Q3 Forecast Revised Downward, but Strong Tourism & Export Performance Set to Boost Growth

The ISET Economist GDP Forecast for Georgia by the International School of Economics at TSU (ISET)

By Davit Keshelava & Yasya Babych

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the third quarter of 2017. Here are the highlights of this month’s release:

• Geostat has recently released its rapid estimate of economic growth for the second quarter of 2017, which now stands at 4%. As a result, estimated real GDP growth for the first half of 2017 reached 4.5%.

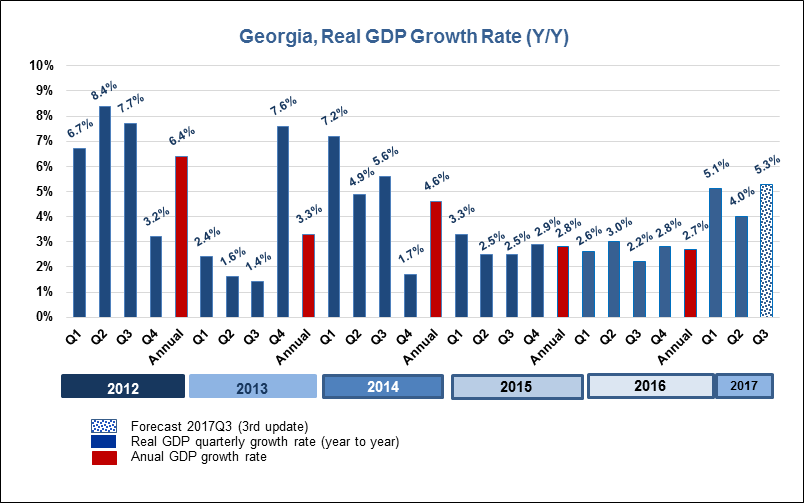

• The ISET-PI real GDP growth forecast for the third quarter of 2017 was revised downward to 5.3%.

• Based on June data, we expect annual growth in 2017 to be 5.0% in the worst-case or “no growth” scenario, and 5.3% in the best-case or “average long-term growth” scenario. We started forecasting the annual growth rate at the beginning of 2014 (see our January 2014 and February 2014 publications for a note on methodology). Typically, the annual forecast accuracy improves significantly after the second quarter data comes in.

Growth in the second quarter of 2017: good enough, but lower than expected

According to the recent release, the official estimate of growth, which is based on VAT taxpayers’ turnover data, now stands at 4%. The official estimate is 1.8 percentage point below ISET PI’s forecast. The forecast error comes from the unexpectedly low growth figures in April (only 2.1%) that significantly hampered the quarterly growth rate. This puts the government well within reach of the 4% annual growth target, although the Q2 figure is still lower than was initially anticipated by the ISET-PI forecast. Consequently, the Q3 forecast has been revised downward to 5.3%. Other factors that influence the ISET-PI forecast model continue to show remarkable stability.

However, a handful of variables have demonstrated significant monthly and yearly changes. In particular, increased money supply, improved external sector statistics, and recovered business and consumer confidence all had a positive impact on the Q3 forecast, while high inflation remains a negative contributor to growth predictions.

The first set of variables that had a significant positive effect on our forecast are related to currency in circulation. Facing increased appreciation pressure on the exchange rate, the National Bank of Georgia purchased $70 mln worth of foreign exchange reserves in four separate auctions. Overall, all monetary aggregates increased by around 15% relative to the same month of the previous year. In particular, the largest M3 and M2 aggregates increased by 17% and 14% respectively in yearly terms, while the most liquid Currency in Circulation (CCIR) went up by 16% year on year. According to economic theory, increased money supply encourages business expansion and consumption spending, which leads to a rise in aggregate demand.

The other set of variables that had a significant positive effect on the predicted GDP growth were related to the external sector. In June, exports increased by 37.4% in yearly terms (the main contributor was re-exports of copper and concentrates), while imports experienced a moderate annual reduction of 0.03%. As a result, net exports (the trade balance) improved by 13.3%. Overall, the reduction in the trade deficit made a significant positive contribution to the real GDP growth forecast.

Remittances and tourism, together with the foreign direct investment (FDI), are among the main sources of foreign funds coming into Georgia. In June, remittances increased by 17.1% relative to the same month of the previous year. Once again, the main contributors to this growth were Israel and Russia. Regarding the number of visitors, Georgia experienced a 28.5% increase in yearly terms. Moreover, inbound tourism increased by 43% year on year. As Georgia is among those countries in which remittances and income from tourism form an important part of household income, their growth had a positive impact on the projected real GDP growth.

Recovered business and consumer confidence were among the other positive contributors to the real GDP growth forecast. The Georgian Business Confidence Index (BCI), a barometer of business sentiment in the country, shows yearly improvement for the first three quarters of 2017. It is notable that businesses seem to be much more optimistic this year than they have been in recent years. In addition, theConsumer Confidence Index (CCI) shows some recovery. As a result, we observe a notable increase in consumer credit-related variables. For instance, in June, the Total Volume of Commercial Banks’ Consumer Credit increased by more than 30% relative to the same month of the previous year. The level of consumer confidence is an important factor that determines consumer willingness to spend, borrow and save. A high level of consumer confidence will encourage a higher marginal propensity to consume, leading to more vibrant consumption and an improved growth environment.

In June, six months had passed since the Georgian government increased excise on a variety of goods. As a result, the annual inflation rate reached 7.1% (the highest level in the past three years). Furthermore, inflation on imported goods reached an even higher rate of 9.8%. In the meantime, core inflation (which excludes fuel and food prices) was lower than general inflation and amounted to 4.5%. The excise tax increase is temporary and will have a one-time effect on the price level (it is expected that this effect will be exhausted by the end of the year); nevertheless, our forecasting model still identifies the inflation rate increase as a negative contributor to future GDP growth.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including the GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.