No News is Good News for Georgia, as Forecasts Point to Stable Growth

ISET-PI has updated its forecast of Georgia’s real GDP growth rate for the first and second quarters of 2018.

Here are the highlights of this month’s release:

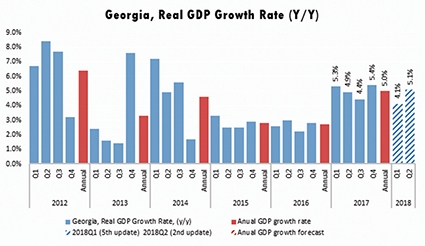

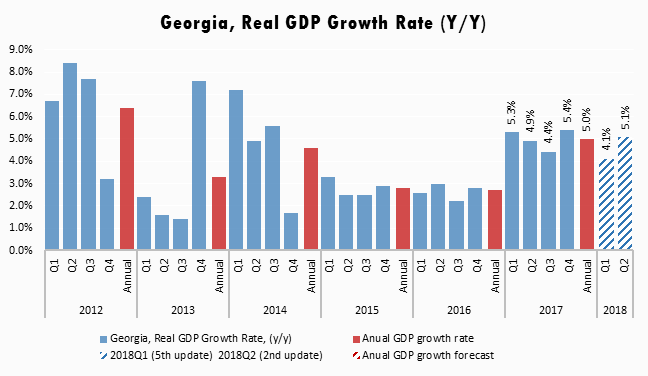

• ISET-PI’s forecast for the first two quarters of 2018 stands at 4.1% and 5.1%, respectively (no change from last month’s estimations).

• Geostat has released its rapid estimate of real GDP growth for January and February of 2018. Estimated growth stands at 4.4% and 5.5%, correspondingly. As a result, the average real GDP growth for January-February 2018 reached 4.9%.

• Based on February’s data, we expect annual growth in 2018 to be 4.6% in the worst-case or “no growth” scenario, and 5.6% in the best-case or “average long-term growth” scenario. Our “middle-of-the road” scenario (based on average growth over the last four quarters) predicts 4.8% real GDP growth.

Based on the February 2018 data, our forecast for the first two quarters of 2018 has not changed significantly. Most of the explanatory variables in our model remained quite stable in February. The most meaningful yearly changes were observed for variables related to the deposits of various maturities in commercial banks and to external sector statistics.

Lari deposits continue to grow as interest rates become more attractive for lenders. Deposit dollarization declines

National and foreign currency deposits in commercial banks grew by 15.9% annually in February 2018. The main drivers were national currency deposits which increased by 44.7% annually and 2.1% monthly, while foreign currency deposits increased by only 4.3% annually and even declined by 1.3% monthly.

The dynamics of deposit interest rates indicate that commercial banks are trying to attract more deposits in the national currency and that this policy is working for almost every type of deposit. For example, interest rates on National Currency Demand Deposits increased by 47% year-on-year and by 3% month-on-month. At the same time, interest rates on Foreign Currency Demand Deposits went down by 27% y-o-y and 2% m-o-m. As a result, National Currency Demand Deposits increased by 87% y-o-y and 7% y-o-y, while Foreign Currency Demand Deposits increased only slightly, by 1% y-o-y and even showed a decline at 4% m-o-m.

De-dollarization measures introduced by the Georgian government, along with improved macroeconomic environment and stable exchange rate, led to a notable reduction in deposit dollarization (by 0.6 percentage point to 63.8%). The combination of these factors has had an overall positive (albeit slight) effect on our model’s prediction of GDP growth.

Out with the Dollar, in with the Lari: long-term loans are increasingly de-dollarized

There were also a few variables which had a slight negative effect on our predictions. These variables were mostly related to Consumer Credit. In year-on-year terms, the Short-Term Volume of Commercial Banks' Consumer Credit in Foreign Currency increased by 37%, but the Long-Term Credit Volume of Commercial Banks' Consumer Credits in Foreign Currency declined substantially, by 10%. As these variables are quoted in lari terms, the growth rates are even higher (or lower in case of negative growth) after excluding exchange rate effect .

The Credit Volume of Commercial Banks' Consumer Credits in the National Currency was increasing for both short- and long-term loans – by 33% and 46%, respectively. The latter suggests that after introduction of de-dollarization measures, long-term Consumer Credit in Foreign Currency is being widely replaced by long-tern Consumer Credit in National Currency. As a result, dollarization of loan portfolios declined by 0.5 percentage points and stood at 55.6%.

The set of key variables that had a slight positive effect on our forecast for the first two quarters’ growth were Import-Export as well as Money Inflows and Tourism.

Exports continue the positive dynamics from last year, although the trade balance has deteriorated due to high imports. In February, total exports rose by 25% y-o-y, driven by higher re-exports of copper and copper ores (to EU countries), which contributed 8.8 percentage points to total export growth. The main destination markets for Georgian export products were Russia, Bulgaria, Turkey, Azerbaijan, Armenia, Lithuania and Ukraine, accounting for 64% of total exports.

These promising trends in Georgian export statistics are closely related to the improved economic performance of Georgia’s trading partner countries. According to estimates for February 2018, the annual growth rates for the countries in the wider region were 7.3% for Armenia, 1.5% for Russia, 1.3% for Azerbaijan, 5.6% for Kazakhstan, and 5.6% for Belarus. The improved economic conditions in partner countries further stimulates the Georgian economy though trade, remittances and tourism channels.

Imports increased by 8.7%, driven by petroleum and petroleum gases, wheat and tobacco products. Turkey, Russia, Azerbaijan, China and Ukraine were the main sources of Georgian imports in February. As a result, the trade deficit deepened by 1.5% year-on-year, and amounted to 416.4 million USD. Interestingly, in terms of destination countries, Georgian imports are becoming more diversified, while exports were less diversified compared to the same month of the previous year.

Both remittances and tourism showed significant annual increases in February. Money inflows increased around 21%, while money outflows increased by 23%, compared to the same month of the previous year. The European Union, Russia and Israel accounted for 74% of total remittances. In addition, the number of international visitors and tourists increased by 20% and 27%, respectively. Both tourism and remittances made a significant positive contribution to our growth forecast.

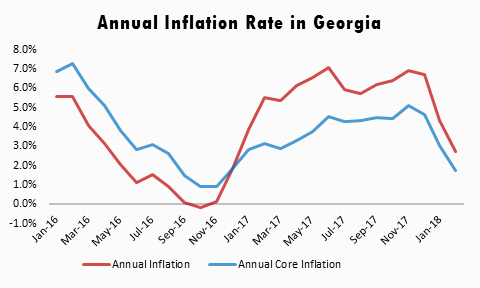

Inflation pressures subside in 2018

Inflation pressures moderated as the national currency exchange rate strengthened. The lari continued to appreciate in February 2018; it strengthened against the US dollar by 3.3%, while the nominal effective exchange rate gained 2.4% month-on-month. The pressure on domestic prices from a one-time increase in excise taxes last year has already subsided. Annual inflation in February 2018 constituted 2.7%, which was in line with the 3% NBG target. In addition, annual inflation on imported goods came down to 1.8% while the core inflation rate stood at a low 1.7%. This is good news for the Georgian economy, as low core inflation typically translates into lower overall inflation in the future.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including the GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly for forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.

By Davit Keshelava and Yasya Babych