Tourism Market Watch

Sector research is one of the key directions of Galt & Taggart Research. We currently provide coverage of Energy, Healthcare, Tourism, Agriculture, Wine, and Real Estate sectors in Georgia. As part of our tourism sector coverage, we produce a monthly Tourism Market Watch, adapted here for Georgia Today’s readers. Previous reports on the sector can be found on Galt & Taggart’s website - gtresearch.ge.

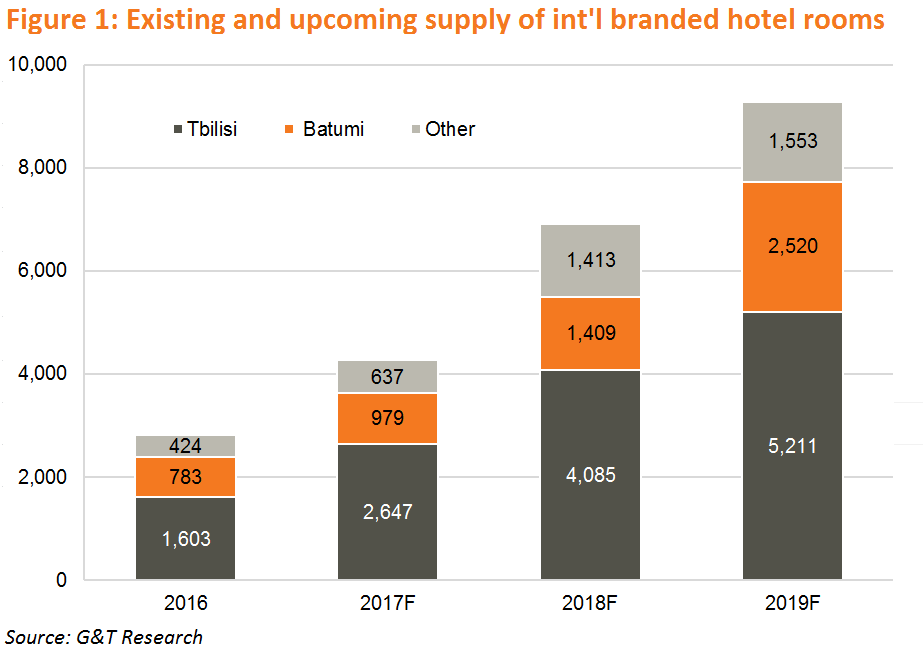

Branded hotel supply outside of Tbilisi set to increase significantly in coming years

Adjara Group Hospitality plans to open a 100-room Rooms Hotel in Kokhta-Mitarbi, the mountain resort near Bakuriani, which opened to visitors last season. With locations in Batumi and Sagarejo also in the pipeline, the Rooms brand could potentially have a portfolio of five hotels across Georgia by 2019. An 85-room Holiday Inn, expected to open in Telavi in 2018, has been added to the Kakheti accommodation pipeline, which already includes a Radisson Blu in Tsinandali and a Golden Tulip in Telavi. Branded hotel presence is also set to expand in Kutaisi. Temur Chkonia announced plans to open a five-star, 100-room Courtyard Marriott in 2019. The hotel will be the second international branded hotel in Kutaisi, following Best Western’s opening in early 2017.

Turnover in hotels and restaurants increased 17.5% y/y to US$ 553.8mn in 2016, say Geostat’s annual figures

Turnover reached US$ 271.7mn in the first six months of 2017, as strong visitor growth has boosted hospitality sector revenues. The sector has also posted significant gains in employment, with over 37,000 people employed in the hotel and restaurant industry in 2016. The sector accounted for 5.6% of total business sector employment, up from 3.2% in 2007. Salaries in the sector remain low, 33.2% lower than the business sector average. FDI in hotels and restaurants in the first half of 2017 is already at US$ 45.1mn, compared to average annual FDI of US$ 64.0mn in the sector over 2012-2016.

Tourism value added up 5.9% y/y to GEL 1.0bn in 1H17, accounting for 6.8% of GDP, compared to 7.1% in 1H16

The accommodation units subsector was the main driver, with 30.0% y/y growth. Travel companies, which account for 32.5% of tourism value added, posted a 2.5% y/y decline. International travel inflows to Georgia increased 31.2% y/y to US$ 391.0mn in August 2017 and 29.0% y/y to US$ 1.86bn in the first eight months of 2017, according to NBG’s preliminary estimates. Foreign card operations in Georgia were up 25.0% y/y to GEL 212.0mn in August 2017 and 32.8% y/y to GEL 1.37bn in the first eight months of 2017.

