In 2017 Georgia Enjoyed Highest Growth in 5 Years, Now Consumer Credit Expansion Needs Monitoring

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the first quarter of 2018. Here are the highlights of this month’s release:

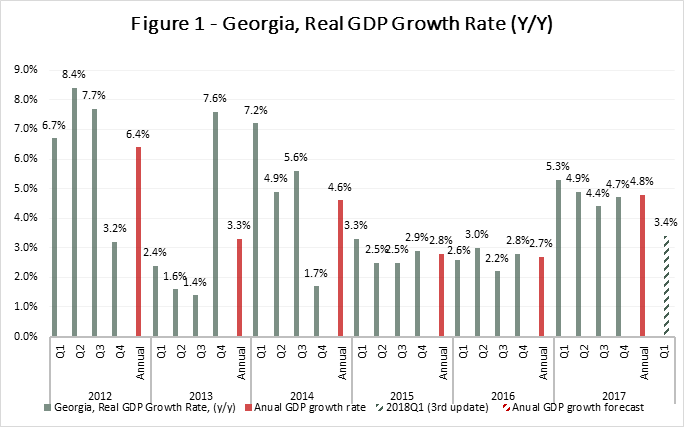

• Geostat has published its rapid estimate of real GDP growth for the fourth quarter of 2017. Estimated growth stands at 4.7%, which is only 0.1% higher than the value forecasted in the last update of our model.

• Given the latest data, Georgian annual real GDP growth in 2017 amounted to 4.8%. Our annual GDP forecast of 4.7% (since November 2017), and 4.8% (since December 2017), therefore turned out to be quite accurate.

• ISET-PI’s forecast for the first quarter of 2018 puts GDP growth at 3.4%.

Real GDP growth in 2017 is the highest in the last five years, supported by both external and domestic factors.

Geostat has released its first rapid estimate of real GDP growth for the fourth quarter of 2017, and it now stands at 4.7%. As a result, the estimated annual GDP growth for 2017 reached 4.8%, which is the highest annual growth rate in the last five years. ISET-PI forecasts annual GDP growth starting from Q1 each year, generating three different scenarios (best-case, baseline, and worst-case). Throughout the year, our predicted figures were very close to the currently released official data . For example, as early as March 2017, our baseline scenario predicted 4.3% real GDP growth, while the best-case scenario predicted 5.1%. In November 2017, we forecasted 4.7% y-o-y growth. Since then, our updated forecasts mirrored the actual 4.8% GDP growth. Notably, last year, ISET-PI model’s prediction of the annual growth rate differed just 0.1 percentage points from the actual real growth rate in 2016.

Based on the available data, one can conclude that the main drivers of real GDP growth for 2017 were notably improved external statistics, supported by domestic factors – such as increased consumption and investment, as a consequence of improved consumer and business confidence.

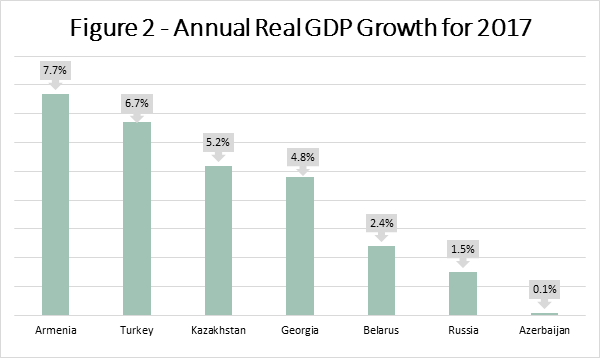

In 2017, economies throughout the region enjoyed moderate growth – the Armenian economy reached an impressive 7.7% annual growth, up from a low 0.2% in 2016. The Russian economy advanced by 1.5%, which further stimulated Georgian and Armenian economies though trade, remittances and tourism channels. Moreover, Azerbaijan finally managed to overcome a severe recession (GDP was down 3.8% in 2016), and exhibited a 0.1% annual growth. There is still no data available on annual GDP growth for Turkey. However, the latest World Bank estimates indicate that the Turkish economy may have expanded by 6.7% in 2017.

