Tourism Market Watch: JUNE

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of Energy, Healthcare, Tourism, Agriculture, Wine, and Real Estate sectors in Georgia. As part of our tourism sector coverage, we produce a monthly Tourism Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

For Georgia Today by Kakhaber Samkurashvili

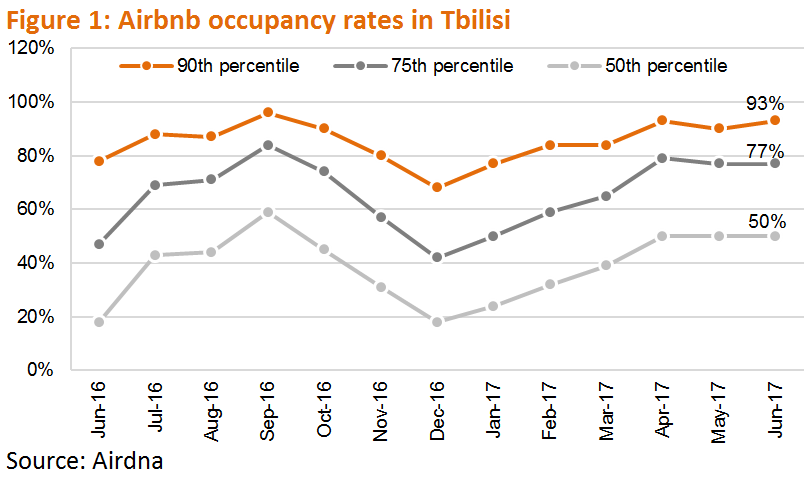

Airbnb’s presence in Tbilisi grows at an astounding pace

7,000 this year. Almost 4,300 active hosts are now offering a wide array of accommodation options. The most prevalent are one and two-bedroom apartments, which together account for over 60% of listings in Tbilisi. Notably, there are almost 1,000 active hosts who provide two or more listings, with as many as 100 hosts offering five or more. It is safe to say that buying apartments in Tbilisi with the aim of securing rental income via Airbnb has become a niche business model.

Airbnb apartment rentals filling the gap in the budget/economy accommodation segment in Tbilisi

This is in line with how Airbnb currently fits in the global accommodation landscape. Only about 10% of its worldwide bookings are for business travel, so the largest impact is felt in the leisure segment, where budget/economy accommodation is dominant. Based on our estimates, there are approximately 3,500-4,000 hotel rooms in the budget/economy segment in Tbilisi. We consider entire home listings ranging from studio size to 3-bedroom apartments on Airbnb, which currently add up to almost 4,700 listings, to be competing directly with this segment. Despite the strong growth in supply, occupancy rates for Airbnb rentals in Tbilisi have been on the rise. The 50th percentile of listings in June 2017 was at 50% occupancy (+32ppts y/y), while the top 10% of properties enjoyed occupancy rates of 93% and higher (+15ppts y/y). Average nightly rates in June 2017 for one and two bedrooms ranged between US$ 19 and US$ 25, while RevPAR for all available listings in Tbilisi was at US$ 23 for the month of June, up 30.6% y/y. Based on our estimates, the 50th percentile, in terms of occupancy and RevPAR, of Airbnb listings is largely in line with the performance of budget/economy hotels in Tbilisi.

International upscale hotels in Tbilisi nearly booked to capacity for summer, despite high prices compared to peers

Based on booking.com data, the highest prices in the international upscale segment in Tbilisi are commanded by Radisson Blu Iveria and Biltmore, averaging GEL 637 to GEL 775 over July and August, while Hualing Hotels & Preference and Tbilisi Marriott average between GEL 479 and GEL 574. Notably, Ambassadori Hotel Tbilisi, a local 5-star hotel, commands one of the highest rates of any hotel in Tbilisi (GEL 624-773 over Jul-Aug). In the international midscale segment, prices average GEL 271 to GEL 501, with Holiday Inn Tbilisi and Courtyard Marriott having the highest rates. Rates at international hotels in Tbilisi are significantly higher than at comparable hotels in peer countries. For example, average nightly rates for Radisson Blu in Tbilisi are 67.6% higher in July and 79.1% higher in August than at comparable Radisson Blu hotels in Eastern European and CIS countries. Such differences in prices point to a scarcity of branded hotels in Tbilisi, which we expect will be remedied once the extensive pipeline begins to materialize, pushing prices down closer to peer averages.

Georgia ranked 70thof 136 countries in Travel & Tourism Competitiveness Index (TTCI) 2017, published biennially by the World Economic Forum (WEF)

In the previous edition, Georgia ranked 71st among 143 countries. The TTCI assesses four key areas: Enabling Environment, T&T Policy and Enabling Conditions, Infrastructure, and Natural and Cultural Resources.The most notable improvement compared to the 2015 edition was moving up 10 positions in Business Environment, which was mainly driven by improved property rights and efficiency of legal framework. While the country ranks extremely highly on Ease of Hiring Foreign Labor, skilled local labor remains a challenge, as indicated by the lowest rankings in Extent of Staff Training, Degree of Customer Orientation, and Ease of Finding Skilled Employees. Lastly, the report highlights the urgent need for further development of tourist service and air transport infrastructure in Georgia.