Agency of Protected Areas publishes visitor statistics for the first nine months of 2017

The number of visitors to protected areas was up 32.7% y/y to over 856,000 and already surpassed the 2016 annual figure. The number of domestic visitors increased 30.3% y/y to nearly 486,000, while the number of international visitors was up 36.0% y/y to nearly 371,000. Russia (27.9% of international visitors), Israel (11.6%), and Poland (6.9%) were the top drivers of growth. The most popular destinations were Prometheus Cave, Martvili Canyon, and Kazbegi National Park, each hosting over 130,000 visitors.

International Arrivals to Georgia

Number of international arrivals up 20.9% y/y to 0.76mn in September 2017

Of the top four source markets, there was strong growth from Armenia (+11.8% y/y), Azerbaijan (+15.6% y/y), and Russia (+32.0% y/y). The number of visitors from Turkey also increased (+10.5% y/y) for the third consecutive month. Arrivals from the EU were up 28.0% y/y to over 42,000 visitors.

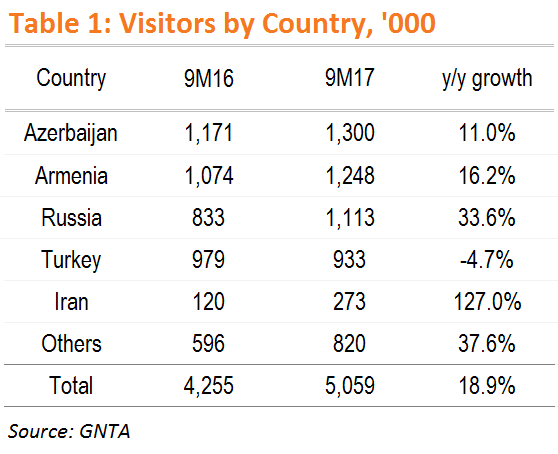

Number of international arrivals up 19.2% y/y to 5.82mn visitors in first nine months of 2017

The number of visitors increased from all major source countries except for Turkey (-4.7% y/y). The largest individual contributor to overall growth was Russia (+33.6% y/y), while Armenia and Azerbaijan also posted double-digit increases. The number of Iranian visitors was up 2.3x to almost 273,000 visitors, overtaking Ukraine as the fifth-largest source market.

Share of top four source markets in total int’l arrivals at 78.9% in the first nine months of 2017; secondary sources continue to post robust performances

The arrival growth from secondary (non-EU) source markets contributed 4.0ppts to the overall growth of 19.2% y/y. The number of Israeli visitors increased 34.9% y/y to almost 100,000, while the number of visitors from Saudi Arabia was up 175.9% y/y to over 53,000. Arrivals from the EU were up 24.8% y/y to almost 264,000 visitors, with Germany, Poland, and UK accounting for a third of the growth.

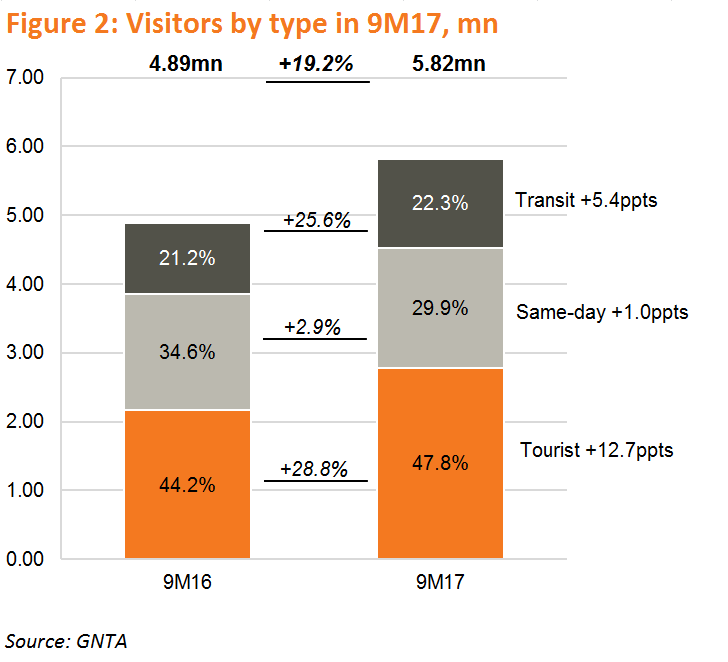

Tourist category continues to drive arrival growth in September 2017

The number of overnight visitors (‘tourist’ category) was up 24.8% y/y and accounted for 49.9% of international arrivals. Same-day arrivals and transit visitors posted 12.7% y/y and 22.6% y/y growth rates, respectively. The number of tourist arrivals in the first nine months of 2017 is up 28.8% y/y to 2.78mn, already higher than the number of tourists in Georgia in all of 2016.

By Kakhaber Samkurashvili