According to the most recent forecast for 2018, the growth rate in Georgia’s first quarter is will be 3.4%.

The most significant changes in our forecast were observable for variables related to excess inflation (inflation exceeding the NBG target), improved external statistics, an increased monetary base, and rapidly growing consumer credit.

Excess Inflation. According to our model, the main negative contributor to growth was the increased consumer price level, compared to the same month of the previous year. The December increase in the Consumer Price Index (CPI) amounted to 6.7% yearly, while the Producer Price Index (PPI) increased by 8.7%. About 2.7 percentage points of CPI inflation were due to higher tobacco and oil prices, driven by the one-time increase in excise tax and higher world prices for oil . For imported goods in particular, the increase in prices was 11%, while “domestic” inflation was relatively moderate at 4.9%.

The measure of core inflation amounted to a relatively moderate 4.7%, of which about 2 percentage points were due to increased tobacco prices. One can conclude that the long run, inflation in Georgia is stable and likely to converge at the 3% target level, once the excise tax effect is exhausted at the beginning of 2018.

External Sector Statistics

The other set of variables which has had a significant positive effect on the predicted real GDP growth was related to the external sector. Georgia exports continued to expand, increasing by 49% yearly in December 2017, while imports were up by 15%. The trade deficit, however, deepened by 0.8% yearly, and amounted to 557.1 million USD. The improvement in trade statistics was mainly due to better economic conditions in the entire region. Moreover, exports to China contributed significantly to growth in export revenues (mainly through copper ores and ferroalloys exports). Georgia also continued to export more wine to China. Cigarette exports increased by more than 14 times, mainly due to the increase in tobacco excise taxes. The only export category that experienced a significant decrease during the last month of 2017 was hazelnut exports.

Furthermore, remittances increased by 16.3% yearly, raising people’s disposable income, consumption and real GDP growth. The main contributors to this increase were Israel (4.4 p.p.), Russia (2.9 p.p.), Greece (2.7 p.p.) and Italy (2.6 p.p.). Russia and Euro Union countries accounted for 66% of total money inflow. In addition, the number of international visitors increased by 23.3%, while the increase in tourist numbers (visitors who spent 24 hours or more in Georgia) was even more impressive – it amounted to 31.7%. In summary, increased money inflow and the dramatically raised number of visitors and tourists in the corresponding month made a significant positive contribution to the growth forecast.

Monetary Base

The other set of variables that had a significant positive effect on our forecast is related to currency in circulation. Despite the fact that in December 2017, the National Bank of Georgia increased the Monetary Policy Rate (MPR) by 0.25%, rapid credit expansion (commercial bank loans to the domestic economy increased by 18.3% yearly) led to an increase in the domestic money supply through the money multiplier effect. All of the monetary aggregates, including the Broad Money (M3) measure, increased significantly (by 2% monthly and 15% yearly) in the corresponding month. The largest yearly increase was observed again for the M2 monetary aggregate, which went up by 29% relative to the same month of the previous year. Moreover, Currency in Circulation (CCIR) itself increased by 10% in yearly terms.

Consumer Credit

In December 2017, Total Volume of Commercial Bank’s Consumer Credit increased by 27% relative to the same month of the previous year. Consumer confidence and expectations for the future are important factors determining the households’ willingness to spend, borrow and save. A high level of consumer confidence and positive expectations will encourage a higher marginal propensity to consume, leading to more vibrant consumption and higher growth. However, rapid consumer credit expansions need to be monitored very closely by the monetary authorities – in cases when credit expansion leads to lower loan quality, and/or when the propensity to spend on imported vs. domestic goods is high, the stability of the banking system, as well as the long-run real GDP growth of the country, may suffer.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including the GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.

Davit Keshelava and Yasya Babych