Electricity Market Watch: MAY

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of Energy, Healthcare, Tourism, Agriculture, Wine, and Real Estate sectors in Georgia. As part of our energy sector coverage, we produce a monthly Electricity Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

For Georgia Today by Mariam Chakhvashvili

Electricity deficit in 2017 bridged by imports rather than TPPs

Electricity imports in 4M17 have already exceeded 2016 total imports by 85.1% and 2017 planned imports by 7.6%. 886.7 GWh of electricity (+138.2% y/y) was imported in 4M17, with Azerbaijan being the main source of imports (62.7% of total) and the rest coming from Russia (24.2%) and Armenia (13.1%). Electricity imports accounted for 21.1% of total electricity supply in 4M17. Imported electricity was directed at satisfying higher consumption (+9.1% y/y) and filling the gap created by a drop in hydro generation (-15.6% y/y). Relative prices of TPP-generated electricity and imports were the main reason behind choosing imports over TPPs to satisfy high demand (5.3% higher than planned) and make up for low HPP generation (11.0% lower than planned). The price of TPP-generated electricity in 2017 has ranged from USc 3.7/kWh to USc 5.9/kWh, while the average import price in 4M17 was USc 4.1/kWh. The decrease in the average import price was a one-off event, caused by subsidized imports from Russia (via the Salkhino line), negotiated mainly to meet the increased demand of the Abkhazian region during and after Enguri HPP’s temporary closure. Imports from Armenia were also on negotiated terms.

Updated annual forecast for 2017

Electricity consumption is expected to increase 7.7% y/y, according to the updated annual forecast for 2017 issued on April 7. The annual forecast, prepared by GSE and approved by Ministry of Energy, outlines the generation and consumption plans for each market participant. Main modifications include the addition of the WPP and HPPs, which were commissioned after the preparation of the last annual forecast on November 28, 2016; changes in import and export amounts and directions; and an update of the first three months’ forecast with actual figures. According to the modified annual forecast, imports will account for 12.9% of planned supply of electricity in 2017, with an additional 763.1 GWh of imports expected from Azerbaijan (83.1%) and Armenia (16.9%) over the remainder of the year.

Export markets

Price volatility on the Turkish market led to a reduction in the number of companies willing to export from Georgia to Turkey, leaving unallocated capacity of 4MW out of the 250MW allowed export capacity (ATC) in May 2017. Private companies with priority access to the Meskheti transmission line connecting Georgia and Turkey will be the main exporters to Turkey in 2017. For the second consecutive year, Georgian Urban Energy (owner of Paravani HPP), which has priority access to the Meskheti line, has chosen to export to Turkey only May through July, in order secure its income at an average of USc 4.5/kWh and contribute to filling the country’s deficit in winter months. Armenia has also become an attractive market for Georgian companies. Among the exporters to Armenia, besides the privately owned GIEC, is ESCO. In exchange for the imported electricity during 4M17 (116.3GWh), ESCO is exporting electricity to Armenia in May and June. The practice of repaying the import bill with exports is also used for repaying 2012 imports from Azerbaijan with exports to Turkey in 2016 and 2017.

IMF restricts power purchase agreements

IMF has declared PPAs for power plants as a fiscal risk for Georgia in its country report issued in April 2017. IMF recommends refraining from initiating any PPAs until the institutional framework is in place. Taking into consideration the existing fall-winter period power deficit, partial PPAs currently under negotiation, with cumulative installed capacity of up to 500MW, are permitted to proceed, as long as the guaranteed purchase period is limited to eight months and the purchase price to USc 6.0/kWh. Exceptions might be made for two specific projects, Namakhvani HPP cascade and Koromkheti HPP, subject to a detailed fiscal risk assessment and evaluation.

Electricity Consumption and Generation – April 2017

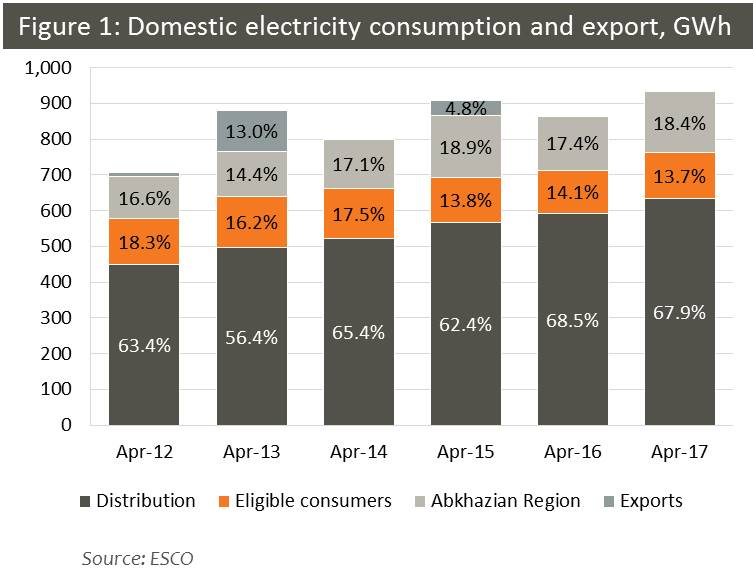

Domestic consumption increased 7.9% y/y in April 2017 and 9.1% y/y in 4M17. Consumption of distribution companies increased 7.1% y/y in April, while the Abkhazian region’s electricity usage was up 13.7% y/y and consumption by eligible consumers was up 5.0% y/y. Electricity exports were negligible. Electricity transit from Azerbaijan to Turkey amounted to 4.7 GWh in April 2017, down 90.1% y/y and 34.7 GWh in 4M17, down 66.8% y/y. The large reduction in transit was largely the result of lower transit capacity due to the high level of electricity imports.

