Trade, Not Consumption or Investment, to Be Largest Source of GDP Growth for Georgia in 2018

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the fourth quarter of 2017 (the final update) and the first quarter of 2018. Here are the highlights of this month’s release:

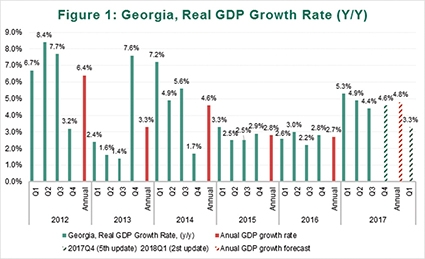

• Based on November 2017 data, the forecast for GDP growth in the fourth quarter of 2017 remained at 4.6%.

• Real GDP growth rate reached 3.7 % y-o-y in November 2017. As a result, estimated real GDP growth for the first eleven months of 2017 was 4.8%.

• Annual growth for 2017 is still expected to be 4.8%.

• According to the most recent (second vintage) forecast for 2018, the growth rate in the first quarter is predicted to be 3.3%.

Based on the available data from November, the growth forecast for 2017-2018 remains largely stable. While the changes in the current GDP forecast do not appear to be significant, a few variables deserve our attention. In particular, rapidly increasing money supply, improved external trade statistics, higher crude oil prices, and cheaper domestic currency all played important roles in forming the current GDP forecast.

Money Supply

The first set of variables that had a significant positive effect on our forecast is related to currency in circulation. In November, all of the monetary aggregates from the broadest (up by 18% yearly) to the narrowest aggregate (up by 13% yearly) experienced double-digit growth in yearly terms. Moreover, the currency in circulation itself increased by 0.4% monthly and 13% yearly.

According to standard macroeconomic theory, an increase in money supply should lower interest rates, leading to more lending/borrowing, consumption and rapid economic growth. However, there are some papers that find no significant correlation between money supply and real GDP growth, even in the short-run. The long-run effect is even more difficult to predict without knowing how well this excess money supply is allocated in the domestic economy. Our empirical model confirms the standard economic theory - the rapidly increasing money supply positively contributed to Georgia’s growth forecast.

External Sector Statistics

Georgia’s neighboring countries continue their recovery from the recent regional crisis, followed by significant slowdowns in growth, and even painful recessions. In November, the Armenian economy advanced by 9.2% yearly, while the real GDP of Azerbaijan contracted by only 0.2% compared to the same month of the previous year. It worth noting that, based on the nine months of data in 2017, the non-oil industry in Azerbaijan was on the rise (increased by 2.5%), while growth in the oil industry remained negative (decreased by 6.5%).

Deterioration of Trade Balance

Improved economic activity in the region increased demand for Georgian goods and services, but at the same time it increased the demand for imported goods in Georgia – leading to a deterioration of the trade balance. Exports grew significantly in November, but the growth rate was less than the double-digit growth we saw in previous months. In fact, November was the only period in 2017 when exports increased by less than double-digits (8% yearly).

Geostat has already published preliminary data about Georgia’s external trade in 2017. According to the report, distribution of exports by major commodity groups did not experience any notable changes – the share of copper ores and concentrates, ferro-alloys, and re-export of motor cars in total exports still exceeded 30% . The only category that suffered significant decline during 2016 was the export of hazelnuts and other nuts - reduced by more than 53% yearly.

Nominal GDP by Categories of Use

Increases in private consumption and gross capital formation were the main contributors to nominal GDP growth in the first quarter of 2017. The situation changed dramatically in the following two quarters, when net-exports started playing a more significant role in growth decomposition (see figure above).

Money Inflows and Tourism Statistics

Remittances, together with foreign direct investment (FDI), represent the main sources of external funding for Georgia. In November, remittances increased by 25% relative to the same month of the previous year. Moreover, there was a dramatic increase in the number of visitors (14%) and number of tourists (22%) yearly. This had a moderate, but still positive impact on projected real GDP growth in Q4 of 2017 and Q1 of 2018.

Brent Crude Oil Price

The increase in the Brent Crude Oil price in November, which put upward pressure on the prices of imported goods and, therefore, the general price level in Georgia, had a slight negative effect on the forecast. In November, the Brent Crude Oil price increased by 9% monthly and 40% yearly.

Exchange Rate

The Georgian Lari depreciated against all main trading partner currencies in November. The most significant depreciation was observable with respect to the Euro (5% in month and 16% in annual terms) and USD (5% in month and 6% in yearly terms). See the figure below to understand the USD/GEL exchange rate dynamics during 2017. In addition, the Real Effective Exchange Rate (REER) depreciated by 5% relative to the previous month, and by 6% relative to the same month in the previous year. Notably, during the whole of 2017, NBG did not sell foreign exchange reserves (despite the phase of Lari depreciation in October-November), and purchased 129.75 million USD worth of foreign reserves during the entire year. Overall, REER-related variables had a small negative contribution to the real GDP growth projections.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including the GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.

Davit Keshelava and Yasya Babych