing

19.1% of international arrivals came in through the Georgian airports in January-April 2017, compared to 13.3% during the same period in 2016. The main driver was Tbilisi airport, with the number of international arrivals up 61.0% y/y to 295,000, while the Kutaisi airport has recorded almost 28,000 international visitors (+62.7% y/y) since the beginning of the 2017. The growing share of air arrivals goes hand in hand with the diversification of direct flight routes out of Georgian airports. Georgia’s air connectivity with the Middle East is improving, with a Jordanian low-cost airline, Air Arabia Jordan, now operating flights between Tbilisi and Amman. Connectivity with Russia is expected to increase further, as several Russian carriers have announced plans to expand their offering during the summer season.

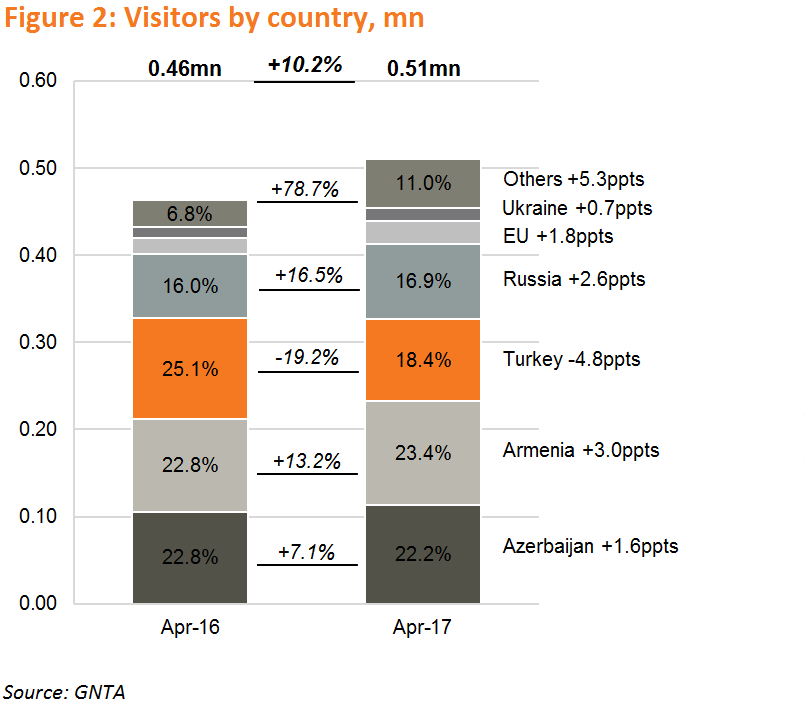

The number of international arrivals was up 10.2% y/y to 0.51mn in April 2017

Of the top five source markets, there was strong growth from Armenia (+13.2% y/y), Azerbaijan (+7.1% y/y), Russia (+16.5% y/y), and Ukraine (+27.2% y/y). The number of arrivals from Turkey continues to exhibit a downward trend (-19.2% y/y), as border delays persist in Sarpi.Arrivals from the EU were up 44.8% y/y to over 26,000 visitors.

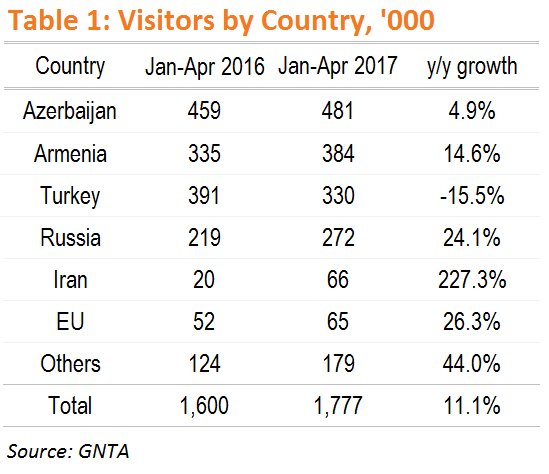

The number of international arrivals was up 11.1% y/y to 1.78mn visitors in January-April 2017

The number of visitors increased from all major source countries except for Turkey (-15.5% y/y). Armenia (+14.6% y/y) and Russia (+24.1% y/y) were the largest contributors to overall growth, with Ukraine also posting double-digit growth (+20.2% y/y). The number of visitors from Azerbaijan posted a modest increase of 4.9% y/y, but from the high base of January-April of 2016 (+22.9% y/y).

While the top four source markets accounted for 82.6% of international arrivals since the beginning of 2017, secondary source markets also posted robust performances

The number of Iranian visitors was up 3.3x to 66,000visitors in first four months of 2017, mainly dueto aninflow from Iran during Novruz Bairam.The number of Indian visitors was up 139.8% y/y to over 16,000, while the number of Israeli visitors increased 66.8% y/y to almost 19,000 visitors. Arrivals from the EU were up 26.3% y/y to over 65,000 visitors in January-April of 2017, with Germany (+43.2% y/y), Poland (+29.8% y/y), and United Kingdom (+26.0% y/y) driving the growth.

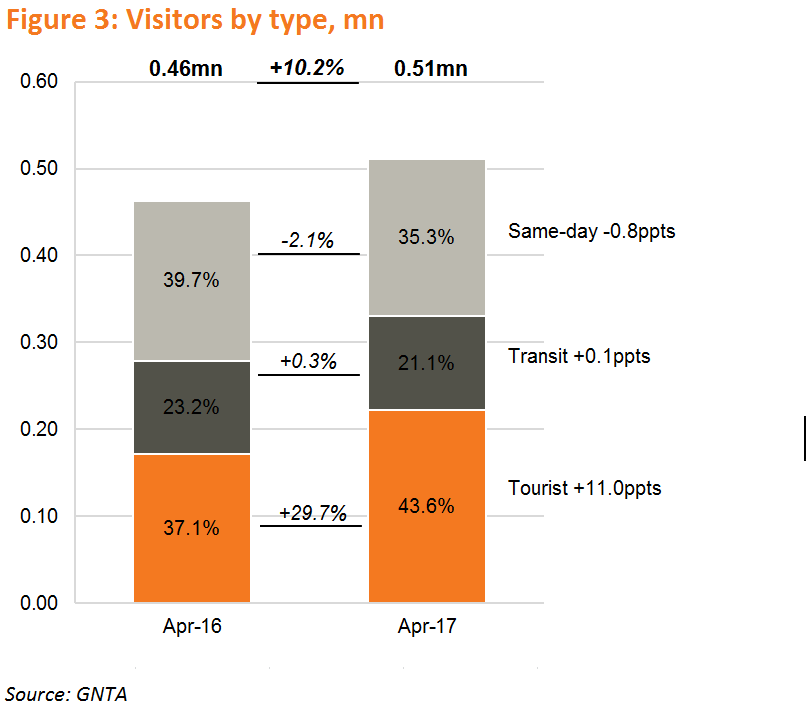

The tourist category continued to drive arrival growth in April 2017

The number of overnight visitors (‘tourist’ category) was up 29.7% y/y and accounted for 43.6% of international arrivals. Same-day arrivals were down 2.1% y/y, while the number of transit visitors was flat. The number of tourist arrivals is up 26.9% y/y to 0.74mn in January-April of 2017, while the number of same-day visitors is down 1.8% y/y and the number of transit visitors up 11.3% y/y.