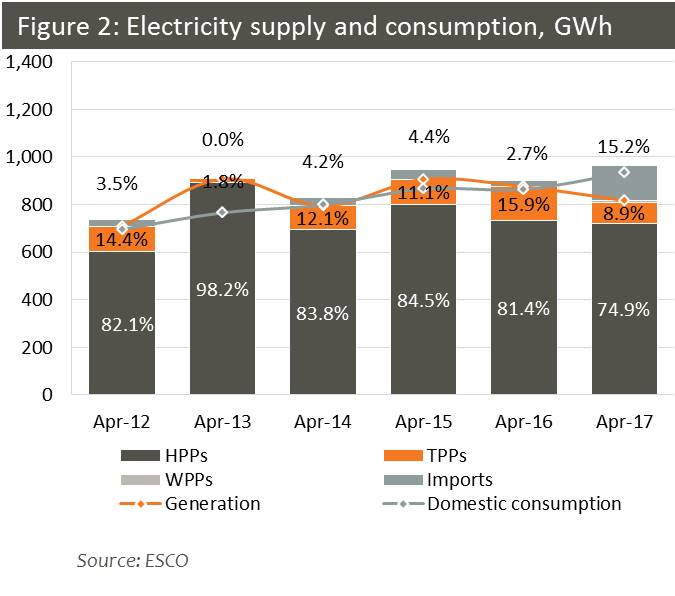

Growth in domestic consumption was met mostly through imported electricity. Total electricity supply from domestic sources was down 6.6% y/y, while imports increased almost six-fold. Three quarters (74.9%) of domestic consumption needs were met by hydro generation; the rest was satisfied by thermal (8.9%) and imported (15.2%) electricity, while the newly built wind power plant accounted for 1.0% of total electricity supply.

New HPPs help maintain hydro generation levels

The main reasons for the change in the electricity supply mix were bad hydrological conditions affecting most HPPs. Total hydro generation was down only 1.3% y/y. Generation was down 13.8% y/y by Enguri/Vardnili and 4.0% y/y by other regulated HPPs, while deregulated HPP generation posted an increase of 24.5% y/y, mainly due to the addition of Dariali HPP (108.0MW), Khelvachauri HPP (47.5 MW), and other new HPPs (9.4MW) to this group at the end of 2016.

The decrease in domestic supply was mainly the result of lower TPP generation (-40.1% y/y). Only one TPP, the Gardabani CCGT, operated at full power for half of the month, while other TPPs mainly provided reserve for the system. The guaranteed capacity fee was down 13.4% y/y to USc 0.8/kWh, with guaranteed capacity provided by each of the five sources for the entire month.

Imports at an all-time high for the month of April

The share of electricity imports in total electricity supply was 15.2%, a historical high for the month of April. More than half of the imported electricity came from Azerbaijan (60.2%), with the rest imported from Russia (12.2%) and Armenia (27.6%). 10.4% of the Abkhazian region’s consumption was satisfied by imports from Russia via the Salkhino line, while the rest was met through Enguri/Vardnili generation.

Electricity Prices in Georgia and Turkey

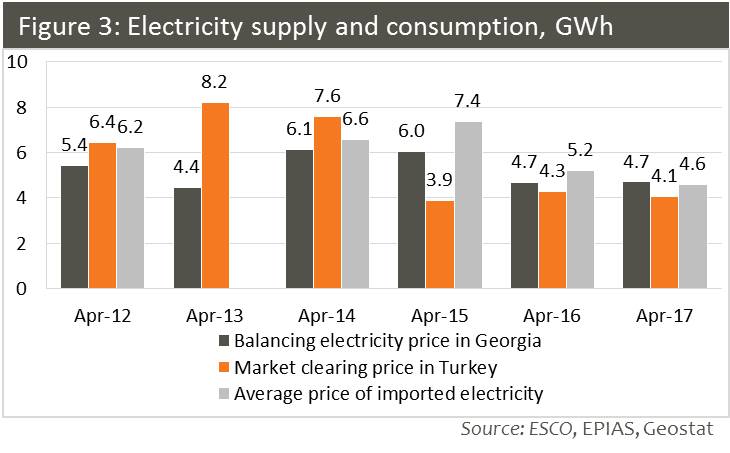

Wholesale market prices in Georgia were 16.0% above the Turkish market clearing price in April 2017. Turkish electricity prices increased 22.2% y/y in local currency, but due to Lira depreciation (-22.4% y/y), prices in US$ terms decreased 5.2% y/y to USc 4.1/kWh.

The average price of imported electricity in Georgia was USc 4.6/kWh, down 11.6% y/y from the already low base in April 2016. The high share of subsidized imports from Russia via the Salkhino line has been the main reason for the lower average import prices in 2017.

Change in purchase price methodology for deregulated HPPs

The wholesale electricity price in Georgia in April 2017 was flat at USc 4.7/kWh (+0.7% y/y), mainly due to the low import price and a change in the balancing electricity purchase price methodology. Starting April 1, the price paid by the market operator (ESCO) to deregulated HPPs for balancing energy supply was lowered from the highest regulated TPP price (14.234 tetri/kWh) to the highest regulated HPP price (9.4 tetri/kWh). In April 2017 the share of such electricity in total balancing energy market was 9.1%, while imports were the leading component (52.3%). Overall, electricity traded through the market operator in April 2017 reached 280.0 GWh, 29.1% of total electricity supplied to the grid, with the rest traded through bilateral contracts.