Growth in 2018 Like 2017? The Economy Might Still Surprise Us…

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the first and second quarters of 2018. Here are the highlights of this month’s release:

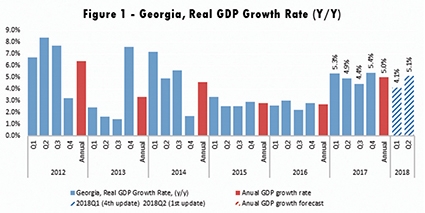

• Geostat has revised its rapid estimate of real GDP growth for the fourth quarter of 2017. Estimated growth now stands at 5.4%, which is 0.7 percentage points above the previously estimated average growth rate for Q4. As a result, the real GDP growth for 2017 reached 5.0%.

• ISET-PI’s forecast of the real GDP growth for the first quarter of 2018 stands at 4.1% - up from 3.4% in February. The first estimate of the second quarter growth forecast now stands at 5.1%.

• Based on January’s data, we expect annual growth in 2018 to be 4.6% in the worst-case or “no growth” scenario, and 5.6% in the best-case or “average long-term growth” scenario. Our “middle-of-the road” scenario (based on average growth over the last four quarters) predicts 4.8% real GDP growth. This suggests that in 2018, GDP growth will be largely similar to that of 2017. However, the economy might still surprise us as the year progresses. Keep in mind that early in 2017, the ISET-PI forecast predicted 5.1% real growth only in the best-case scenario. As it turned out, the best-case scenario was the one closest to reality.

• Currently, ISET’s middle-of-the-road annual forecast is close to the projections coming from national and international institutions. According to the National Bank of Georgia, real GDP growth in 2018 is projected at 4.5% , while the World Bank, the International Monetary Fund, and the Asian Development Bank predict 4.2%, 4.2% and 4.5% real GDP growth for 2018, respectively.

Expected Q1 2018 growth is now higher. ISET-PI’s forecast for real GDP growth for the first quarter of 2018 was revised upward by 0.7 percentage points. Two factors can help explain this: first, Geostat’s upward revision of 2017 growth for the fourth quarter, which now stands at 0.7 percentage points higher than the previous estimate. Secondly, diminishing inflationary pressures, improved business confidence, continuing money supply growth and much improved external statistics – all contributed to the buoyant expectations.

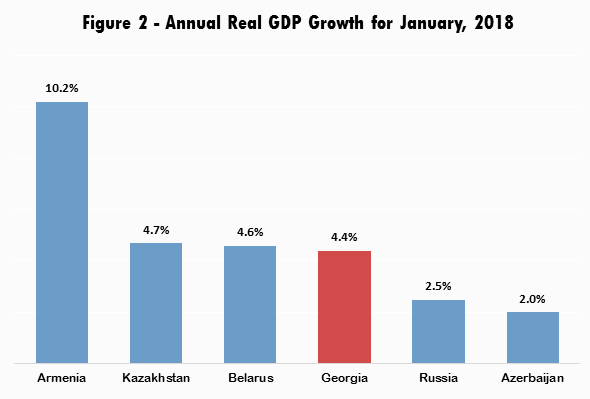

January 2018 shows strong growth in the wider region. According to the estimates for January 2018, the majority of countries in the region showed significant improvement compared to the same period in the previous year. The Armenian economy reached impressive 10.2% annual growth. The Russian and Azerbaijani economies advanced by 2.5% and 2% respectively, which further stimulated the Georgian economy though trade, remittances and tourism channels. The Georgian economy itself grew by 4.4% y-o-y in January.

Diminishing inflationary pressures

In January 2017, the Georgian government increased the excise tax on a variety of goods. As a result, the general price growth in the country notably exceeded the targeted level. As expected, however, the excise tax effect started to wane at the beginning of this year. For example, in January 2018, the effect of the excise tax on inflation was just 1.5 percentage points. The annual inflation rate amounted to the 4.3% (which is still higher than the new target rate of 3%).

Inflation on food and non-alcohol beverages subsided to 4.9%, and this sector’s contribution to the overall inflation amounted to only 1.3 percentage points. The measure of core inflation amounted to a relatively moderate 3%, of which about one percentage point was due to the lingering excise tax effect. Based on this evidence, one can conclude that inflation is not a major concern for economic growth in Georgia. The long run inflation in the country is stable and likely to converge at the 3% target level.

Exports expand, even as trade deficit deepens

The other set of variables which had a significant positive effect on the GDP growth forecast was related to trade. Georgia’s exports continued to expand, increasing by 26% yearly in January 2018, while imports were up by 18.2%. The trade deficit, however, deepened by 13.9% year-on-year and amounted to 371.2 million USD. Among the main contributors to the export increase were traditional products: petroleum and petroleum oil (599%); nitrogenous fertilizers, (135%).

Remittance inflows and tourism maintained double-digit growth in January

Money inflow increased by 31.1% compared to the same month of the previous year. In addition, the number of international visitors increased by 14.8%, while the change in tourist numbers (visitors who spent 24 hours or more in Georgia) was even more impressive – a 23% increase. Both tourism and remittances made a significant positive contribution to our growth forecast.

Recovering business confidence among strong positive contributors to real GDP growth forecast

The Georgian Business Confidence Index (BCI), a barometer of business sentiment in the country, showed a year-on-year improvement in the first quarter of 2018 and reached its highest level in the last three years. Moreover, almost 60% of business executives participating in the survey expected improvement of their businesses over the next three months.

Monetary Base

The other set of variables which had a significant and positive effect on our forecast was related to currency in circulation. As of March 12, 2018, the majority of the countries in the region were implementing expansionary monetary policy by reducing their monetary policy rate (MPR). Azerbaijan, for instance, reduced MPR from 15% to 13%; Belarus from 11% to 10.5%; Russia from 7.75% to 7.5%; and Kazakhstan from 9.75% to 9.5%.

Despite the fact that Georgia is among the countries that maintained its MPR, a rapid credit expansion (commercial bank loans to the domestic economy increased by 14.9% y-o-y) led to an increase in the domestic money supply through the money multiplier effect. All of the monetary aggregates, including the Broad Money (M3) measure, increased significantly (27% yearly) in the corresponding month, while the most liquid measure of money supply, Currency in Circulation (CCIR), experienced a 9% y-o-y growth. While credit expansion in itself is a stimulus for growth, it can also become a source of major instability. Therefore, as we progress through the year, the monetary authorities should keep a watchful eye on the financial sector, and particularly the expansion of private credit.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including the GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.

Davit Keshelava and Yasya Babych