Georgia Sees New Real-Estate Trends

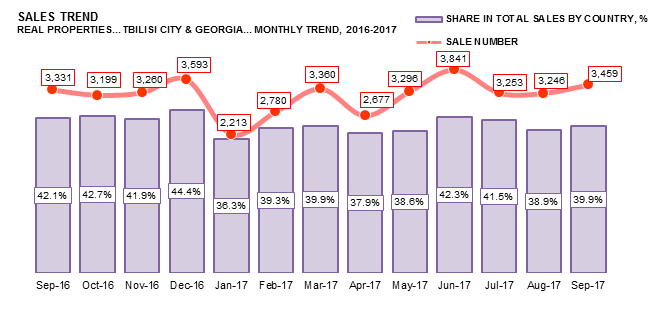

After hitting an all-time high in JUN-17, the Georgian real property market slowed down in JUL-17 (-13.8% compared to the previous month (MoM)), but gradually recovered during the next two months: AUG-17 (+6.5% MoM) and SEP-17 (+3.8% MoM). Despite the slowdown, with a total of 24 848 property sales, the GEO market in the third quarter (Q3) 2017 grew by 0.7% compared to the previous quarter, and 5.9% against Q3 2016 (YoY).

40.1% of all registered transactions took place in the capital. TBS’s share of total transactions remained stable, except for peak seasons in other regions of the country.

Ajara, with 11.9%, and Kvemo Kartli, with 9.1% shares in total sales, respectively, remained in the top 3 busiest regions. Q3 2017 YoY growth in total transactions was mostly driven by growth in the Tbilisi market (+8.4%), while outside the capital, the market grew by 4.2%.

For Q3, 2017 TOP 3 regions by sales in Georgia were:

Tbilisi (9 ,958 units, 40.1%)

Ajara (2,951 units, 11.9%)

Kvemo Kartli (2,262 units, 9.1%)

For Q3, 2017 TOP 3 districts by sales in Tbilisi were:

Saburtalo (2,416 units, 24.3%)

Vake (1,795 units, 18.0%)

Samgori (1,028 units, 10.3%)

RESIDENTIAL PROPERTY PRICES

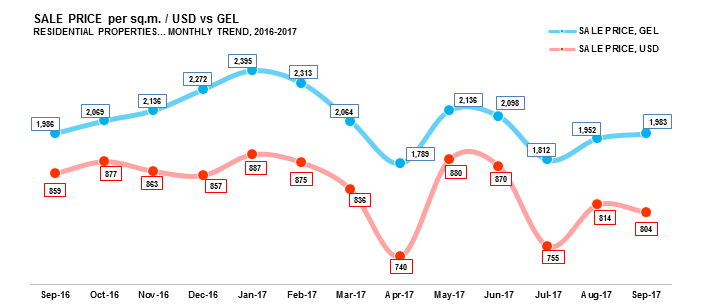

In Q3 2017, both Sales Price Index (SPI) and Rent Price Index (RPI) for residential properties reached an all year maximum in Aug-17. SPI increased by 30.9% MoM (+19.4% YoY), and RPI increased by 19.9% MoM (+16.2 YoY). In Sep-17, both indices dropped below the Sep-16 level.

During Q3 2017, Average Sales Price (ASP) varied between USD 755 and USD 804 per sq.m, and Average Rent Price (ARP) varied between USD 6.41 and USD 7.68 per sq.m.

A significant drop for ASP was recorded in Jul-17 (-13.2% MoM, -13.0% YoY). Despite swiftly recovering in AUG-17, ASP remained below 2016 levels for the rest of Q3. In SEP-17, ASP in TBS reached USD 804 (-1.3% MoM, -6.5% YoY) per sq.m, and ARP dropped to USD 6.41 (-16.6% MoM, -8.1% YoY) per sq.m.