Number of international arrivals up 28.5% y/y to 0.67mn in June 2017

Of the top four source markets, there was strong growth from Armenia (+28.8% y/y), Azerbaijan (+16.6% y/y), and Russia (+45.0% y/y). The downward trend persists in the number of arrivals from Turkey (-6.4% y/y), but the decline was a modest one, compared to the previous three months.Arrivals from the EU were up 27.0% y/y to nearly 35,000 visitors.

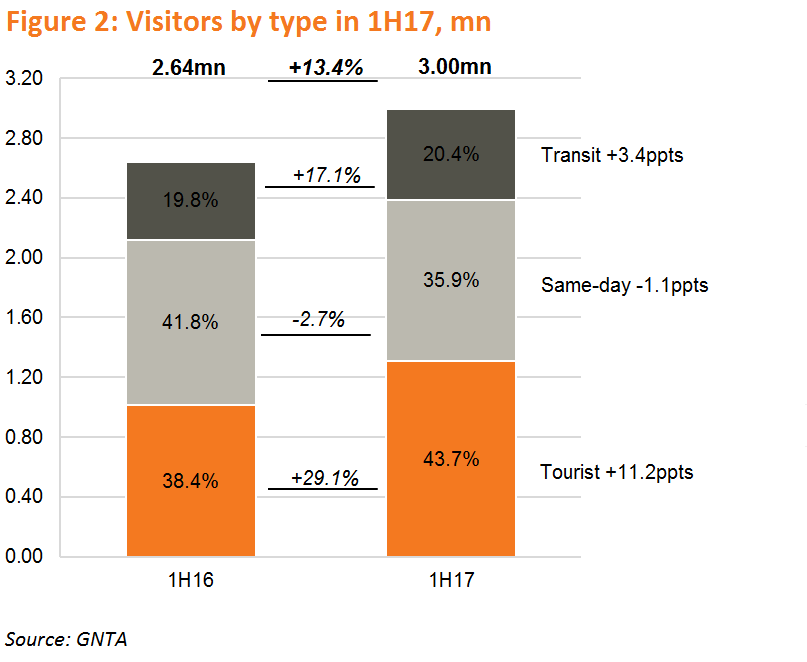

Number of international arrivals up 13.4% y/y to 3.00mn visitors in first half of 2017

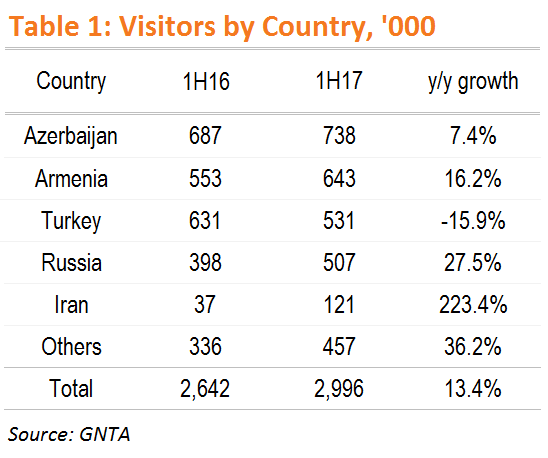

The number of visitors increased from all major source countries except for Turkey (-15.9% y/y). The largest individual contributors to overall growth were Armenia (+16.2% y/y, +3.4ppts) and Russia (+27.5% y/y, +4.1ppts). Azerbaijan contributed 1.9 percentage points, as the number of visitors from Azerbaijan posted a modest increase of 7.4% y/y from the high base of the first half of 2016 (+18.2% y/y). The number of Iranian visitors was up 3.2x to almost 121,000visitors and surpassed the number of Ukrainian visitors (+18.8% y/y) in the first six months of 2017.

While the top four source markets accounted for 80.7% of international arrivals in January - June, secondary source markets also posted robust performances

Arrival growth from secondary (non-EU) source markets contributed 3.7ppts to the overall growth of 13.4% y/y.The number of Israeli visitors increased 48.1% y/y to over 49,000 visitors, while the number of Indian visitors was up 132.7% y/y to over 27,000. Arrivals from the EU were up 23.2% y/y to over 128,000 visitors, with Germany (+32.3% y/y), Poland (+24.9% y/y), and UK (+27.9% y/y) driving the growth.

Tourist category continues to drive arrival growth in June 2017

The number of overnight visitors (‘tourist’ category) was up 43.0% y/y – the largest y/y growth on record – and accounted for 49.3% of international arrivals. Same-day arrivals were roughly flat, while transit visitors posted an outsized 42.9% y/y growth rate. The number of tourist arrivals is up 29.1% y/y to 1.31mn in the first half of 2017, while the number of same-day visitors is down 2.7% y/y and the number of transit visitors is up 17.1% y/y.