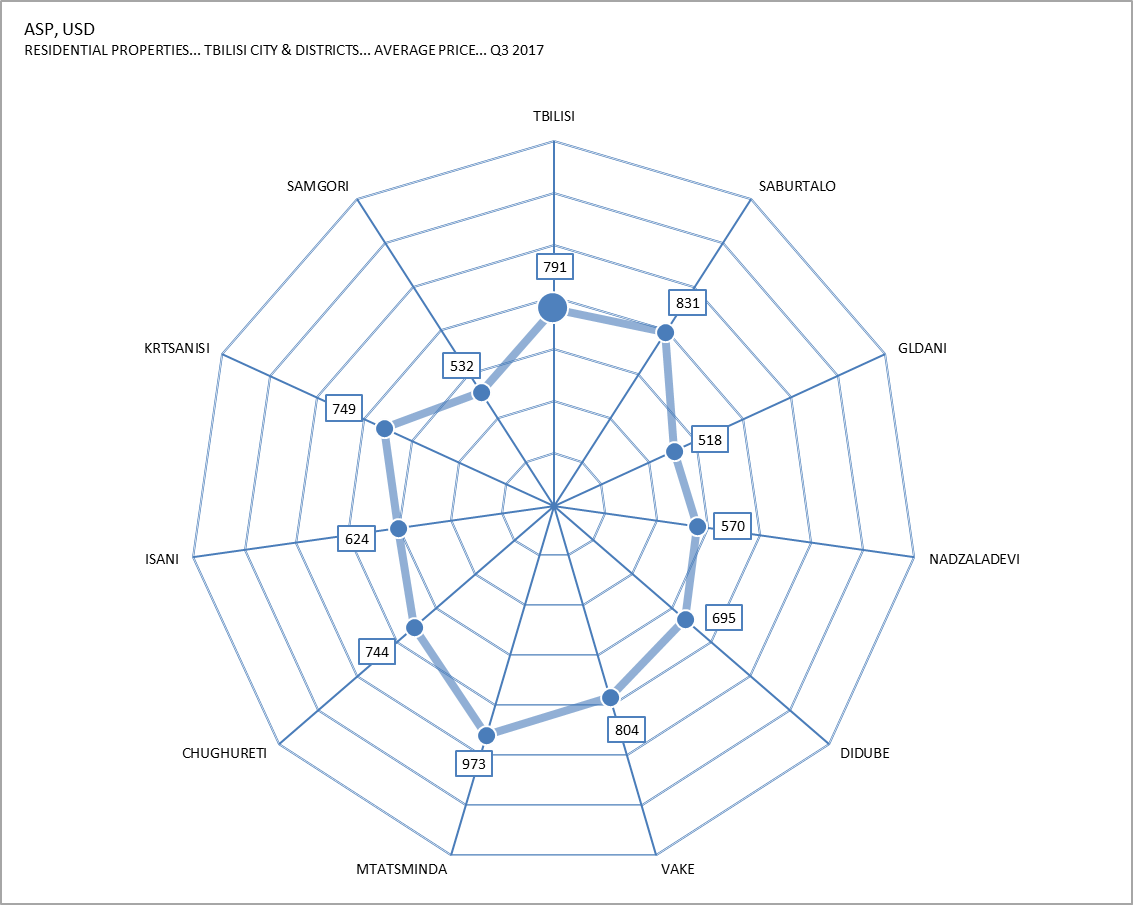

In Q3 2017, the most expensive and cheapest districts of TBS were, by ASP: Mtatsminda (USD 973) and Gldani (USD 518); by ARP: Mtatsminda (USD 8.52) and Gldani (USD 4.40).

COMMERCIAL PROPERTY PRICES

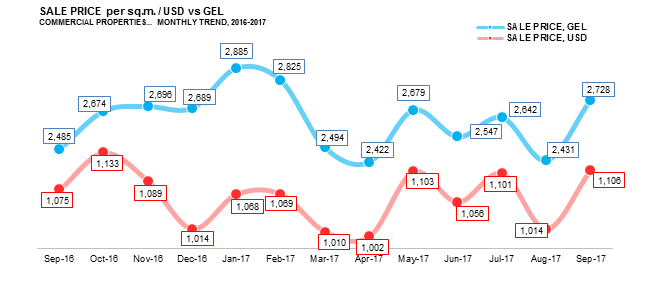

In AUG-17, SPI for commercial property dropped drastically. RPI, on the other hand, remained relatively stable. SPI declined to 0.686 (-20.1% MoM, -17.7% YoY), while RPI fell to 1.044 (-5.2% MoM, +27.0%YoY). In SEP-2017, both indices recovered, albeit with SPI finishing the quarter below the SEP-16 level.

During Q3 2017, ASP for commercial properties varied between USD 1,014 (AUG-17) and USD 1,106 (SEP-17) per sq.m, with ARP between USD 9.75 (SEP-17) and USD 10.08 (JUL-17) per sq.m.

Except AUG-17, ASPs in Q3 2017 remained above ASPs in Q3 2016, while ARPs stayed below ARPs in Q3 2016.

From ISET